Chicago finances are even worse than I thought which is saying quite a bit because I have written about the sorry state of Chicago finances on numerous occasion.

Kristi Culpepper, a bond guru, has gone over Chicago’s annual financial report, bond documents, investor presentations, and CAFRs. She has uncovered things the City of Chicago does not want anyone to understand.

For example, Culpepper reports Chicago general obligation bond deals have been used by the city as a means to avoid servicing short-term debt. Says Culpepper, “These bonds have received extraordinarily aggressive tax opinions . If the Internal Revenue Service ever gets around to scrutinizing them, your bonds probably won’t be tax exempt for long. Many of these uses of bond proceeds are not eligible for tax-exempt financing under the federal tax code.”

That is just the tip of the iceberg as to what Culpepper has discovered.

Who Is Kristi Culpepper?

Intrigued? You should be.

First let’s go over Culpepper’s background. Kristi Culpepper is a state government official with the Commonwealth of Kentucky. Among other things, she handles the structuring and sale of bonds for schools across the state. Previously, she worked for the Kentucky General Assembly analyzing state and local government bond issues and tracking the state’s capital construction programs. She has also worked at Merrill Lynch.

“Bond Girl”

Culpepper built up a huge following as “Bond Girl”. Bloomberg explains Twitter’s ‘Bond Girl’ Outs Herself as Kentucky Official.

Bond Girl, using the Twitter handle @munilass, had been posting commentary about state and city borrowing and issues beyond public finance since April 2011. Her sometimes-pointed posts attracted the attention of municipal-bond investors, bankers and analysts. Using her nom de Twitter, Culpepper sparred with other users, criticized public officials and vented about her life.

Culpepper “is regarded as an authority on capital projects and debt by the Legislative body,” according to a Kentucky Education Department website posted in November that announced her appointment. “She has worked with legislators, lobbyists, and attorneys to draft legislation and effect policy changes related to the state’s bonded indebtedness.”

Buyers and traders in the $3.7 trillion muni market had puzzled at the true identity of Bond Girl, Hector Negroni, co-founder of New York-based investing firm Fundamental Credit Opportunities, said in a telephone interview.

“For any bond geek like myself, she’s fascinating, well-informed and entertaining,” Negroni said.

On Oct. 28, as Bond Girl, she wrote a 1,650-word blog post for the Financial Times’ Alphaville on a proposed debtor-in-possession financing for bankrupt Detroit.

Guest Post

I mention the above to prove Culpepper is highly regarded in the industry. She knows what she is talking about.

The following guest post by Culpepper first appeared on Tumblr as How Chicago has used financial engineering to paper over its massive budget gap.

For those who want to follow Culpepper, her Twitter handle is @munilass.

I dispense with my usual blockquotes for ease in reading. What follows is a guest post by Kristi Culpepper.

Emphasis in Italics is Mine – My Comments and Recommendations follow Culpepper.

How Chicago Used Financial Engineering to Paper Over its Massive Budget Gap

Chicago made headlines at the end of February after Moody’s downgraded the city’s general obligation bond rating to Baa2. Moody’s has cut Chicago’s rating five notches in less than two years. This downgrade, however, placed the city’s credit below the termination triggers on some of its outstanding interest rate swaps. The city has been working to renegotiate the terms of those contracts with its counterparties.

If Chicago’s general obligation rating falls below investment grade, the city’s credit deterioration will become a self-fulfilling prophesy. The city risks nearly $400 million of swap termination payments and the acceleration of its $294 million of outstanding short-term debt.

Unsurprisingly, some of Chicago’s bonds are already trading at junk levels. Chicago CUSIPs are listed here.

That said, the rating agencies and most other market participants still appear to be light years away from understanding the true scope of Chicago’s financial problems. The city has a very — well, let’s just call it unconventional — approach to borrowing money and probably should not be considered investment grade.

Some Budget History

In order for you to follow my discussion of Chicago’s borrowing shenanigans, it is necessary to understand the fiscal machinery behind its bond issues. Please be patient with me here. This story will blow your mind shortly.

