You know what company barely suffered in the pandemic?

JB Hunt Transport Services (JBHT).

Freight companies operate whether we go to work or stay at home.

The only thing that really changes over time is HOW they deliver their cargo.

What made us suddenly think about trucking?

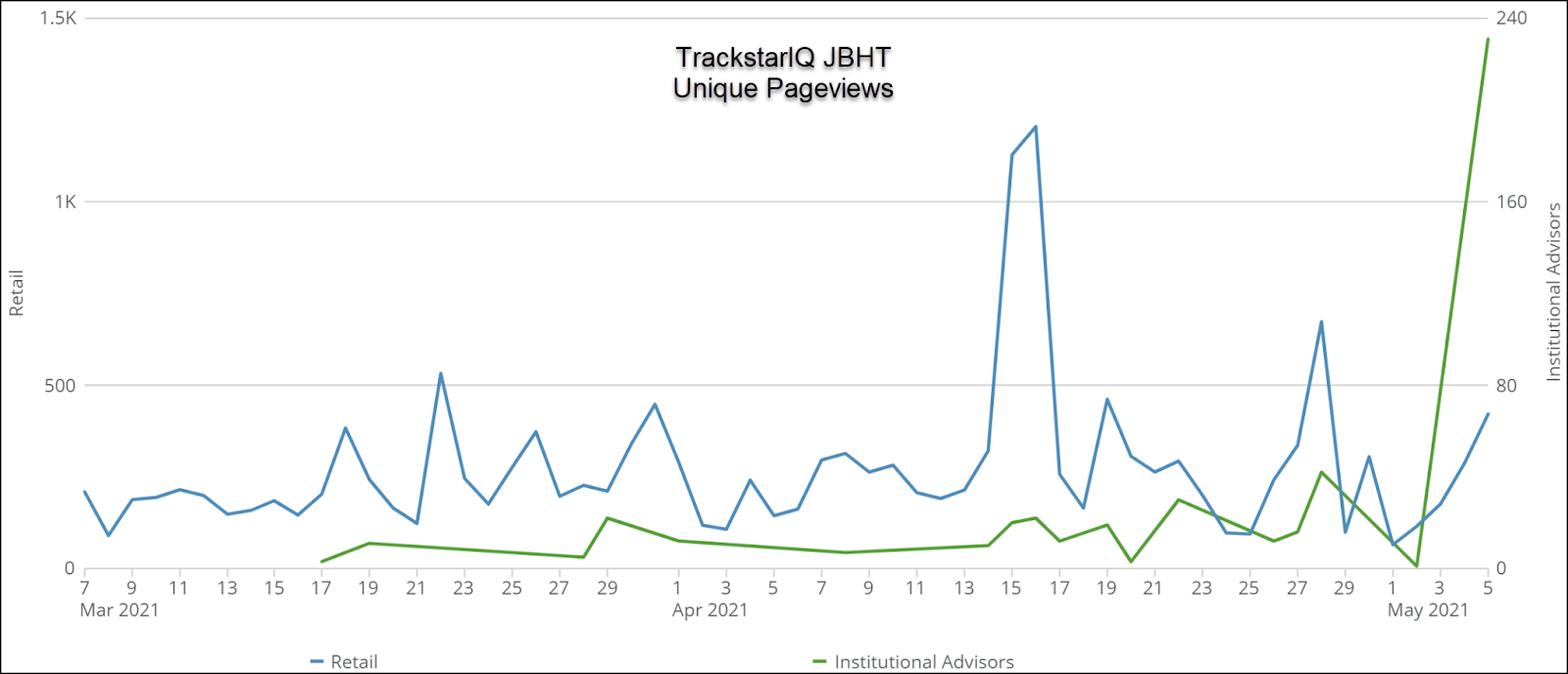

Unique pageviews for institutional advisors spiked in our TrackstarIQ data the last few days.

From what we can tell, there hasn’t been any news of late, save for earnings mid-April.

So, do these guys know something we don’t?

We dove into the details of JB Hunt. And we found they’re way less about trucking than you might think.

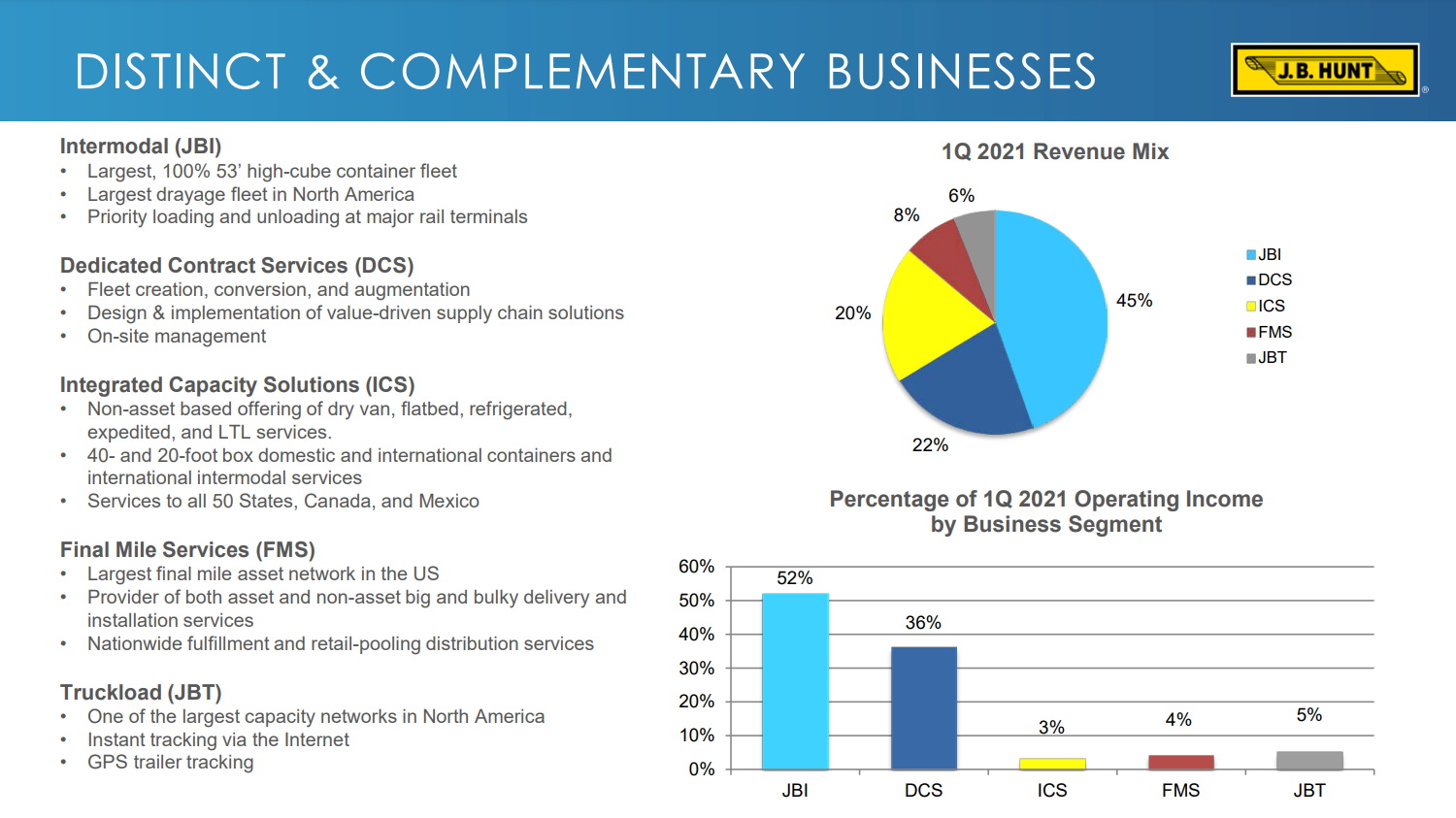

JB Hunt’s revenue split

Fun fact – JB hunt makes up nearly 50% of their revenues, and more than 50% of their profits from intermodal freight.

If you’re not familiar with the term, intermodal freight (JBI) refers to shipping that goes typically through rail with trucks on either side of the hubs to make delivery.

The old notion of the trucking convoy long-haul is a thing of the past.

Long-distance truckloads only make up 6% of their revenue and 5% of their operating income (JBT).

The rest is set up through dedicated fleets that operate within ~150 miles of a customer (DCS), brokerage style services including 3rd party logistics (ICS), and retail store distribution (FMS).

What you’ll notice is that the ICS division accounts for 20% of revenues but hardly any operating income.

In fact, the ICS and FMS divisions rarely turn a profit at all.

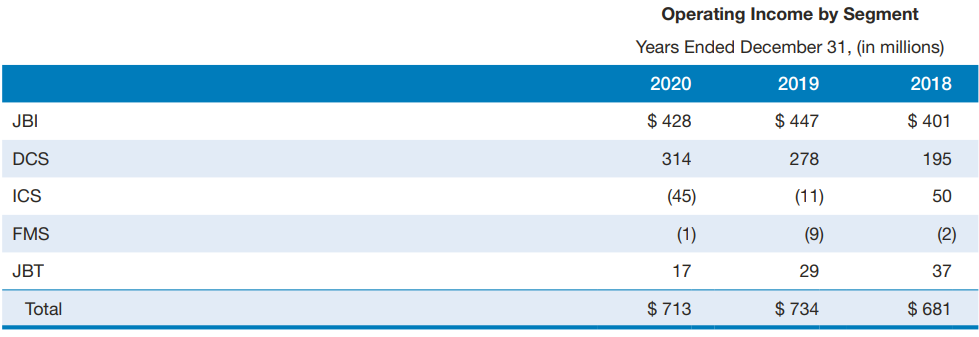

2020 performance

What’s notable is how well JB Hunt did during 2020. You’ll notice that their operating income was only down slightly from 2019.

The company certainly benefited from cheaper fuel prices.

But, they continue to grapple with driver shortages that have plagued the industry for the past several years.

It’s also worth noting that revenues actually INCREASED in 2020 by 5.15%.

Not too shabby all things considered.

Valuation and outlook

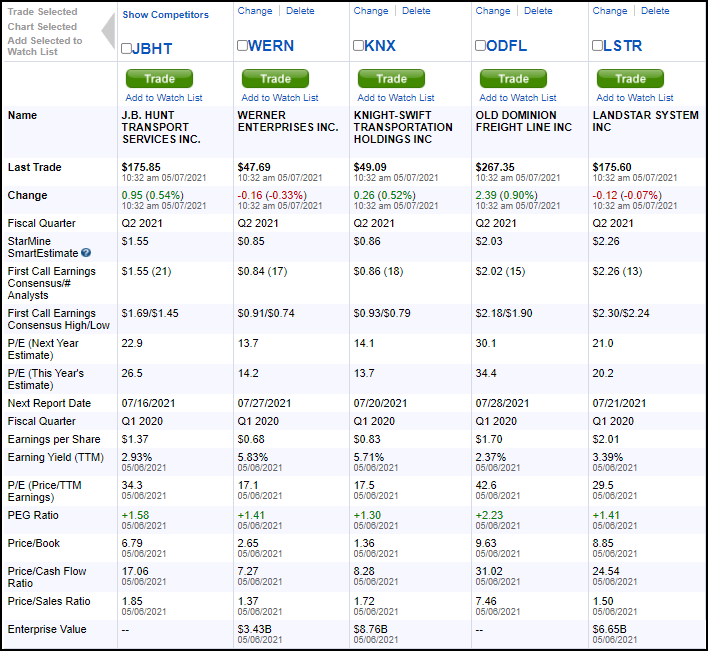

Comparing JB Hunt to its peers and the market, shares aren’t cheap.

Current price-to-earnings ratio (P/E) comes in higher than peers looking at the trailing 12 months, the current year, and next year with the exception of Old Dominion Freight Lines (ODFL).

While they are the best in class, the stock has been priced accordingly.

Our hot take

JB Hunt is a great company, no doubt. But from a price to valuation standpoint, it’s quite rich compared to its peers.

However, looking at next year’s estimates, you could make an argument that shares might be underpriced.

Still, it’s probably worth waiting on a pullback to get a cushion of comfort to work with.