|

Proprietary Data Insights Financial Pros Mega-Cap Tech Stock Searches in the Last Month

|

|||||||||||||||||||||

|

Technology |

😫 AMZN’s Dreadful Q4: Buy Now? |

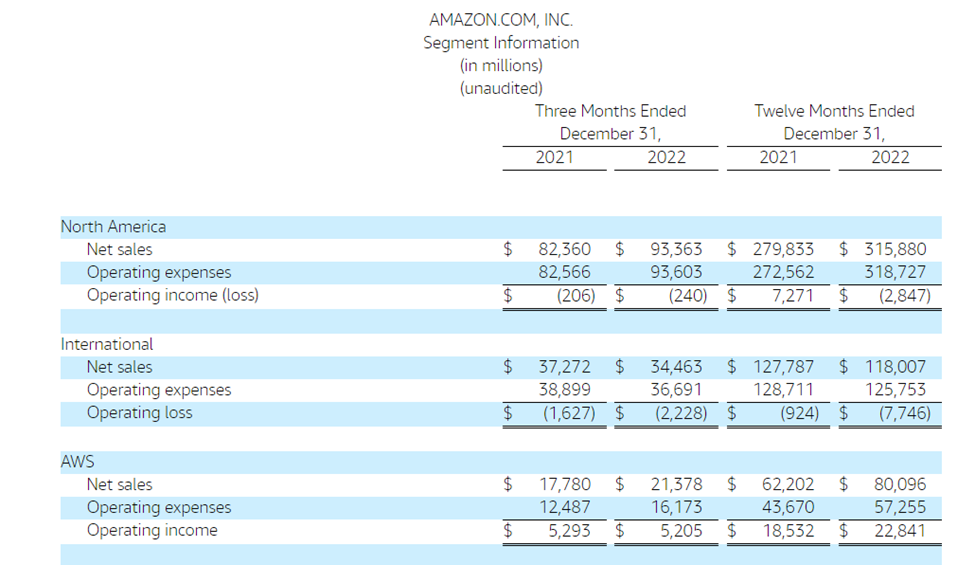

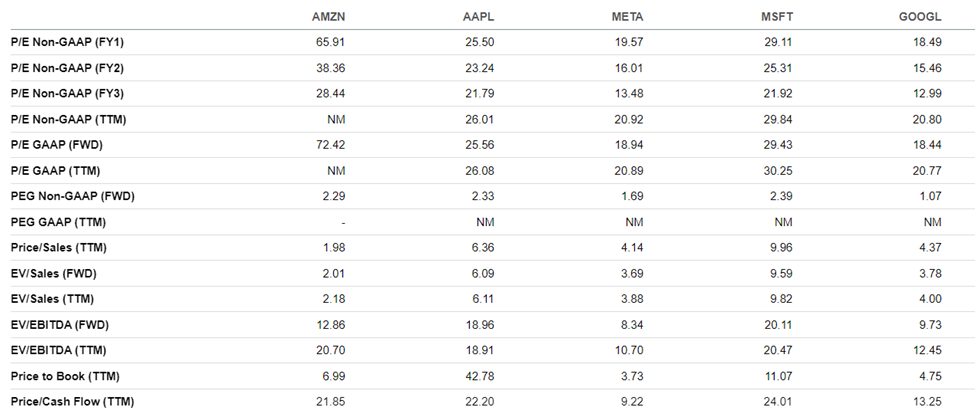

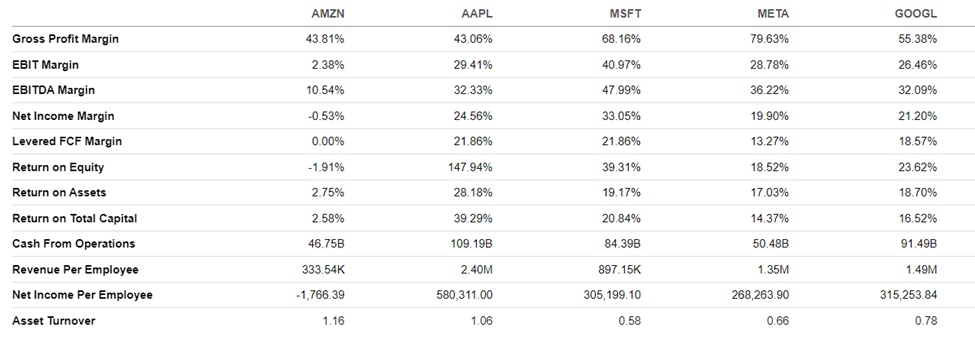

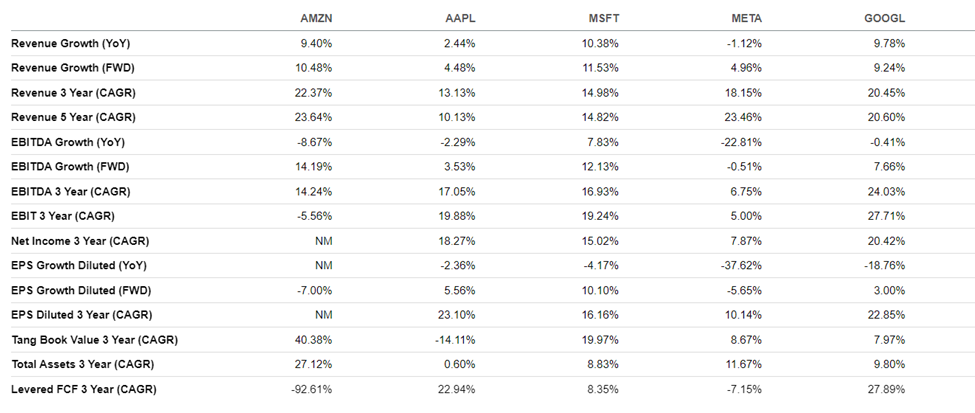

Sometimes what we don’t see is just as important as what we do. For example, 95% of the time, our proprietary Trackstar data shows a jump in a stock’s search volume around that stock’s earnings. This is true for searches by both retail investors and financial pros. Except this kind of surge didn’t happen for Amazon.com (AMZN). Total searches were largely the same before and after it reported earnings for Q4 2022 earlier this month. That could be because it’s already the third-most searched stock overall behind Tesla (TSLA) and Apple (AAPL). How much more popular can it get? Amazon posted record revenues of $513.9 billion in 2022. The only problem is the company didn’t make any profit. Shares are now down 40.8% from their 52-week highs. Is Amazon a steal at its current price? Or should you stay away? Amazon’s Business Unless you’ve been living under a rock, you know Amazon. It operates the largest e-commerce platform in the United States. As of June 2022, it made 37.8% of all online sales in the U.S. But its most profitable business is Amazon Web Services (AWS), which provides businesses with cloud-based computing services, including storage, computing power, and database management. The company breaks its business into three segments. The North America segment includes Amazon’s online retail platform, physical stores, Whole Foods Market, other retail-related services such as subscription services like Amazon Prime, advertising services, and customer credit and financing programs. The company’s international segment includes e-commerce sales and other retail-related services outside of North America. The third segment, AWS, includes computing, storage, databases, analytics, machine learning, security, and various other tools and services that help organizations build, deploy, and manage their cloud applications and infrastructures. Source: Amazon The North America segment lost $2.8 billion in operating income in 2022. International lost $7.7 billion. The company’s bright spot was AWS, which made $22.8 billion in operating income. People forget, but Amazon was largely unprofitable or barely so for most of its life. It wasn’t until AWS became a profit powerhouse that things changed for the company. Financials Source: Stock Analysis Amazon’s revenues have been consistently rising, going from $232.9 billion in 2018 to about $514.0 billion in 2022. 2020 was one of the company’s best years, as online ordering skyrocketed during COVID-induced lockdowns. But operating income significantly dropped in 2022, from $24.8 billion in 2021 to $12.2 billion. Amazon’s profitability fell from $33.3 billion in 2021 to -$2.7 billion in 2022, and its operating margin declined from 5.3% to 2.4%. The company burned through $26.0 billion in cash in 2022, and its cash position dropped 27.1%. It now has $70.0 billion in cash and $169.9 billion in debt. Valuation Source: Seeking Alpha Amazon fell out of profitability in 2022, largely due to growth plans that outpaced underlying demand. Its current P/E GAAP ratio is NM (not meaningful), significantly worse than other mega-cap tech companies like Apple (AAPL) at 20.1x, Meta Platforms (META) at 20.9x, Microsoft (MSFT) at 30.3x, and Alphabet (GOOGL) at 20.8x. Amazon’s EV/EBITDA ratio of 20.7x is notably lower than its five-year average of 31.6x but still higher than AAPL at 18.9x, META at 10.7x, MSFT at 20.5x, and GOOGL at 20.8x. Profitability Source: Seeking Alpha Amazon’s net income margin of -0.5% is brutal compared to its peers AAPL at 24.6%, MSFT at 33.1%, META at 19.9%, and GOOGL at 21.2%. Its operating margin of 2.4% looks tiny compared to mega-caps AAPL at 29.4%, MSFT at 40.9%, META at 28.8%, and GOOGL at 26.5%. Its cash from operations of $46.8 billion is less than META’s $50.5 billion, and META has less than half the market cap of AMZN. Meanwhile, AAPL has $109.1 billion in cash from operations, MSFT has $84.4 billion, and GOOGL has $91.5 billion. Amazon is trying to reduce spending to help it get back to profitability. The company announced last month that it would cut more than 18,000 jobs. Growth Source: Seeking Alpha Amazon did grow its revenues by 9.4% YoY, notably more than META at -1.1% and AAPL at 2.4%. MSFT and GOOGL did slightly better at 10.4% and 9.8%, respectively. But Amazon’s EBITDA growth fell 8.7% YoY. AAPL’s was -2.3%, MSFT’s 7.8%, and GOOGL’s -0.41%. The worst of the group was META at -22.8%. Our Opinion 5/10 AMZN shares are trading 40.8% below their 52-week highs. But the company recently reported a dreadful quarter to investors. Its revenues are increasing, but its profits are shrinking. Amazon’s CFO said the company has seen continued slowness this quarter for AWS, its moneymaker. That’s clearly not something investors want to hear. We’d wait for Amazon’s management to string together a few good quarters before considering an investment or for an entry near $80 to $85 (it currently trades above $101). There’s no reason to jump into AMZN at the moment. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |