|

Proprietary Data Insights Financial Pros Top Airline Stock Searches December

|

|

Stock Analysis |

Southwest Flies Above The Rest |

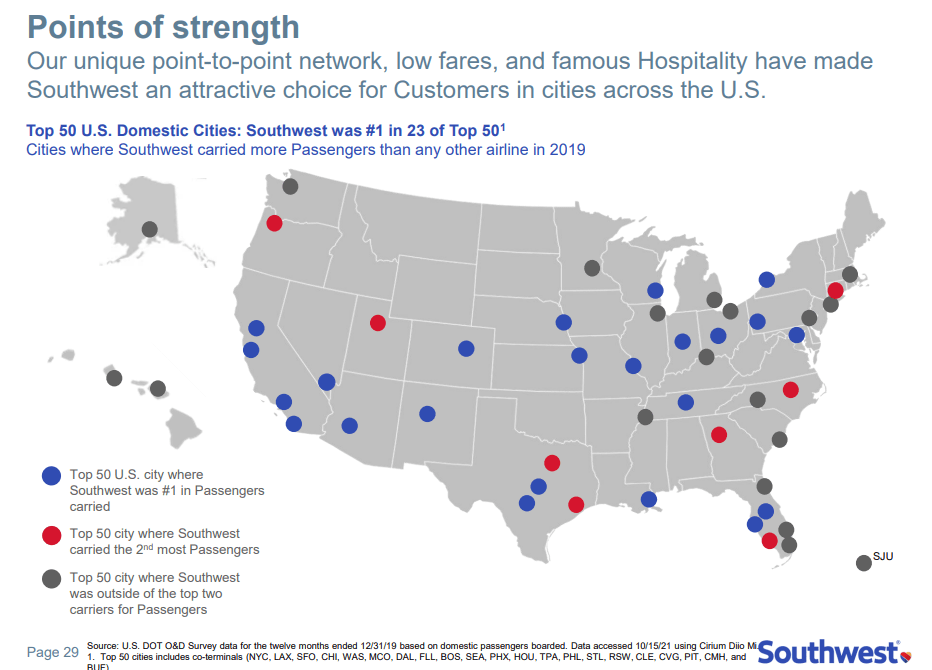

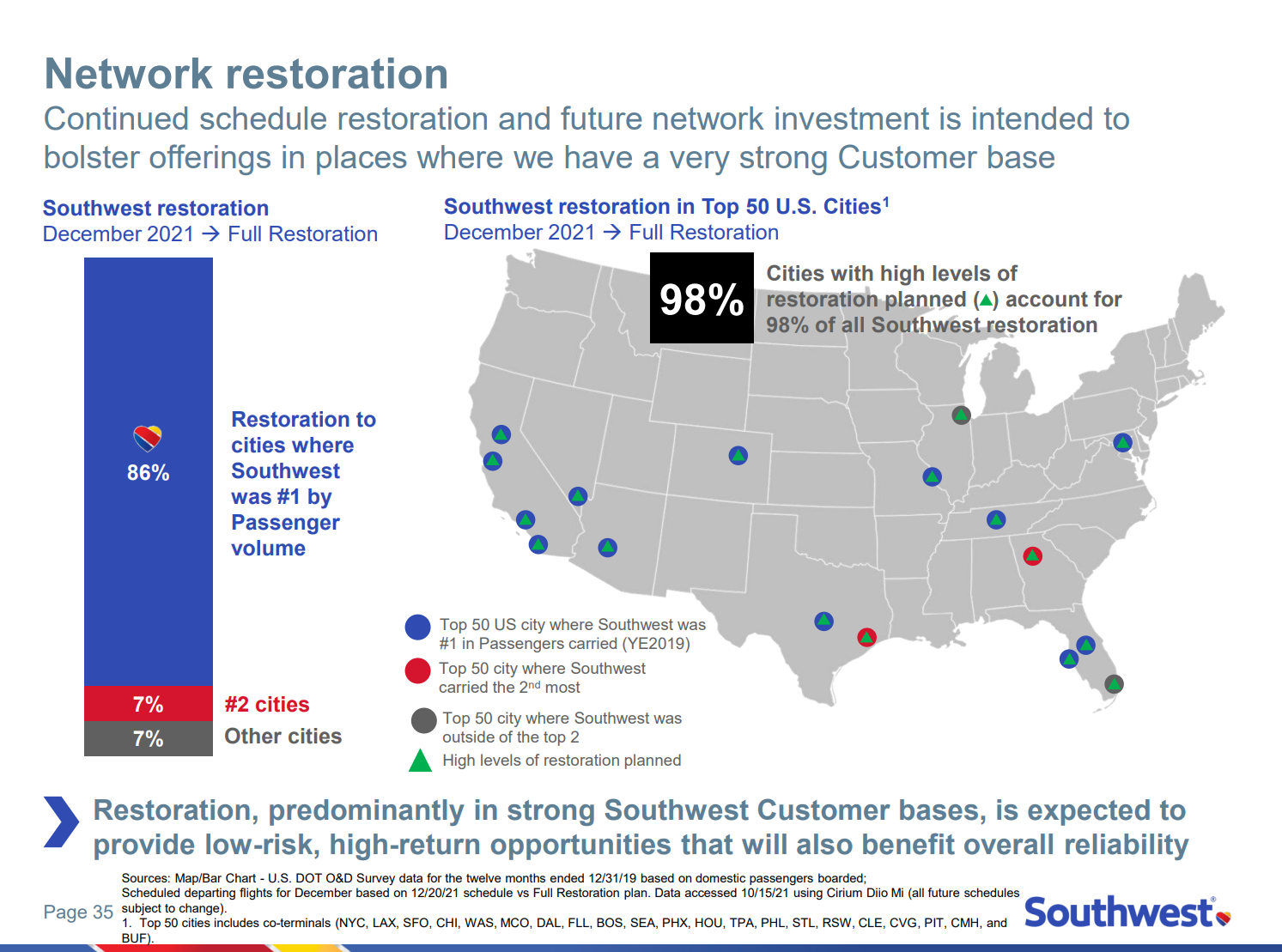

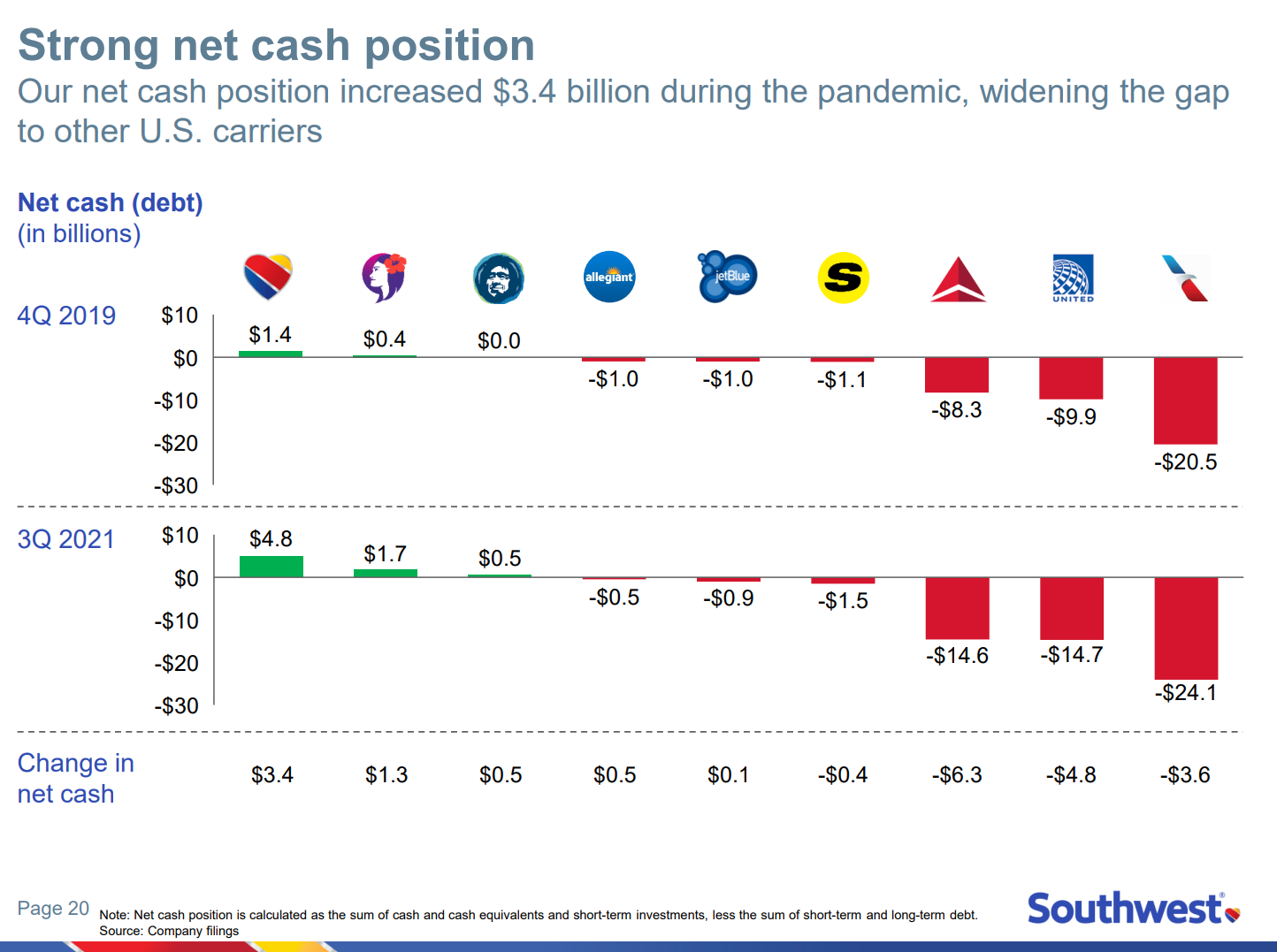

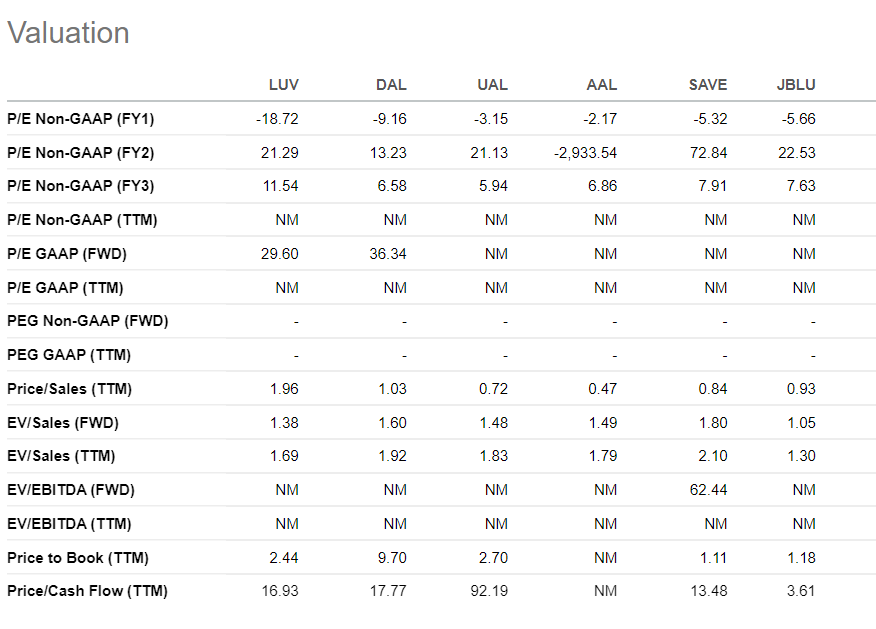

Let’s face it. Back in March 2020, no one knew if airlines would survive. Many of us thought the industry would get a bailout like the autos did back in the Great Recession. Thankfully, nearly all survived the pandemic and returned to profitability. Yet, most airline stocks still trade at a discount to pre-pandemic levels. Southwest Airlines (LUV) is our favorite of the bunch. With operational excellence, a continual focus on employees, and fewer international routes, the Dallas based airline could climb by more than 50% in the next year or so. As the top airline search amongst financial pros this month, we know there are a lot of eyes on the company. And we think now may be the ideal time to get in. Southwest Airline’s Business They fly airplanes. Great, so how is that different from the others? Back in the day, Delta (DAL) and other airlines created and worked the hub and spoke model. You would fly Delta and likely be routed through their Atlanta hub before reaching your final destination. Southwest Airlines went for point-to-point travel. Coupled with zone boarding rather than assigned seating, customers see less crowding and more on-time departures. Additionally, the company focuses on creating fun customer experiences with jovial staff that are attentive and congenial. While airlines like United (UAL), American (AAL), and Delta service 369, 350, an 325 international destinations respectively, Southwest only hits 101, with most in the Caribbean, Latin America, and the north part of South America. Covid hit the industry pretty hard, and Southwest was no exception. The company pared back offerings while doing what it could to fully utilize staff and reduce cash burn. Now, the company is focused on restoring its network, focusing on cities that represent key customer bases. Additionally, the company expanded its network into Hawaii and 18 new airports that it plans to continue as it restores service. Lastly, Southwest plans to implement a new Revenue Management System (RMS) to improve processes and maximize revenue through enhanced passenger demand forecasting while adding a 4th fare product to it’s line of fares such as ‘Wanna Get Away.’ Financials When we look at Southwest’s financials, we want to know how long it will take the company to return to its former glory and can it go further. Revenues will take time to climb back as total air travel remains subdued. Gross margins aren’t a good measure for airlines as much as operating margins. Now, what we like is that operating margins turned positive over the last 12 months which is no small feat. Plus operating and free cash flow pulled a 180, both turning positive. This bodes well for the airline as it ramps up operations. We don’t believe it’s a question of if Southwest can get back to its former profitability but when. Right now, that’s entirely dependent on demand stabilizing more than anything else. We expect Covid related travel restrictions to ease and become more uniform in the coming year. That provides Southwest more certainty and a better chance to plan. Lastly, we want to show you a slide from Southwest’s last investor presentation. We feel this slide is important because cash on hand will be a key factor determining growth in the coming years. Companies with more cash can invest where they find opportunities. Those in the hole cannot. Valuation As you might have guessed, none of the airlines have positive earnings at the moment. However, there are some telling valuation metrics. For starters, only Southwest and Delta are expected to deliver positive earnings next year. That’s a big deal when you consider how bad things were last year. What’s interesting is that although Southwest has the highest price-to-sales ratio, it has the lowest enterprise value (EV) to sales ratio looking forward. That implies that when you take into account debt and cash (EV), Southwest is a better value. Lastly, although Southwest isn’t the lowest price to cash flow over the last 12 months, its forward price-to-cash flow (not shown above) is 12.65x. That’s pretty solid given the difficulty other airlines like American face generating positive cash flow. Our Opinion – 8/10 Southwest is the best-positioned airline in our opinion. The company’s domestic focus will help it increase profitability faster than airlines that rely on international routes. More importantly, Southwest focuses heavily on its staff, which given the current shortages, is vital to the company’s future success. |