These days no matter what the Federal Reserve actually says, the markets respond like dogs sensing a piece of bacon coming their way. This is so for several reasons:

1) The world is vastly overleveraged, which terrifies investors and traders with even a modest historical perspective. The resulting insecurity makes them long for a higher power willing and able to keep the wolf of instability from the door.

2) The federal government understands that its ability to be all things to all constituents requires steadily increasing asset prices. To this end it has converted the financial markets from mechanisms for the efficient distribution of capital via accurate price discovery, into public policy tools for manipulating finance and politics. So the Fed’s job is no longer to maintain a stable playing field on which capitalism can work its magic, but to ensure rising asset prices forever.

To view the markets’ happy acceptance of this new reality, we need only look at what stock prices do when the Fed speaks. Here’s a CNBC report on the March 2015 Fed meeting:

Thank you, Janet Yellen! Stocks surge after Fed

The Federal Reserve has run out of patience. And Wall Street couldn’t be happier.

Stocks surged after the Fed’s latest statement was released Wednesday afternoon. The Dow was deep in loss territory and then jumped over 300 points in a matter of minutes. The index ended the day up 227 points and back above 18,000.

The S&P 500 and Nasdaq quickly popped as well. The Nasdaq even briefly surpassed 5,000 again and is not far from its all-time high from March 2000. Here’s why.

The Fed didn’t do anything unexpected. The market hates surprises.

What it means: But the central bank reassured the market that a rate increase was “unlikely” at its next meeting in April. That is not a surprise either. Wall Street has been betting on rates starting to go up in June or later.

The Fed also issued new forecasts. It lowered its 2015 and 2016 outlook for gross domestic product (GDP) slightly. It also cut its inflation forecasts and predicted that the unemployment rate will fall further than it thought a few months ago.

All this suggests the Fed will take a slow and steady approach to rate hikes. That should calm down investors who had been worrying the Fed would boost rates too quickly.

To summarize, the Fed didn’t actually do anything but did say some warm and fuzzy things implying that the financial crisis was still a ways off. The fact that Fed governors, based on their extensive paper trail, know little or nothing about the future is irrelevant next to the promise of a few more months of easy money.

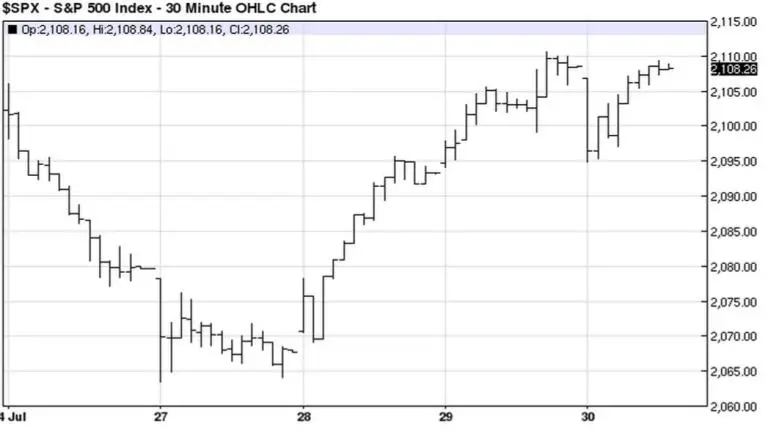

Now fast forward to this week, when the Fed met and again said very little. It might bump up the Fed Funds rate by a tiny amount in September or it might not depending on the data generated by the economy in the meantime. In other words, the story is unchanged from the previous five or six statements.

The markets, however, loved the soothing, adult cadences. Note how the S&P 500 was falling hard until the Fed started meeting on the 28th, and then bounced nicely in anticipation of the accustomed reassurance.

So what does this mean? Mostly that in today’s decadent, leverage-saturated financial system, markets are now largely branches of government policy. Which history teaches is a very temporary situation that will be remedied when the laws of economics now being defied reassert themselves with a vengeance. When they do, the soothing words will be replaced by capital controls, bank bail-ins and devaluation, and the transition will be complete.