|

Proprietary Data Insights Top Big Bank Stock Searches This Month

|

|||||||||||||||||||||

|

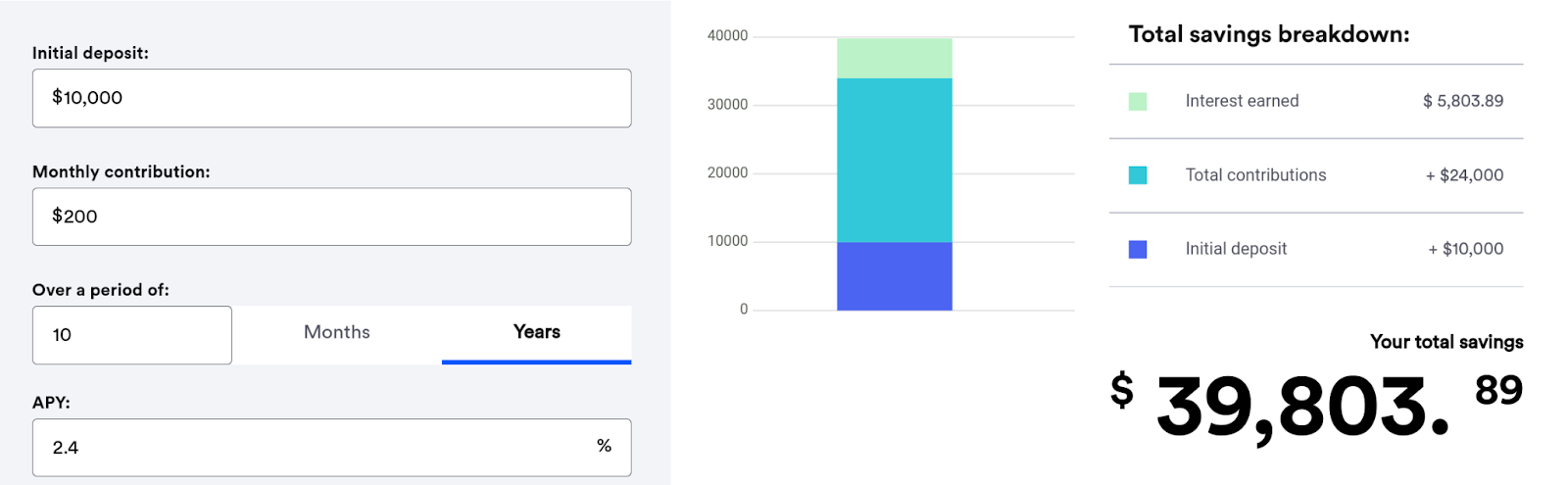

The Juice has a love-hate relationship with big banks. We love them because we think you can profit from some of their stocks, especially if the housing market takes shape the way we think it will this year. We hate them because of the paltry interest rates they still pay on their savings accounts. Using Wells Fargo (WFC) as an example, unless you have $100,000 or more in a savings account, you’ll earn either 0.15% or 0.25% interest at the bank. To secure the 0.25% rate, you need a minimum daily balance of $3,500 or you’ll pay a $12 monthly fee. If you have six figures or more with Wells, the bank will throw you the not-so-attractive bone of between 1.0% and 2.5%, depending on your balance. (For the record, these numbers came up when we said we live in California.) It’s even worse at Bank of America (BAC) and JPMorgan Chase (JPM), where rates still languish in the 0.01% to 0.04% range. Even as the Fed hikes interest rates, the big brick-and-mortar banks refuse to compete with the 3% or 4% interest rates online-focused banks now offer on savings. These big banks keep rates so low because they make their money on net interest income (NII), which is basically the difference between the interest they collect and pay out. Oddly, this move – combined with what we think will be greater mortgage and refinance activity in 2023 and 2024 – makes us long-term bullish on big banks, even if (or when) NII takes a hit. So it’s sort of pointless to explain compounding using a basic savings account. Even one with a decent interest rate. In a basic savings account, compound interest looks something like this: Source: Bankrate Just $5,803.89 interest on $34,000 over 10 years. What a letdown. What a waste of time. It’s much more exciting to explain how compounding works and can make you rich with dividend growth investing as the illustration. |

|||||||||||||||||||||

|

Dividend Growth Investing |

|

Turn $10,000 Into $199,739 in 30 Years |

|

Key Takeaways:

The most straightforward way to define compounding is earning interest on both your principal balance and the interest (or other form of income) it generates. If you deposit $5,000 into a savings account tomorrow, you earn interest on that $5,000. Let’s say, at the end of the month, you earned $1.00 in interest. Your balance becomes $5,001. Now you earn interest on that amount. As this process plays out every month in a basic savings account, the interest payment grows. And your balance grows exponentially with it. There’s a similar, but potentially way more lucrative, dynamic at play when we look at compounding in dividend growth investing. To explain what we mean, let’s see how your investment in a stock can grow over time – we’ll use 10 years to start – in different scenarios. 100 shares of a $100 stock that doesn’t pay a dividend and increases in price an average of 5% annually goes from $10,000 to $16,288.95 over 10 years. Let’s up the ante by adding a dividend. If you buy 100 shares of a $100 stock that pays a $1.00 annual dividend, and both the stock and dividend payment increase an average of 5% annually, you earn $1,318.08 in dividend income over 10 years. As you get it, you reinvest it into new shares of stock, which raises your rate of return annually to 6.0% and your principal balance to $17,908.48. Now, let’s throw additional $150 monthly contributions of your own money into the stock, keeping all the other metrics and factors – most importantly, reinvestment of dividend payments – the same. Your average rate of return falls, but your nest egg grows to $41,633.91. If you took away the dividend, it would grow to only $38,929.15 after 10 years. The key: time. Up your timeframe to 30 years. Your initial 100 shares of a $100 stock, growing at an average of 5% annually that initially pays a $1.00 annual dividend, also increasing at an average of 5% annually, alongside dividend reinvestment and a $150 monthly contribution would grow to $199,739.65. Major caveat: This was a neat and clean calculation, assuming linear stock growth (it just goes up 5% every year) and a dividend that rises 5% – and only 5% – annually. This calculation doesn’t account for when your stock decreases in price, and your dividend reinvestment and monthly contributions buy more shares. This is known as dollar-cost averaging. Buying more shares when their price is low and fewer shares when their price is high. It also doesn’t account for the stock and dividend growing more than 5% on average yearly.

The Bottom Line: It’s pretty easy to imagine a larger portfolio that acts this way – or better – over time. It’s the clearest path to wealth through investing. While there are no guarantees, it’s the most certain path in a world of uncertainty. Compounding is simple math. And we have an idea of what stocks do over time and how dividends increase – at strong companies paying stable dividends – over time. The key is to spread your exposure across strong dividend stocks and dividend ETFs rather than put your eggs all in one basket. |

|

News & Insights |

Freshly Squeezed |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |