|

Proprietary Data Insights Financial Pros Small-Cap AI Stock Searches in the Last Month

|

|||||||||||||||||||||

|

Information Technology |

Don’t Buy This AI Stock Yet |

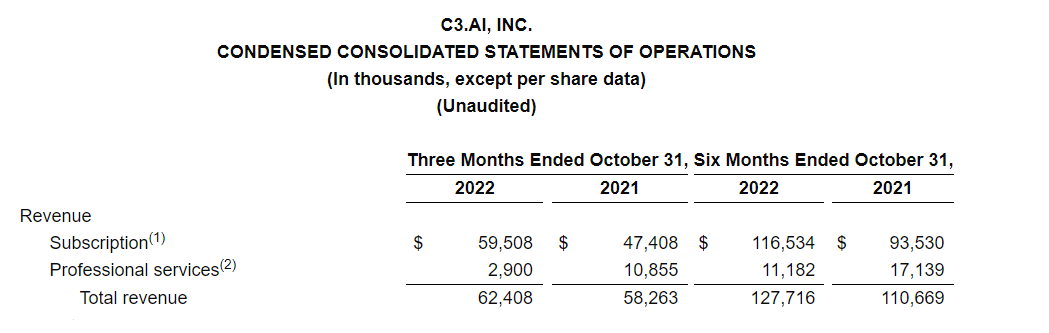

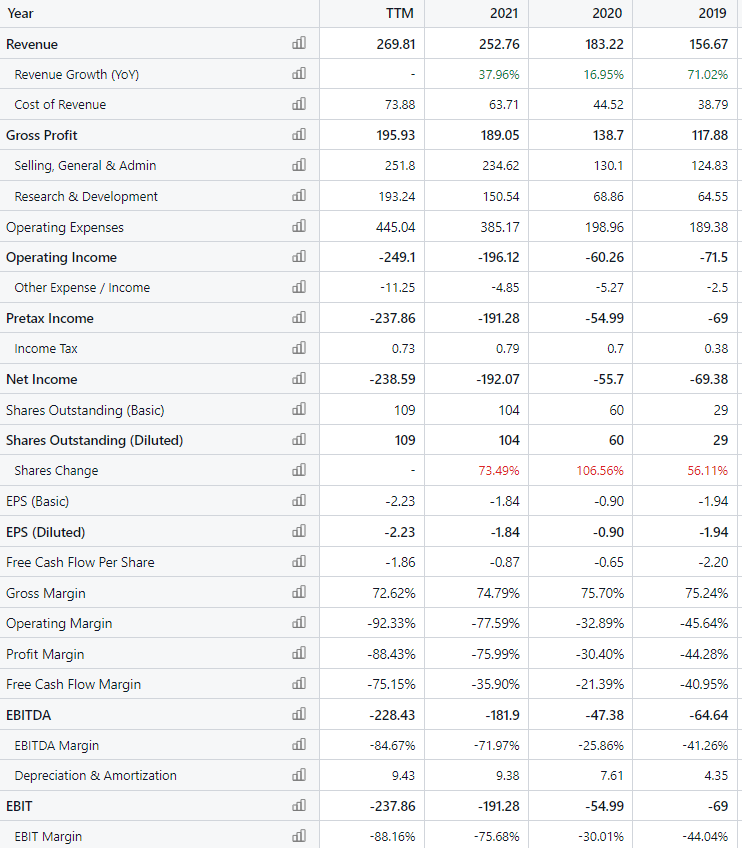

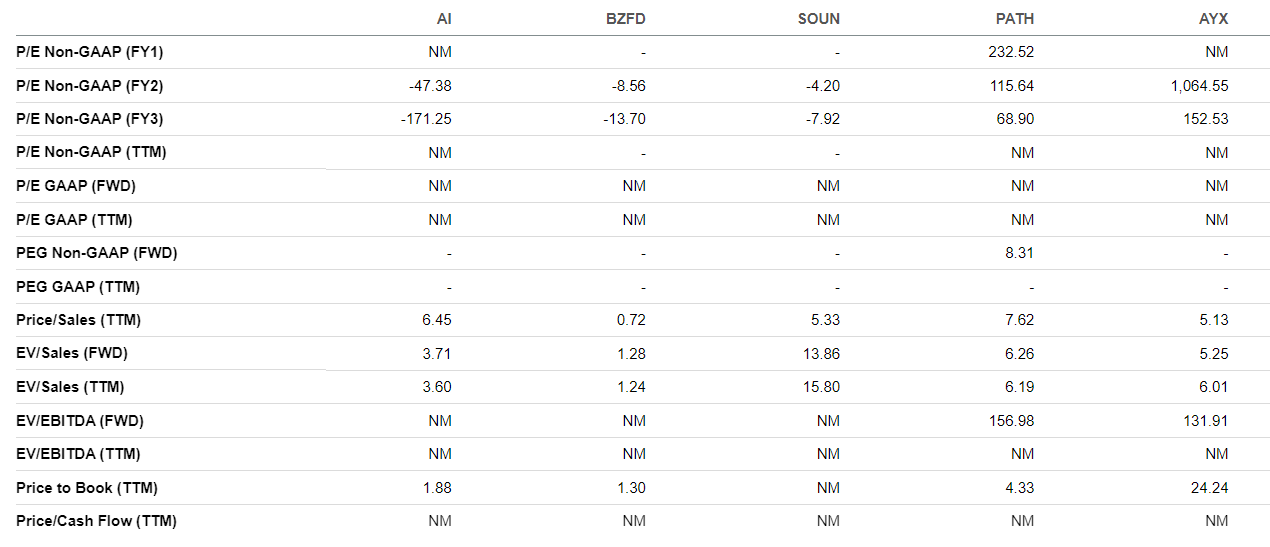

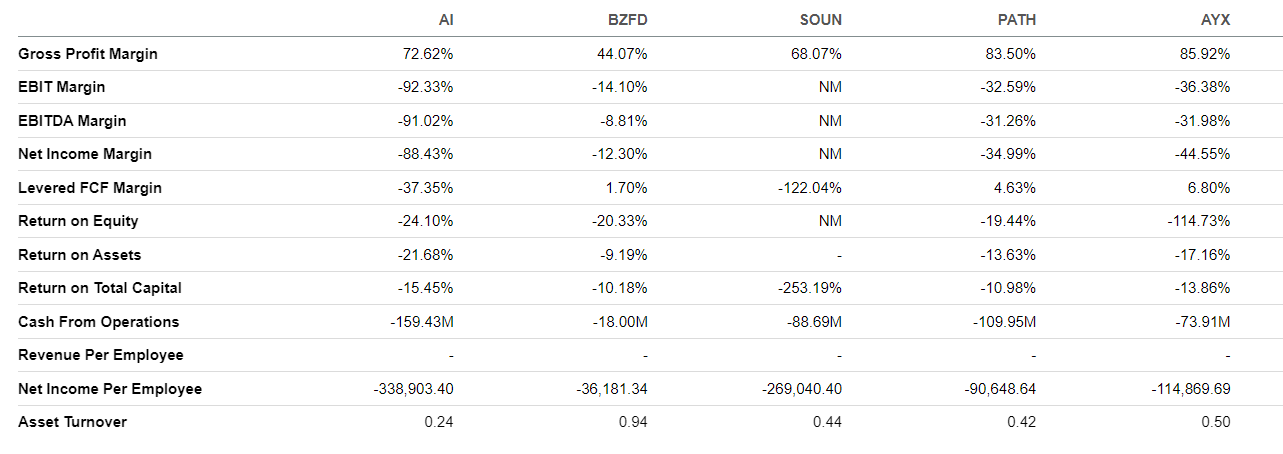

Facebook took 10 months to reach 1 million users about two decades ago. At the end of 2022, OpenAI’s ChatGPT AI platform shattered records by reaching the same milestone in just five days. The AI sector is soaring, with traders bidding up shares of anything related to AI. C3.ai is leading the charge with its ticker symbol, AI. With a nearly 100% jump in January 2023, it’s gaining significant momentum among financial pros, according to the latest search data from Trackstar, our proprietary sentiment indicator. Financial pros’ total monthly searches for the stock went from just a few hundred a couple months ago to nearly 1,000 in the last 30 days. C3.ai is one of the hottest stocks right now. But is it just a trend or a company investors can rely on for the long term? C3.ai’s Business C3.ai provides enterprise AI software for organizations to build, deploy, and operate AI applications at scale. Its platform allows customers to create custom AI applications for various industries, including healthcare, energy, and financial services. The unique software combines data management, machine learning, and cloud deployment to help companies accelerate their AI initiatives. C3.ai touts impressive partnerships with big names like Raytheon, AWS, Intel, Google, Microsoft, Baker Hughes, and FIS. It breaks its revenues into two segments: subscription and professional services. However, management says it will transition to a consumption-based revenue model. Instead of trying to land large subscription contracts, the new model will allow clients to access C3.ai’s tools at a lower entry price and charge them based on usage. In December, the company reported that its subscription revenue for Q2 2023 (how it classifies