Congress is about to pass a massive infrastructure plan, one of the largest in history.

And several companies stand to come out on top.

But we don’t want to bring you just any random infrastructure stocks.

That’s why we looked into our TrackstarIQ data.

We looked at which companies saw increased search volume. Then, we married that with fundamental and technical analysis to come with one really interesting stock:

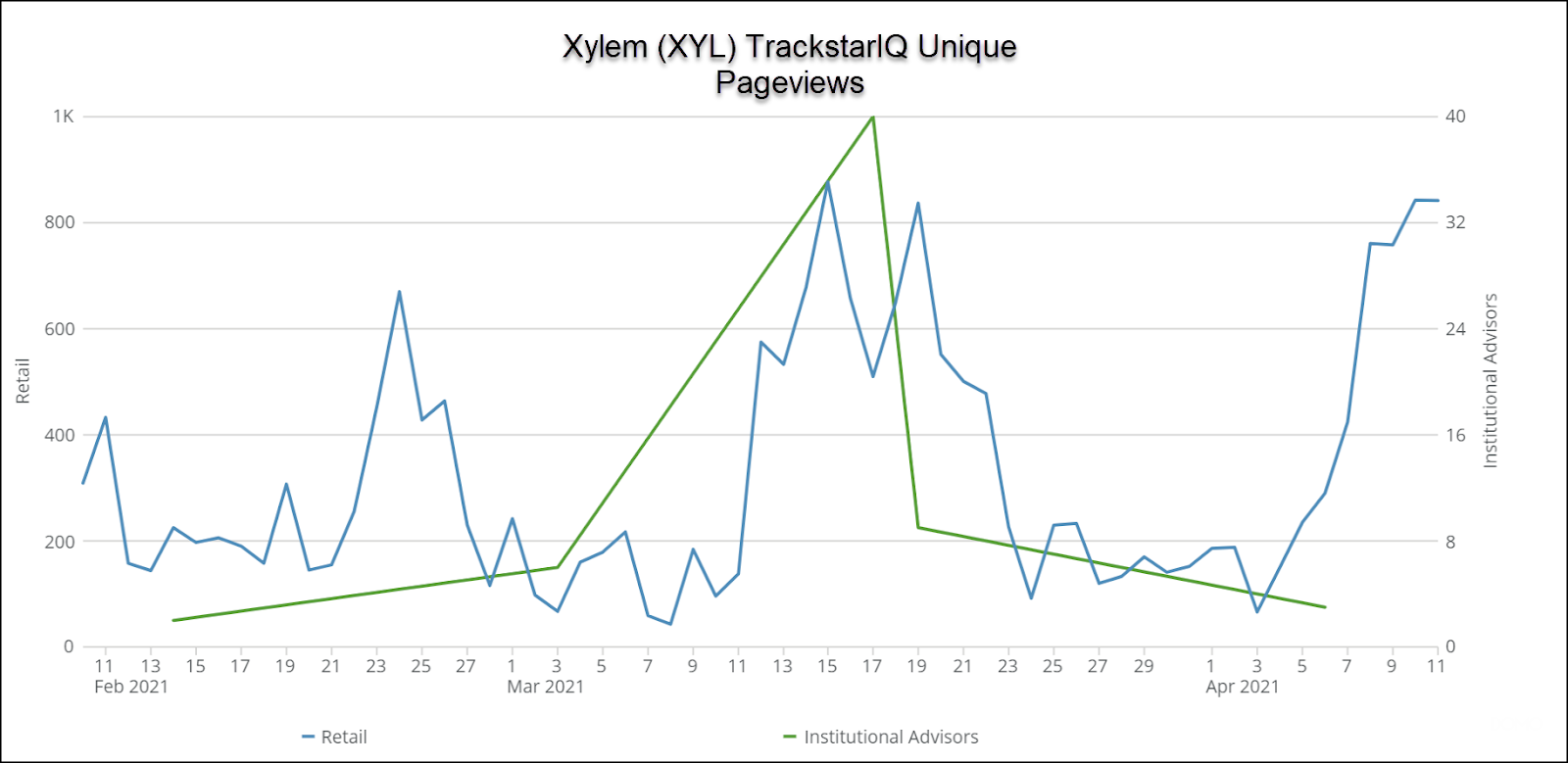

Xylem Inc (XYL)

Last week alone, Xylem saw a 300% increase in pageviews!

And we’ve got an interesting options strategy to take advantage of current price levels.

Click here to continue reading

Xylem Inc (XYL)

We turn on the tap and rarely wonder about what got that clean water to us.

Yet, there’s a whole industry dedicated to not just delivering us water, but recycling it for the environment.

Demand for water continues to climb around the world.

By 2025, 1.8 billion people will live in countries or regions with an absolute water scarcity.

Xylem aims to change that.

The company operates three segments: water infrastructure (44.9% of revenues), applied water (28.7% of revenues), and measurement & control solutions (26.4% of revenues).

Xylem focuses heavily on environmental, social, and corporate governance (ESG), even dedicating an entire deck to it for investors.

Revenues declined year over year in 2020 by 7.11%. However, their 5-year average runs around 6%.

More importantly, Xylem pays out a healthy 1.3% dividend and currently runs at around a 77x p/e ratio.

But, if the company is able to recapture its margins prior to the pandemic, we’re looking at a 35x-50x p/e ratio.

That certainly doesn’t make it a cheap stock. But they managed to surprise investors in the last quarterly report.

Prior to the pandemic, shares traded near $90 prior to the pandemic. That’s not too much cheaper than the current $108 mark.

And rather than wait for shares to pull back, here’s an idea to get paid in the interim.

Options 101

Have you considered the cash-covered put?

Cash covered puts pay you to wait for a stock to come back down.

Here’s how it works:

- Pick a put strike price below the current price, say $95.

- Then go out in time to pick your expiration, say July 16th expiration.

- You then sell a put contract and receive a credit, in this case, around $140 per contract.

- Each contract controls 100 shares so you multiply the options price by 100.

- To place this trade, you need to set aside enough money to cover 100 shares of stock at the strike price.

- With a $95 strike, that’s $90 x 100 = $9,500

Now, here’s how the payout works:

- If we get to expiration (July 16th) and XYL remains above $50, the contract expires worthless and you keep the $65.

- If we get to expiration (July 16th) and XYL is below $95, you will get assigned (IE you will buy) 100 shares of XYL at $50. But you get to keep the $65.

The idea is pretty simple. You could put in a limit order to buy 100 shares of XYL at $95 and hope to get filled.

But, by selling a cash covered put, you get paid while you wait.

Now it’s not a lot as you’re earning $140 on $9,000 over 95 days, which translates into ~6.0% annually.

But, if the stock drops below $95 at expiration, then your average cost to purchase those shares is $95 – $1.40 = $93.60.

Our hot take

Chances are XYL should pullback in the coming months. And when the Fed goes to raise rates, they’ll probably take a major hit. But until then, it’s a strong stock in a strong trend with a strong story.