|

Proprietary Data Insights Financial Pros Top Industrial Stock Searches in the Last Month

|

|||||||||||||||||||||||||||

|

Industrials |

Buy My Package |

|

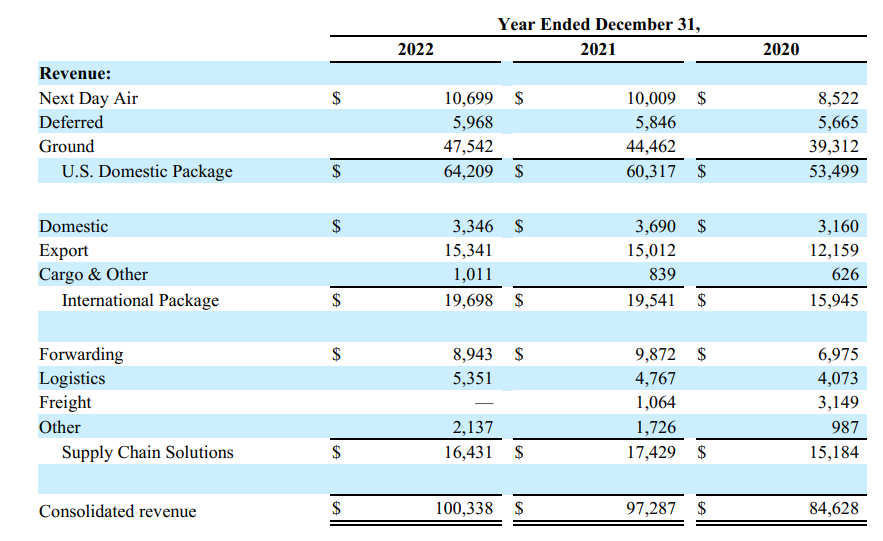

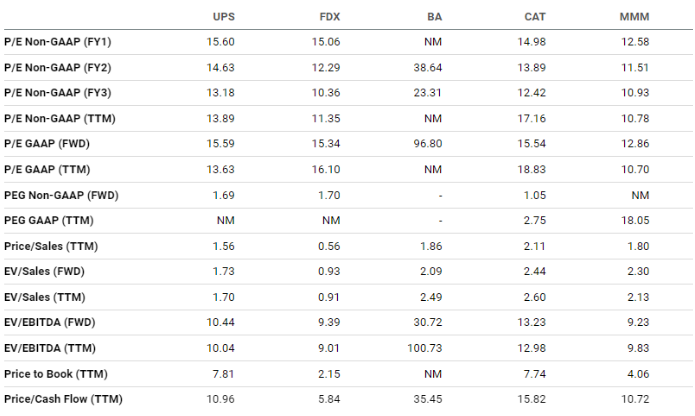

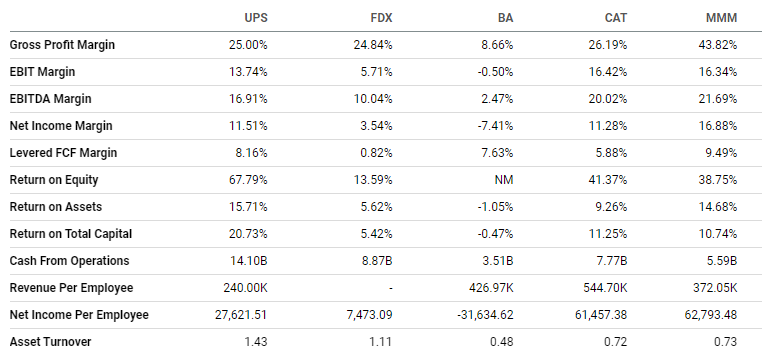

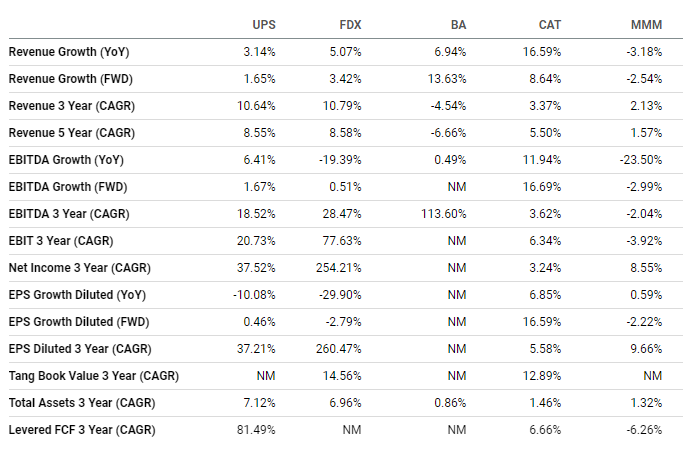

Last week, we left you with a bit of a teaser. We’d spoken highly of Memphis-based international freight logistics company FedEx (FDX) in Thursday’s issue of The Spill. At the same time, we noted the intriguing value of United Parcel Service (UPS). We admit, we were surprised to see UPS garner more searches from financial pros than FDX did. UPS seemed to be a stodgier player in the same market. Yet our proprietary Trackstar database showed UPS’ searches constantly outstripped FDX’s. UPS landed at #7 in financial pros’ industrial sector stock searches. A couple years ago, UPS was in the top five pretty consistently. A lot has changed since then. But as you’ll soon see, UPS has a stable business model with growth potential and true investor value. United Postal Service’s Business UPS was founded in 1907. It’s the world’s largest express carrier and package delivery company. With a ground fleet of over 120,000 vehicles and 624 aircraft, the company moves more than 25 million pieces per day and nearly 7 billion each year. UPS operates globally, providing package shipping as well as specialized transportation and logistics services. U.S. business accounted for 64% of all revenues in 2022, followed by international packages at 19.6% and supply chain solutions at 16.4%. Source: UPS 10-K The company’s Q4 revenue fell 2.7% from the prior year. Operating profit was down 3.3%. Notably, Q4 total average daily volume was down across the board, largely due to demand tempering from extreme levels. Many analysts expect weaker demand in 2023, which pricing and margin improvement will largely offset. Financials Source: Stock Analysis UPS’ revenues exploded in 2020 and 2021 as online demand skyrocketed, largely due to COVID. Profit margins also greatly improved, hitting a high of 13.3%. This rapid growth should shrink over the next year or so as consumer spending normalizes. Also noteworthy is UPS’ massive dividend increase of 49.0% last year, putting the current yield at 3.6%. While $17 billion in long-term debt might seem excessive, that’s down from $22 billion just a few years ago. But there’s an overhang of pensions, and union negotiations hit in earnest this summer. Nonetheless, a quick ratio of 1.2x and a current ratio of 1.1x mean investors shouldn’t worry about liquidity or dividend cuts. Valuation Source: Seeking Alpha For comparison, we left FDX in our spreadsheet and added three other industrials to give us a sense of where UPS lies in the broader sector. To that end, UPS has the lowest price-to-earnings ratio over the last 12 months and looking forward, at 13.6x and 15.6x respectively, apart from 3M (MMM) at 10.7x and 12.9x. But the price-to-earnings growth (PEG) non-GAAP ratio is nonexistent for MMM looking forward, while UPS is right up there with FDX at 1.7x, implying better profit potential for UPS than MMM. FDX is the clear winner for price-to-cash flow at 5.9x. But UPS at 11.0x isn’t too shabby, just behind MMM at 10.7x. Boeing (BA) at 35.5x isn’t in the same ballpark, and Caterpillar (CAT) at 15.8x is just more expensive. Profitability Source: Seeking Alpha MMM is the clear winner for gross margin at 43.8%. CAT comes in second, well behind at 26.2%. It’s just ahead of UPS at 25.0% and FDX at 24.9%. Boeing is again well outside the norm at 8.7%. UPS’ 13.8% EBIT margin is impressive despite coming in behind CAT at 16.4% and MMM at 16.3%. Notably, FDX managed only 5.7% last year, and BA was unprofitable. UPS is in the top spot for return on equity, assets, and capital, at 67.8%, 15.7%, and 20.8% respectively, handily outpacing its peers in every category, aside from MMM, which had a decent return on assets of 14.7%. Growth Source: Seeking Alpha We won’t bother with BA other than to say it has a decent revenue growth outlook. But that’s bound to happen when the bar is so low. Among the other players, MMM interestingly had negative growth last year. CAT grew a nice 16.6%, which has largely been priced into the stock. The forward outlook for MMM is negative, which again is a bit of a surprise. UPS is expected to hit only 1.7%, with FDX slightly better at 3.4%. CAT has a solid outlook at 8.6%. But for compound annual growth rate over the last five years, UPS and FDX are within a hair of each other at 8.6% rounded. Only CAT comes close at 5.5%, leaving MMM in the dust at 1.6%. Interestingly, CAT had the standout EBITDA growth last year at 12.0% and a solid outlook of 16.7% this year. UPS did 6.4% last year and is looking at only 1.7% this year. FDX had negative EBITDA growth last year and is forecast for 0.5% this year. UPS doesn’t look like it’ll go gangbusters. But it should steadily improve. Our Opinion 9/10 UPS offers a pretty compelling valuation and story. The company generates oodles of cash and is priced fairly well. We aren’t thrilled about its growth outlook. But it’s predicated on a recessionary forecast and comes off a banner year. This is a great stock with a healthy dividend. Based on the technicals of the chart and the likely stagnant environment ahead, this is one to dip your toe into over time, reinvest the dividend, and wait for a break of $150 (it’s trading above $180 at writing) before taking a larger position. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? |