the quarter that ended in October) hit $59.5 million, an increase of 26% compared to $47.4 million one year prior. Professional services delivered $2.9 million in Q2 2023, a significant drop from the year before. Source: C3.ai The company made $62.4 million combined in the same quarter, a 7% increase from the previous year. GAAP gross profit hit $41.7 million, and non-GAAP gross profit hit $47.8 million, representing a 67% and 77% margin, respectively. Despite a GAAP net loss per share of $0.63 and a non-GAAP loss per share of $0.11, C3.ai is financially solid, with $858.8 million in cash and investments. It’s poised to continue investing in growth and innovation in the enterprise AI sector. The firm made headlines yesterday when it announced the launch of the C3 Generative AI Product Suite with the release of its first product, C3 Generative AI for Enterprise Search. Shares of the stock rallied a whopping 21.8% on the news. Financials Source: Stock Analysis C3.ai boosted revenues from $91.6 million in 2018 to $269.8 million in 2022. But its operating expenses grew faster, from $97.3 million in 2018 to $445.0 million in 2022. With a $2.19 billion market cap and $858.8 million in cash, the company has an enterprise value of $1.3 billion. Its long-term debt is modest at $31.8 million. Plus, the company’s current ratio of 8.1x gives it plenty of breathing room as it transitions to a consumption-based revenue model. But the company burns through over $150 million in cash from operations annually. Valuation Source: Seeking Alpha C3.ai trades at a price-to-sales ratio of 6.5x, relatively high compared to other small-cap AI stocks. For example, BuzzFeed (BZFD) is at 0.7x, SoundHound AI (SOUN) is at 5.3x, and Alteryx (AYX) is at 5.1x. C3.ai’s P/S ratio is, however, lower than UiPath (PATH)’s 7.6x. Yet the AI ticker looks more competitive from an EV-to-sales standpoint thanks to the company’s large cash position. It has an EV-to-sales ratio of 3.6x, notably lower than SOUN at 15.8x, PATH at 6.2x, and AYX at 6.0x, but not quite as low as BZFD at 1.2x. Profitability Source: Seeking Alpha Wall Street adored the software industry for many years before last because of its high gross profit margins and ability to retain customers. C3.ai is no exception with a gross profit margin of 72.6%, higher than BZFD at 44.1% and SOUN at 68.1%, but lower than PATH at 83.5% and AYX at 85.9%. Stocks like AI got crushed in 2022 because they weren’t profitable. With an EBIT margin of -92.3%, it’s hard to get excited about the company. While its peers aren’t as bad, they aren’t good either. BZFD has an EBIT margin of -14.1%, SOUN’s is NM (not meaningful), PATH’s is -32.6%, and AYX’s is -36.4%. AI’s net income margin of -88.4% is also a tough pill for investors to swallow. Again, its peers aren’t exactly knocking it out of the park, but they’re not nearly as awful. BZFD has a net income margin of -12.3%, SOUN’s is NM, PATH’s is -34.9%, and AYX’s is -44.5%. Growth Source: Seeking Alpha C3.ai grew 27.2% YoY, which wouldn’t be awful if it was already profitable. But the company’s revenue growth has been slow relative to how much money it loses. That’s not a good sign, especially considering it’s changing its revenue model, which will likely slow the company’s growth for at least a few quarters. Some of its peers are growing faster, like AYX at 39.2%, SOUN at 32.2%, and PATH at 28.3%. BZFD is at 19.4%, the lowest among the group. Our Opinion 3/10 C3.ai stock had an incredible run in January, gaining nearly 100%. Shares are at $19.80, significantly off from their all-time high of nearly $180. The stock’s recent surge isn’t based on the company’s fundamentals but on the hype ChatGPT has. The problem is C3.ai hasn’t figured out how to monetize its business. Analysts at Morgan Stanley believe the company is a takeover target. But that’s not a good reason for investors to jump into the stock. We’d like to see C3.ai string together a few quality quarters of growth before we consider it a buy. For now, it’s a stock worth trading but not worth owning as an investment. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |