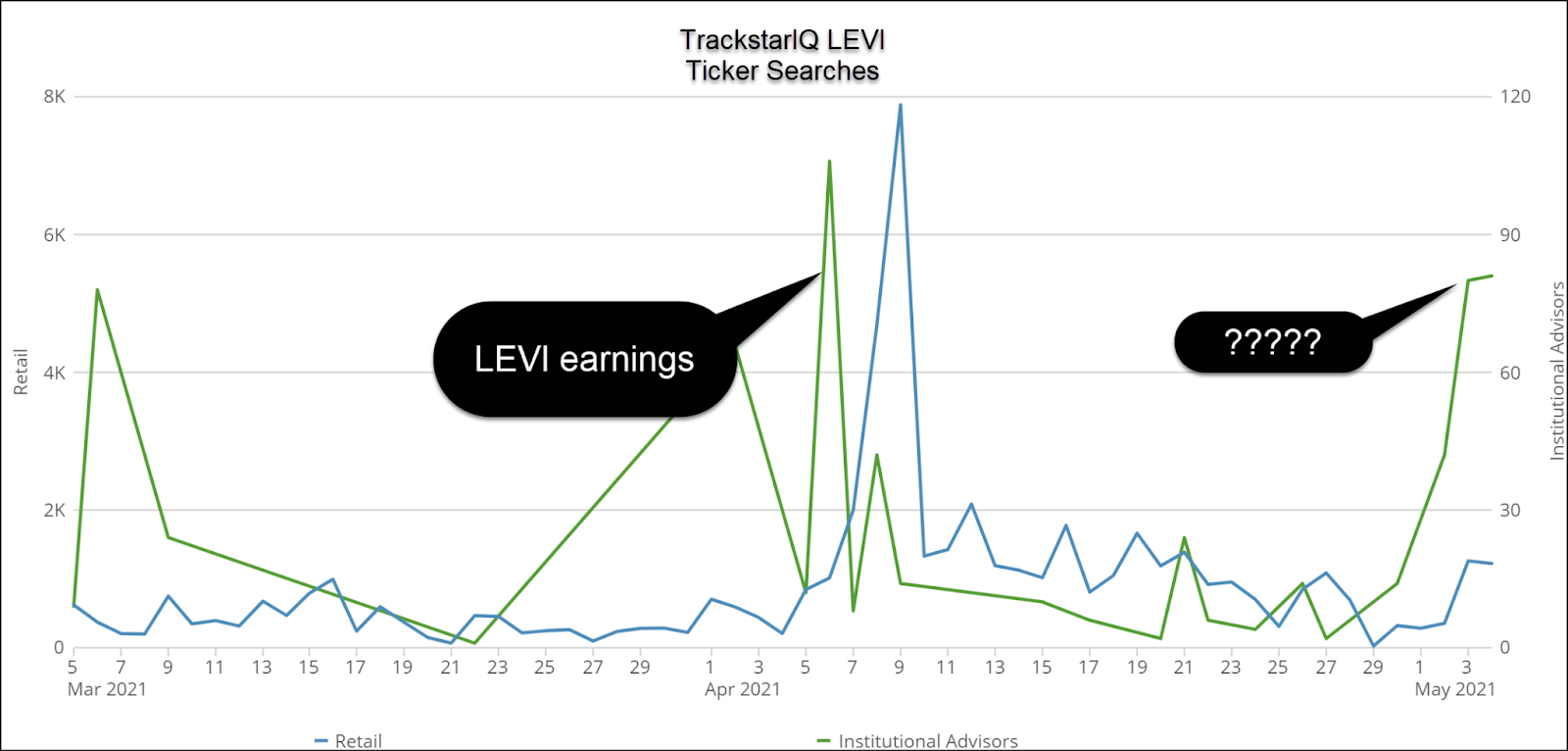

Something interesting came through our TrackstarIQ data recently.

Searches for Levi Strauss & Co. (LEVI) spiked nearly a month after earnings.

It got us curious.

So we dug into the details.

And let’s just say, we might have found one of the cheapest growth stories out there!

But we know you’re skeptical.

So give us five minutes to walk you through our case and see if you don’t agree.

The pandemic and Levi Strauss

We won’t bother covering who Levi Strauss is. They make awesome jeans. If you didn’t know that, we feel sorry for you.

What you may not know is the company remained private from 1985 until February 2019. Before that is was public starting in 1971.

Levi built an iconic American brand so much so that authentic pairs smuggled into Communist Russia in the 1970s-1980s would fetch hundreds if not thousands of dollars.

Unfortunately, the company operates many brick and mortar stores where the pandemic exacted its heaviest toll.

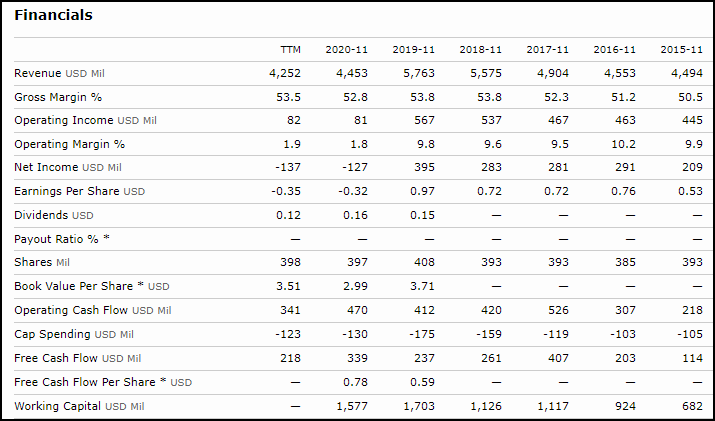

Until Covid, LEVI delivered fantastic growth and steady margins.

Source: Morningstar

In order to save upwards of $100 million, corporate made the decision to cut 700 office jobs.

The hidden value

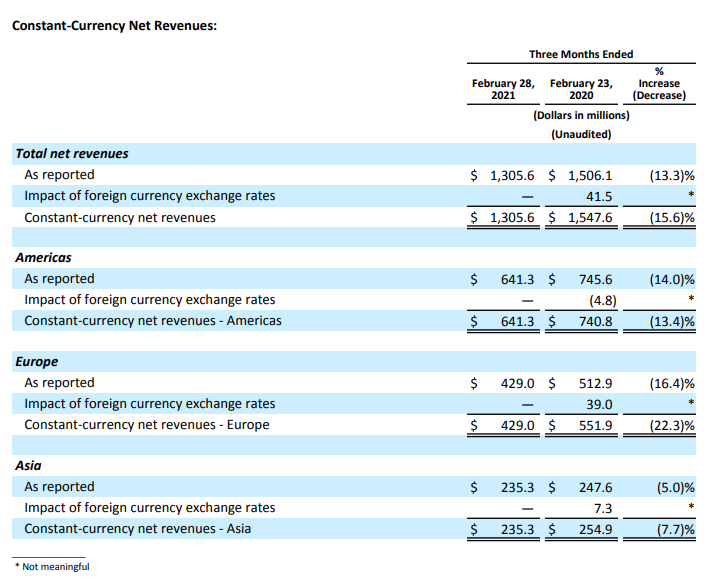

LEVI segments their business into three geographies: Americas, Europe, and Asia.

Let’s take a look at those:

Notice how the heaviest hit came in Europe and the smallest in Asia.

It’s not a far-fetched assumption that sales will return to pre-pandemic levels in these two geographies in the coming months.

And if you look at their performance by quarter, the company turned a profit every quarter but Q2 of 2020.

Prior to the pandemic, LEVI hit nearly $1 per share in EPS.

At their current price, that would be around a 30 price to earnings ratio (P/E).

However, if we look into the future and consider their five-year average growth of around 4%, things start to look rather cheap. Plus, they already took a massive one-time restructuring charge in Q2 of 2020.

Heck, their last quarter showed a $0.35 EPS. At that run rate, they would only be at a 21.4x P/E ratio, before revenue growth!

Our hot take

Compared to the rest of the market, LEVI looks pretty darn cheap. The long-term debt they added was significant. But, they’ve already begun to pay it off.

While the dividend isn’t much at less than half a percent, it’s better than a treasury bill.

Keep an eye on this one. Even near all-time highs, it’s got a lot of potential.