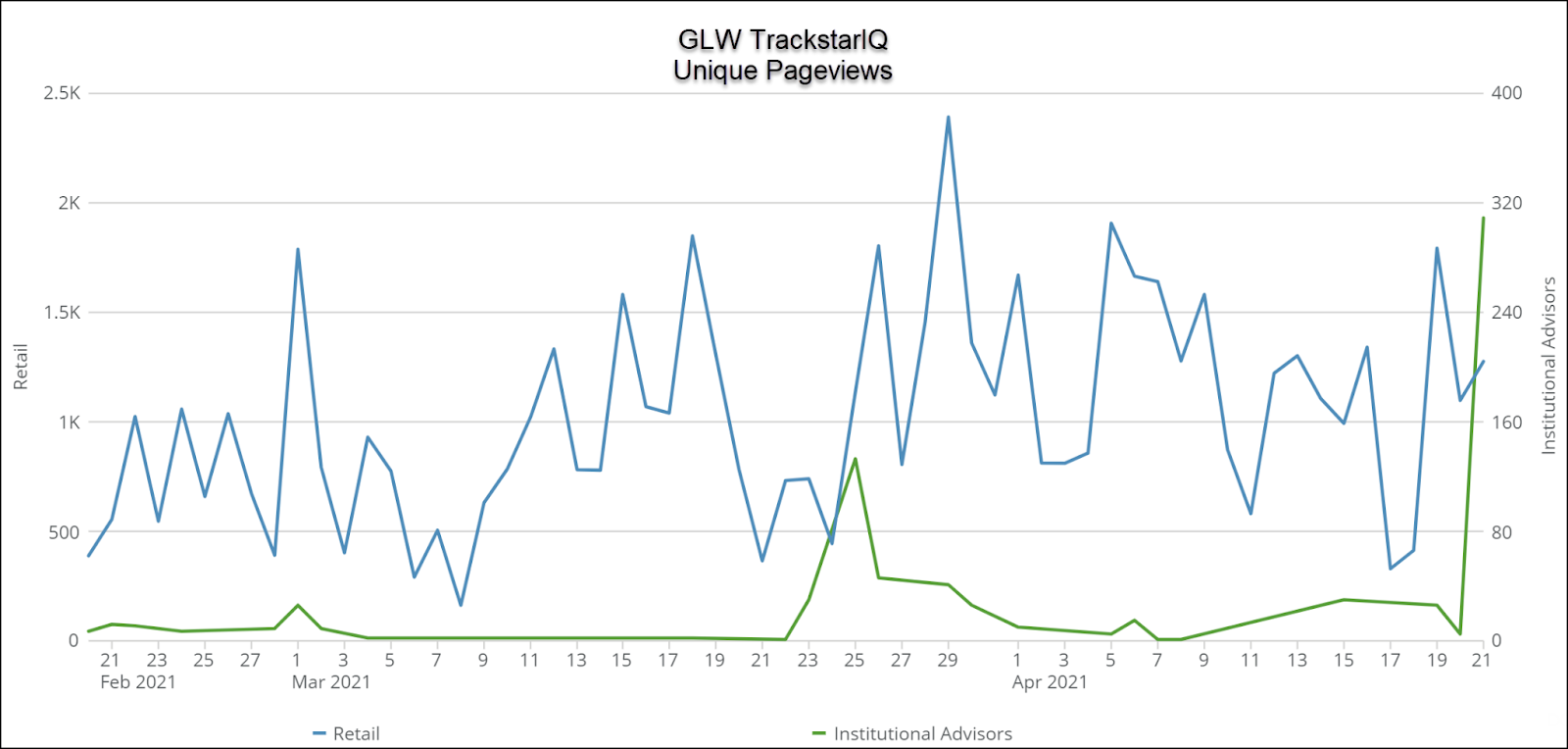

Institutional advisors may know something we don’t.

Out TrackstsrIQ data had seen search volume for Corning Inc. increase over 1000% in the last couple of days.

The question is, why?

Why would anyone care about a company that’s been around since 1851?

We dug into the financials to find out why.

Who is Corning?

Corning is all about glass.

For over 170 years, the company innovated in the sector, making it a leader in both product and size.

You’ve likely encountered their products on everything from mobile phones to smartwatches.

Corning weathered the pandemic fairly well, with a less than 2% decrease in revenues.

And from a balance sheet perspective, they’re fairly healthy.

Given its size, the company benefits from centralized R&D, using its massive scale and limited product lines to monetize its innovations.

The big driver coming up is 5G networks.

Most people don’t realize it, but Corning’s largest revenue segment is optical fiber, accounting for over 30% of their sales.

Upcoming earnings

Q4 earnings surprised analysts by 41.6% (which again – how are analysts this bad).

These same analysts expect a 23.7% revenue increase year-over-year with a 110% increase in earnings.

Both of these are reasonable given the volatility in the industry.

Corning’s business correlates with the broader economy with a bit of a boost from the growth niches it serves.

Value stinks

As seems to be the common theme these days, there isn’t much value here.

Shares currently trade at a price to earnings (P/E) ratio of 95.36x.

Even if they get back to pre-pandemic levels, you’re still at +45x P/E, which is extremely rich given the size and growth of the company.

Generally speaking, the company pulls in annual revenue growth of around 7%, which is only a touch above the S&P 500’s weighted average of 5%.

The good news is that they have a very strong balance sheet with some debt that’s offset by a decent amount of cash, receivables, and inventory.

Our hot take

Shares more than doubled off the pandemic lows and are up more than 50% from pre-pandemic levels.

Advisors have this one wrong here. Even if the stock pops off earnings, the recent trajectory based on the fundamental value isn’t sustainable.