|

Proprietary Data Insights Financial Pros Air Freight and Logistics Stock Searches in the Last Month

|

|||||||||||||||||||||

|

Air Freight and Logistics |

|

Can FedEx Deliver? |

|

|

After a euphoric start to the year, investors are again worried about inflation and the possibility the Fed will raise interest rates for an extended period. Perhaps surprisingly, FedEx (FDX) can be a barometer of economic activity because of the broad range of goods it moves. Watching the company often gives us clues we don’t see in economic data. That’s why we used our proprietary Trackstar search database to gauge financial pros’ interest in the stock. While United Parcel Service (UPS) got more searches in the last month, a recent spike in FDX search volume caught our attention. FedEx’s Business FedEx is a global delivery company that provides courier, ground, air, and freight services. The company generates revenue primarily by charging customers for delivery services. These services include:

Rising inflation forced consumers to cut back on spending in 2022, directly impacting FedEx’s business. The company announced it would no longer provide a monthly economic update in October 2022. A month later, it announced:

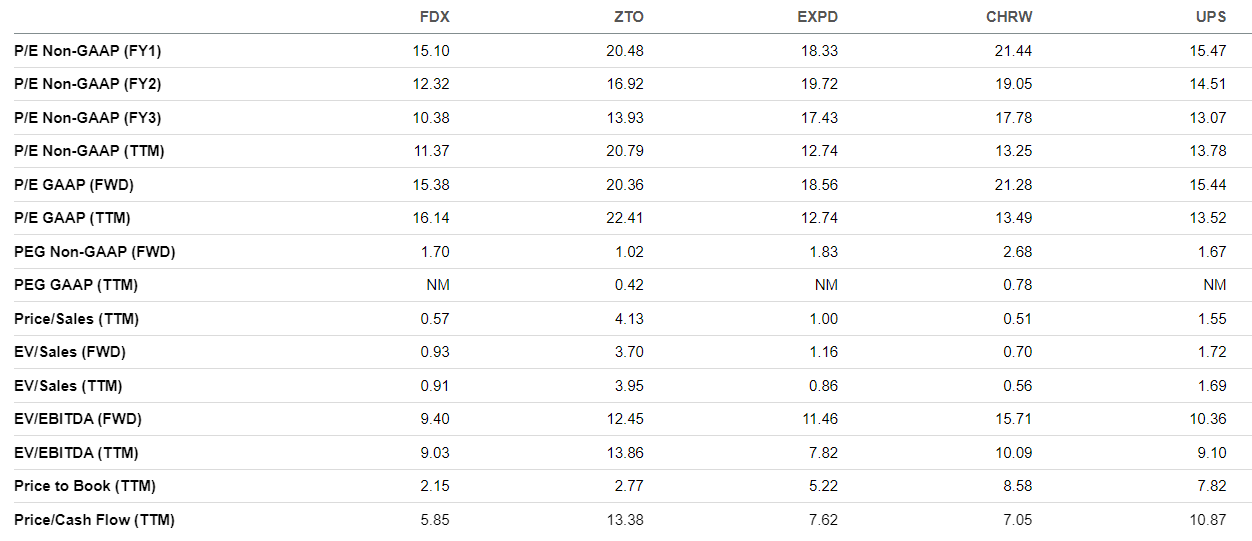

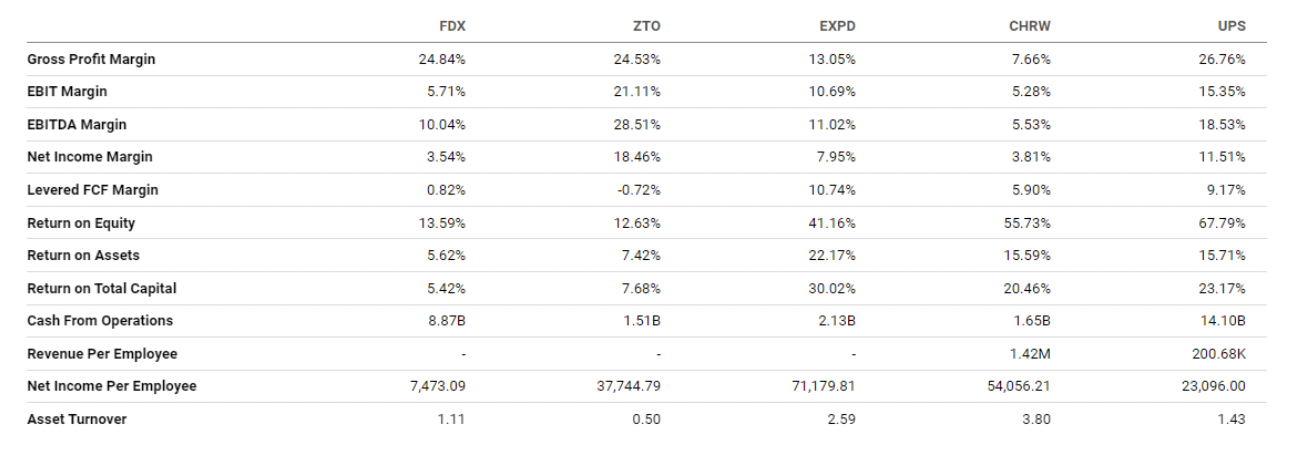

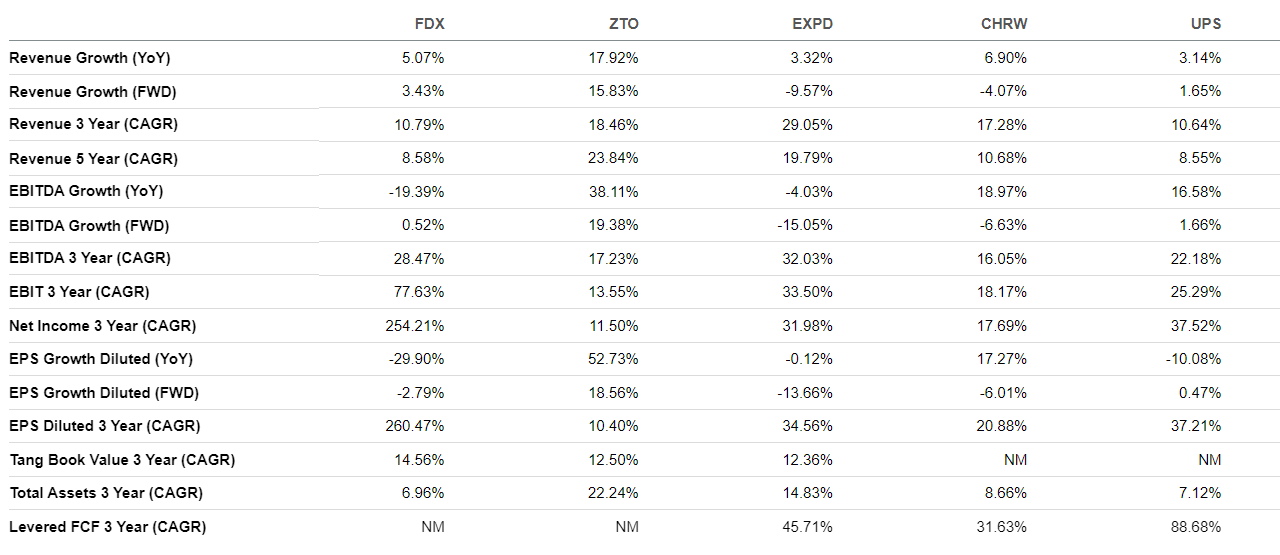

The drop in demand pushed the company to use a cost-saving plan. Management identified an incremental $1 billion in cost savings beyond its September forecast. It expects to generate total fiscal-year 2023 savings of approximately $3.7 billion relative to its initial FY 2023 business plan. Earlier this year, it announced it would further reduce its Sunday deliveries and cut more than 10% of management jobs. Most recently, shares of FDX have come under pressure as pilots threaten to strike over contract negotiations. Financials Source: Stock Analysis FDX’s revenues have bounced nicely since 2020, from $69.2 billion to $93.5 billion in 2022. But the company’s net income has fallen sharply from $5.2 billion in 2021 to $3.8 billion in 2022, a much sharper drop than its peer UPS. In addition, its trailing-12-month (TTM) net income is $3.3 billion. Its diluted earnings per share have fallen from $19.45 in 2021 to $12.76 TTM. But the company has boosted its dividend to $3.80 per share annually from $2.60 in 2021. FDX has $38.0 billion in debt and $4.6 billion in cash. Its current ratio of 1.3x shows it’s financially stable and can handle its short-term obligations. Valuation Source: Seeking Alpha FDX trades at a 16.1x P/E GAAP ratio, which is relatively high compared to peers UPS at 13.5x, C.H. Robinson Worldwide (CHRW) at 13.5x, and Expeditors International of Washington (EXPD) at 12.7x. It is, however, cheaper than ZTO Express (ZTO) at 22.4x. FDX looks cheaper than its peers on a price-to-cash-flow basis at 5.9x, compared to UPS at 10.9x, CHRW at 7.1x, EXPD at 7.6x, and ZTO at 13.3x. Its EV-to-EBITDA ratio is also on the lower end at 9.0x, compared to UPS at 9.1x, CHRW at 10.1x, and ZTO at 13.8x. But it’s not as low as EXPD at 7.8x. Profitability Source: Seeking Alpha FedEx is committed to improving profitability. As we said, it plans to cut spending and save $3.7 billion in 2023. Its net income margin of 3.5% is relatively low compared to UPS at 11.5%, CHRW at 3.8%, EXPD at 7.9%, and ZTO at 18.5%. FDX’s EBIT margin of 5.7% also looks weak compared to ZTO at 21.1%, EXPD at 10.7%, CHRW at 5.3%, and UPS at 15.4%. FedEx’s gross profit margin of 24.8% is higher than most of its peers but slightly behind UPS at 26.8%. Growth Source: Seeking Alpha FDX has done an exceptional job of growing revenues over the years. In 2017, it made $60.3 billion in revenues, while in 2022, it made a record $93.5 billion. Its year-over-year revenue growth of 5.1% is relatively low compared to previous years, ZTO at 17.9%, and CHRW by 6.9%. But it’s better than UPS at 3.1% and EXPD at 3.3%. Over the last three years, FDX has been solid, with an EBIT compound annual growth rate of 77.6% compared to ZTO at 13.6%, EXPD at 33.5%, CHRW at 18.2%, and UPS at 25.3%.

Our Opinion 7/10 FDX offers investors an opportunity for growth and income, with a dividend yield of 2.3%. It’s in an industry where the barrier to entry is high, which is good if you’re a long-term investor. The stock seems to have gotten a little ahead of itself. At writing, FDX is already up 15.3% year to date, trading at $204.34. We’d buy if it can pull back to $185 to $190. Stay tuned to The Spill for our analysis of UPS in an upcoming newsletter. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? |