Chicago’s budget is divided into seven different fund classifications, but only three funds are relevant to our narrative: the Corporate Fund, Property Tax Fund, and Reserve Funds.

The Corporate Fund is Chicago’s general operating fund. This fund is used to pay for essential government services and activities (e.g. public safety and trash collection). Corporate Fund revenues are derived from a wide variety of sources, including: (1) local tax revenue from utility, transaction, transportation, recreation, and business taxes; (2) intergovernmental tax revenue, which represents the city’s share of the state’s sales and use taxes, income tax, and personal property replacement tax; and (3) non-tax revenue from fees, fines, asset sales, and leases.

Chicago’s property tax revenues do not go into its general operating fund. These revenues go into a Property Tax Fund, which is used to make debt service payments on the city’s general obligation bonds; make required employee pension contributions; and (to a minor extent) fund the library system. The fund also includes tax increment financing revenues that flow to projects in designated TIF districts.

The city used some of the proceeds from long-term leases of city assets to establish Reserve Funds. The Chicago Skyway reserve funds were established in 2005 in the amount of $975 million. The Metered Parking System reserve funds were established in 2009 in the amount of $1.15 billion. Of these funds, $475 million of the Skyway reserves were designated for budgetary uses. What remained was $500 million for the Skyway; $400 million for the Metered Parking System; and $326 million for a budget stabilization fund.

There has been a structural gap in Chicago’s Corporate Fund budget since at least 2003. Although most governments are required to balance their budgets on a cash flow basis each fiscal year, a structural budget gap can arise when recurring expenditures are greater than recurring revenues. Some of the city’s offering documents suggest that this gap is a legacy of the last economic downturn, but in reality the gap pre-dates the economic downturn by several years. The impact of economic downturns on tax collections tends to have a considerable lag anyway.

So, Chicago’s structural budget gap is a political, not economic, creature. Rather than cut expenditures to a level that could be supported by recurring revenues, the city mostly used non-recurring resources to fill the gap from one fiscal year to the next. This is not surprising. Most of Chicago’s Corporate Fund budget goes to salaries and benefits for its employees, and 90% of the city’s employees belong to around 40 different unions. Attempts to adjust expenditures tend to have well organized opposition.

Between fund transfers and drawing down its reserves, the city blew through its financial cushioning quickly. The $326 million budget stabilization fund was exhausted by 2010. From 2009 to 2011, the city used $320 million from the Metered Parking Reserves. The city’s budget gap was at its widest in the wake of the last economic downturn, at over $600 million.

Chicago’s Dysfunctional Debt Program

Now things start to get interesting. Transfers from reserves and other funds have not been the only means Chicago officials (across administrations) have devised to subsidize the city’s Corporate Fund. The city has effectively been using its general obligation bond offerings and interest rate derivatives to accomplish the same thing.

State and local governments typically use the proceeds from their bond offerings to construct or renovate public buildings and infrastructure. These are projects that have long useful lives and will benefit residents for generations.

Dating back to at least 2003, however, Chicago has been issuing long-term tax-exempt and taxable bonds to:

(1) Roll over short-term debt used as working capital;

(2) Pay for maintenance activities that would otherwise be paid from the Corporate Fund;

(3) Pay for judgments and settlements that would otherwise be paid from the Corporate Fund, including wage increases and retroactive pension contributions for its employees; and

(4) Provide discretionary funds to each of the city’s 50 aldermen to pay for activities in their own districts.

The magnitude of tax-exempt bond proceeds used for judgments and settlements over this period is staggering. The Chicago Tribune estimated it at approximately $400 million:

In 2002, for example, the city used tax-exempt bonds to pay an arbitration award involving the Fraternal Order of Police. Rank-and-file officers rejected a city contract offer in 2001, but an arbitrator ruled in favor of the city’s wage proposal a year later.

The deal included raises of 2 to 4 percent a year, to be applied retroactively. In bond documents, city officials deemed the back pay the city owed an extraordinary expense and paid $164 million of it with tax-exempt bonds.

The city ultimately will need to pay bondholders $280 million to cover the loan …

Bonds also ended up covering the $28 million a jury awarded to Joseph Regaldo in 1999. The jury found that, years earlier, a Chicago police officer had beaten him in the back of the head and neck with a blunt object, which ripped apart an artery and cut off the blood supply to his brain. The injuries left Regaldo unable to walk, talk or care for himself.

The judgment won’t be paid off until 2019 at the earliest; by then, the total cost will have grown to $53 million.

City officials eventually switched to paying judgments with taxable bonds, which are even more costly in the long run.

That is, until 2012:

About $54 million from a tax-exempt bond helped cover a legal judgment awarded to African-Americans who were denied a chance to become firefighters by a 1990s entrance exam that favored white applicants. An additional $8 million in tax-exempt bond money went to pay legal fees related to the case, records show.

By using bond money, the city created an irony for many of those awarded damages, as their future property taxes will help pay interest on the debt. In 2033, when the city starts paying down the $54 million, interest will have more than doubled the total cost.

Stop and let that sink in for a moment. That police brutality case? Wage increases negotiated with labor unions? Not just financed, but financed with long-term debt.

So why haven’t the city’s 50 aldermen protested the use of bond proceeds for these purposes? It probably has something to do with the “Aldermen’s Menu,” which allows the aldermen to use a portion of the proceeds from the city’s general obligation bond issues to pay for whatever they want for their district.

It is unclear (to me) whether the city tracks how the funds from the “Aldermen’s Menu” are spent, but in the aggregate they are not a negligible amount. From 2003 to 2012, these projects have ranged from $54.2 million to $102 million.

The use of bond proceeds to provide slush funds for policymakers has a historic analog in the revenue bonds Harrisburg issued for its incineratorproject as the city was on its path to insolvency. Pennsylvania law limits the amount of debt local governments can issue to finance projects that are not self-supporting. Substantially all of the bonds tied to the incinerator project were issued to provide working capital, although city officials were able to locate financial advisory firms that were willing to certify the opposite to state regulators.

In order to win authorization for bond issues that outright defied state law, Harrisburg’s later bond issues included a “Special Projects Fund” for city officials to play with. They bought things like artifacts for a Wild West Museum. In Pennsylvania. Don’t think too hard, there is no why.

See? Reading the Sources and Uses provisions in official statements can be fun. I know, this makes you want to invite me to your next dinner party.

Our story gets even more interesting when you look at how Chicago’s past general obligation bond offerings have been structured.

First, the city has undertaken several large, non-traditional refundings to push the maturities on debt that is coming due out into later years.

A traditional refunding is akin to how a homeowner refinances a mortgage loan. A new loan is used to prepay an old loan to achieve an interest cost savings. A “scoop and toss” refunding, which is what Chicago has done, involves additional interest cost — even in a ridiculously low interest rate environment — because the debt remains outstanding for a longer period of time.

The objective of these deals was to provide budget relief for the city’s general operating fund in the short term, even if the structure means escalating debt service payments in the long term. These restructurings artificially inflated the city’s debt capacity, so the city could continue to use property tax-supported bonds to take out the city’s working capital credit facilities, which allowed the city to avoid balancing its Corporate Fund budget.

Chicago is far from the only government to restructure debt for budget relief. Quite a few state and local governments engaged in similar transactions following the last recession. What makes Chicago unique is, again, the magnitude of this activity. According to the Chicago Tribune, “since 2000, the city has used $3.6 billion in bond money to refund old debt as principal payments came due. Of that amount, half will end up costing taxpayers in the long run.” For the sake of comparison, Chicago has around $7.2 billion of general obligation bonds outstanding.

Second, Chicago’s past few general obligation bond offerings have involved considerable amounts of capitalized interest.

Capitalized interest is typically associated with project finance, not general obligation bond issues. Project finance is a sector where loans finance revenue-producing facilities and infrastructure. The debt is supported by those revenues, not taxes as with general obligation bonds.

With capitalized interest, a bond issuer borrows more money than a project requires for construction in order to pay the interest on the bonds while the project is being built. The idea here is that the project will eventually generate revenues that can support debt service payments and the cost added by capitalizing interest.

From 2010 to 2014, Chicago’s general obligation bond deals included over $235 million of capitalized interest, simply as a means for the city to avoid servicing its debt in the short term.

If you are a bondholder, there are two things you should take away from this segment of our narrative.

First, if you hold the tax-exempt portion of these deals and the Internal Revenue Service ever gets around to scrutinizing them, your bonds probably won’t be tax exempt for long. Many of these uses of bond proceeds are not eligible for tax-exempt financing under the federal tax code. These bonds have received extraordinarily aggressive tax opinions — including, incidentally, from the same law firm that drafted Illinois’s swap legislation, which I will get to momentarily.

Second, Chicago taxpayers are on the hook for billions of dollars of long-term debt and have little of tangible value to show for it. There is a good chance that residents do not understand the nature of their government’s borrowing activities, since these were complex offerings. (Well, unless they read what I have written here…) As debt service payments increasingly compete with other political priorities for funding, this revelation might eventually erode the city’s willingness to pay.

These transactions should never have happened.

Chicago’s Interest Rate Derivatives Portfolio

Perhaps a third thing a bondholder should take away from our narrative is that to the extent Chicago is slapped with future termination payments on its interest rate derivatives, the security for your investment will be diluted. Since Chicago’s property tax revenues are also applied to pension contributions and the debt/derivatives of several other overlapping taxing districts, this is not an insignificant factor.

The State of Illinois authorized local governments to use interest rate derivatives in 2003. Here is a link to the legislation. The bill restricts the notional amount of a municipality’s interest rate derivatives to the outstanding debt the contracts will ostensibly hedge. Since the notional amount of a swap, etc. says nothing about an issuer’s risk exposure, this provision is pretty much worthless. And since the legislation was drafted by the financial industry, that probably wasn’t an accident.

The legislation allows the municipality to make payments due under the swap contract (which would include termination payments) from any source of revenue it has, including property taxes. This probably wasn’t an accident either.

Chicago used interest rate swaps on its 2003, 2005, 2007, and 2009 bond deals, apparently as part of a synthetic fixed rate strategy. (I explain the mechanics of synthetic fixed rate deals in this essay.) The city also recreationally experimented with more exotic contracts — swaptions and the like.

The associated bond offerings were multimodal. Multimodal bonds are bonds that can be converted to any of a number of interest rate modes at the option of the issuer. Bond documents allow the bonds to be remarketed daily, weekly, or monthly as variable rate tender option bonds, or in term or fixed rate modes. Like capitalized interest, this structure is typically used only in project finance. The multimodal structure allows long-term debt to function as both interim and permanent financing to accommodate the life cycle of a revenue-producing project.

Because the underlying debt is multimodal, Chicago never required interest rate derivatives to hedge its interest rate exposure. The city could have virtually any interest rate exposure it wanted as the bonds were remarketed. Why don’t all government issuers use this structure, you ask? Because most governments value predictable payments over trying to handicap interest rate trends and basis risk. That’s a function of being tethered to a budget.

As I noted at the beginning of this essay, Chicago is now almost $400 million out-of-the-money on its outstanding swaps. This only matters to the extent that the city’s credit ratings continue to sink toward termination triggers. Only one rating agency has to break these thresholds — so, even though S&P and Fitch still somehow believe Chicago is an A+/A- credit, Moody’s is the only rating agency that matters. If the city doesn’t get cut to junk and interest rates normalize, Chicago’s interest rate swap situation will eventually repair itself. The tipping point here either way is probably the outcome of the state/city’s pension litigation.

Chicago Public Schools — which already takes more property tax revenues from Cook County than the City of Chicago — has a swap/pension nightmare of its own to muddle through. Between the city and school system, area residents are at risk of making/financing $660 million of termination payments. The payments would compete with $28.3 billion of city and overlapping debt and billions of dollars of escalating pension contributions for funding. Basically, if you are in Chicago, your property is about to become more expensive.

From the outside, it looks like Chicago also used its interest rate swaps as a means of drumming up non-recurring resources to fill its budget gap in 2010 and 2011. If so, this is another example of the city’s willingness to trade long-term costs for avoiding politically inconvenient spending decisions.

The city made amendments to outstanding swap contracts by layering on forward-starting basis swaps. (This is something else Chicago has in common with Harrisburg.) These transactions changed the city’s net interest rate exposure on those deals from fixed to variable and introduced basis risk to the portfolio after they became effective in 2014. There was not an event that prompted these amendments and the city remains underwater on the deals. The city did receive a series of up-front payments, however. Judging from the swap confirmations from Deutsche Bank, PNC, and Wells Fargo, these payments amounted to around $25 million.

Could Chicago File for Chapter 9 Bankruptcy?

No. At least not right now. To be eligible to file for bankruptcy under Chapter 9, there must be a state law that specifically authorizes a municipality to do so. Illinois law does not currently permit municipalities to do so, except under a provision that relates to units of governments with populations under 25,000. Of course, Chicago would also have to meet the other eligibility criteria. The city does have a relatively large tax base.

That said, if state lawmakers wanted to give Chicago the ability to adjust its pension liabilities — its pensions have an aggregate funded ratio of 37% — amending a statute is a lot easier than amending the state constitution. Article 8, Section 5, of the Illinois Constitution says: “Membership in any pension or retirement system of the State, any unit of local government or school district, or any agency or instrumentality thereof, shall be an enforceable contractual relationship, the benefits of which shall not be diminished or impaired.”

Multiple federal bankruptcy judges have ruled that the federal bankruptcy code supersedes state constitutions, which theoretically provides a path for municipalities to adjust their pension commitments. The rulings have not been challenged in an appellate court, however, so there isn’t a bona fide legal precedent yet.

Illinois’s Constitution describes pension commitments as contractual in nature. For an obligation to be considered secured in bankruptcy, there has to be a property interest.

This logic also applies to the city’s general obligation debt though. For most of the city’s outstanding general obligation bonds, the city has pledged a specific property tax levy. Illinois is not one of the handful of states that provides general obligation debt a statutory lien. So it would seem, in my very non-legal opinion, that the bonds would be considered unsecured debt.

As I noted earlier, the city’s general obligation bond offerings have provided little of tangible value to taxpayers. If the city were authorized to file for bankruptcy and actually did so, there could potentially be political pressure to adjust general obligation debt before depriving pension beneficiaries their incomes.

It seems unlikely that the state or federal government would “Lehman” Chicago. It is the third largest city in the United States and a vital transportation hub. It seems reckless, however, to dismiss this possibility in its entirety over the medium term.

When you tally up the ways bond proceeds have been used to offset operating expenses, scoop and toss restructurings, capitalized interest, and swap modifications, the city’s cumulative Corporate Fund budget gap is much, much larger than the city’s disclosures imply. At some point, this manner of doing business will collapse.

END Culpepper

There is much above to digest. Anyone investing in Chicago “Tax Exempt” bonds need beware.

Meanwhile, and in regards to Culpepper’s article, Yahoo! Fiance reports “The City of Chicago Mayor’s office did not respond to multiple calls and emails seeking comment on the matter.”

Politically and Financially Bankrupt

I have stated many times, my belief that Chicago is bankrupt; it’s just not officially recognized. Actually, Chicago is both politically and financially bankrupt.

The analysis from Culpepper confirms my belief. Her report provides many more details of what’s really behind Moody’s downgrade.

I wrote about the downgrade in Chicago’s Fiscal Freefall: Moody’s Cuts Chicago Credit Rating to Two Steps Above Junk; Snake Oil and Swaps; It’s All Junk Now.

When will Fitch and the S&P catch up? Perhaps after they see this article.

Chapter 9 Bankruptcy Test

My personal viewpoint on bankruptcy aside, it’s important to point out that Chapter 9 has a different insolvency test than corporate bankruptcy.

“It is not a balance sheet test, but a cash flow test. Municipality has to be in a position where it cannot make near-term payments on obligations as they come due (like within six months). This is one of several eligibility criteria. So Chicago is not bankrupt by definition (yet) and has a huge tax base. The biggest risk to residents (now) is that they are in for an absolutely massive property tax hike to pay for debt and pensions,” says Culpepper.

Pension Liabilities

On March 2, I wrote Illinois Pension Plans 39% Funded; Taxpayers On the Hook for $105 Billion in Liabilities; It Will Get Worse!

That was my second article for the Illinois Policy Institute where I am now a senior fellow. Please give it a look as it contains a detailed look at horribly funded Illinois Pension Plans state-wide, not just Chicago.

World of Hurt Coming Up

When the equity and junk bond bubbles break (and they will – big time), Illinois and numerous cities in the state will be in a world of hurt.

It is imperative the Illinois legislature start addressing these issues right now. Of course, California and numerous other states will be affected as well.

Needed Legislation

I mentioned three things Illinois needs to do in my first post for the Illinois Policy Institute: Right-to-Work Sweeps Midwest, Heads for Passage in Wisconsin.

- Eliminate collective bargaining of public unions

- Pass Right-to-Work legislation

- Scrap prevailing-wage legislation

Cities, municipalities, and the state itself massively overpay for services because of the influence of public unions and onerous prevailing wages laws. This needs to stop now.

Raising Taxes Not the Answer

Raising taxes is not the answer. Illinois taxpayer pockets are nowhere deep enough to fix massive budget and pension undefundings.

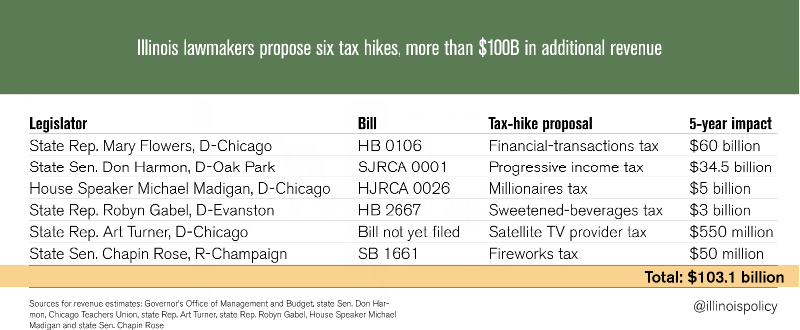

Unfortunately, the Illinois legislature does not see it that way. Check out the massive Proposed Tax Hikes.

The array of six tax hikes proposed by Illinois lawmakers this legislative session adds up to more than $100 billion over the next five years. That’s more than the state’s total projected general-fund spending in fiscal years 2016, 2017 and 2018 – combined.

And the tax-hike proposals don’t stop there.

Additional tax-hike proposals are being thrown around without any idea of how much they might raise. State Rep. Rita Mayfield, D-Waukegan, proposed a 3.75% tax on guns and gun parts. When asked how much revenue it would raise, she said she didn’t know but thought “if we can get a good million or so, I’ll take it.”

Never-Ending Tax Hikes

The big problem with raising taxes is it will never stop.

Progressives will ask for more and more and more, driving businesses and mobile individuals out of the state. Moreover, tax hikes forestall the ability of municipalities to declare chapter 9.

Bankruptcy Law and Pension Reform

Rather than burden taxpayers (and tax hikes will ultimately not work any better in Illinois than they did in Detroit), Illinois desperately needs legislation to …

- End defined benefit pension plans

- Allow municipalities to set their own benefits (benefits are now they are set at the state level as if the state knows what’s best for every municipality)

- Allow cities and municipalities to declare bankruptcy

Frank Discussion Needed

As I wrote on March 3, Chicago’s Only Possible Salvation is Bankruptcy – a Name That Cannot be Spoken.

The Illinois legislature and the city of Chicago both need to admit the sorry state of affairs instead of opting for can-kicking exercises that make the inevitable day of reckoning worse.

So, instead of playing shell games with derivatives, general obligation bonds and interest rate swaps, and instead of using long-term financing to fund ongoing needs, how about a frank discussion of everything discussed above?

The legislature and the City of Chicago owe taxpayers an honest assessment. It’s a sad state of affairs that we have to get that assessment from a bond guru in Kentucky.

Unsurprisingly, Chicago city officials would not comment.

Mike “Mish” Shedlock

http://globaleconomicanalysis.blogspot.com