|

Proprietary Data Insights Top Capital Markets Stock Searches This Month

|

||||||||||||||||||

|

A Brilliant Job Interview Tactic A few days ago, a friend reminded us of what the CEO of Charles Schwab (SCHW), Walt Bettinger, used to do (and maybe still does?) when interviewing job candidates. He would arrive at the restaurant early and pull the server aside. He’d ask the server to mess up the order of the person who was about to join him. In return, he promised to tip handsomely. Then, when the interviewee received the wrong order, Bettinger assessed the person’s response. Did they:

Of course, the right answer is calm acknowledgement followed by understanding. The wrong answer is to act like a jerk in any form. But saying nothing at all, according to Bettinger, could indicate somebody who’s too timid, lacks attention to detail, and doesn’t care to make things right. As in life, things go wrong at work. When they do, the best employees respond with tact, class, and problem-solving capacity. The Juice loves these types of stories. Call them teachable moments. We especially like this one because it got us thinking about one of the things Charles Schwab specializes in – retirement planning – and how we might respond on the uncertain, even frightening road to retirement. Because we’re going back to personal-finance-meets-investing basics to start 2023. And because we touched on the importance of often maligned Social Security in retirement yesterday, we figured we’d continue the theme and consider retirement from a different angle today. |

|

Retirement |

Some Different Advice About Funding Retirement |

Key Takeaways:

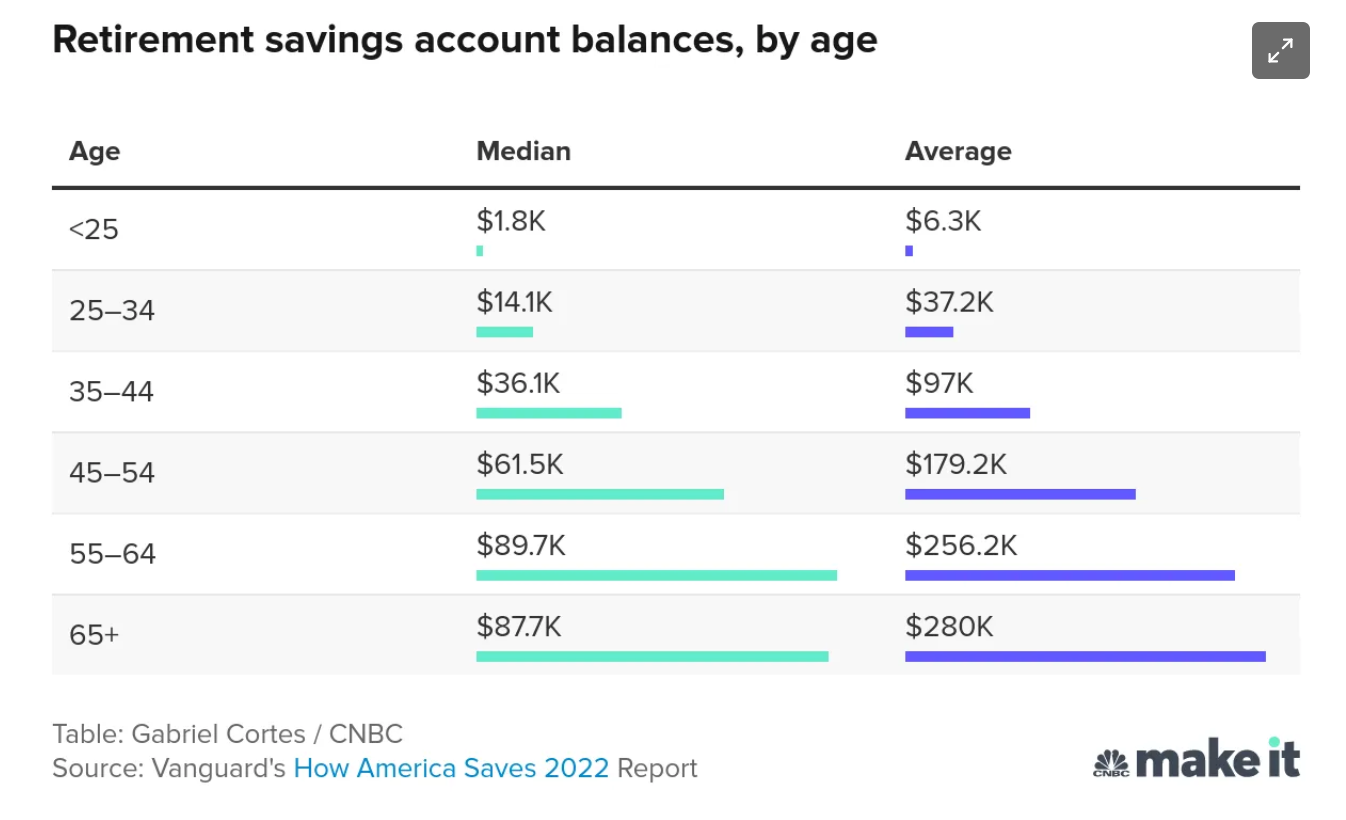

Here’s the reality on retirement: Across age groups, we don’t have enough money saved to fund it. Forget about a comfortable retirement. We’re talking retirement, period. Which underscores the importance of Social Security. While it might be a handy supplement to some or icing on the cake for others, it’s a lifeline for countless others. Imagine hitting 62 with $89,700 in your retirement account, the median amount for that age. If you want to work less or quit altogether, and you have no other meaningful sources of cash, you’ll likely be collecting Social Security pronto. Source: CNBC/Vanguard In money article after money article, you see the same advice about what is a flat-out retirement crisis. The investing gurus run the math and tell you how much more you need to save each month based on your age, what you expect to spend in retirement, and how far behind you are at the moment. How to catch up. But if you’re struggling to save and invest, saving and investing more might be futile. It can be annoying to be told only to double down on a strategy that hasn’t worked out so well thus far. So, beyond factoring Social Security into the mix, what can you do? Pay Off Your Mortgage The next-worst thing to going into retirement light on savings is going in with large, fixed monthly expenses. If you have a mortgage or big car payment, get rid of it ASAP. Lower your cost of living, particularly on your biggest expenses. Once you do this, the money you do have saved and the income you might be forced to earn will take you further. Which leads to… Estimate Your Personal Financial Runway We’ve gone back to basics because we often don’t think about the obvious when we face a complicated problem. Like the job candidate who doesn’t address the wrong order, we put our heads in the sand, ignore reality, and do nothing. As if the situation will fix itself. Or we freak out and let agitation and anxiety take over. We don’t go beyond the headlines about needing more than $1 million to retire. Instead, we let them paralyze us, freak us out, or a mix of both. Look at how much money you have saved, then consider how much you absolutely must spend each month in retirement. Once you take things like mortgage and car payments out of the mix, the number you need to retire with might be less intimidating. Let’s say you have $500,000 saved and can get by spending just $2,000 a month. That’s 250 months, or 20.8 years, of personal financial runway. You might outlive that nest egg, but when Social Security and some form of employment enter the mix, having $500,000 saved in your 50s or 60s doesn’t seem so dire. You Might Have to Make a Drastic Move Maybe you have a mortgage balance or a rent payment. You might have to part with a significant chunk of your nest egg to pay off the loan or buy a place for cash so you can quit renting and eliminate that monthly outlay. This might require moving to a less expensive area. Increasingly, people are leaving the United States for less expensive terrain in Mexico, parts of South America, Asia, and Europe. Places where your money takes you much further, which, quite possibly, can elevate your quality of life. At the same time, you might have to continue working or take on part-time work in relative old age, like it or not. The earlier you start thinking about this, the better. What type of work can you do that’s easy enough on your mind and body that you can do it during the traditional retirement years? Better yet, can you start developing a source of passive income today to help sustain you tomorrow? The Bottom Line: Saving more isn’t always the most effective retirement strategy when you’ve fallen short of savings goals or never had any to begin with. Instead, you might have to start thinking of ways to lower your overhead or alternatives to full, traditional retirement. In the coming weeks, The Juice will expand this line of thinking and consider ways to structure retirement when you don’t have a million bucks or more ready and waiting in the safe of a condo that overlooks a golf course. |

|

News & Insights |

Freshly Squeezed |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |