|

Proprietary Data Insights Financial Pros Top Industrial Stock Searches in the Last Month

|

|||||||||||||||||||||

|

Healthcare |

|

Pfizer’s COVID Hangover |

|

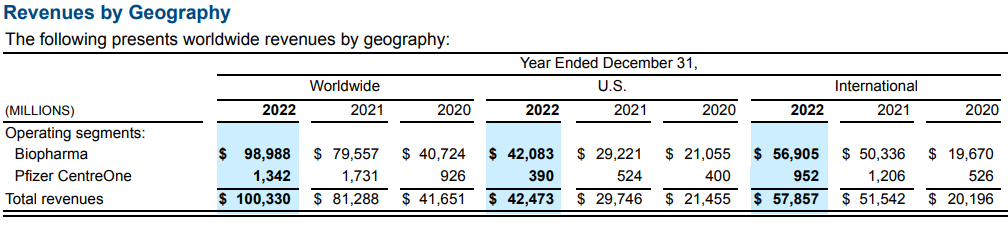

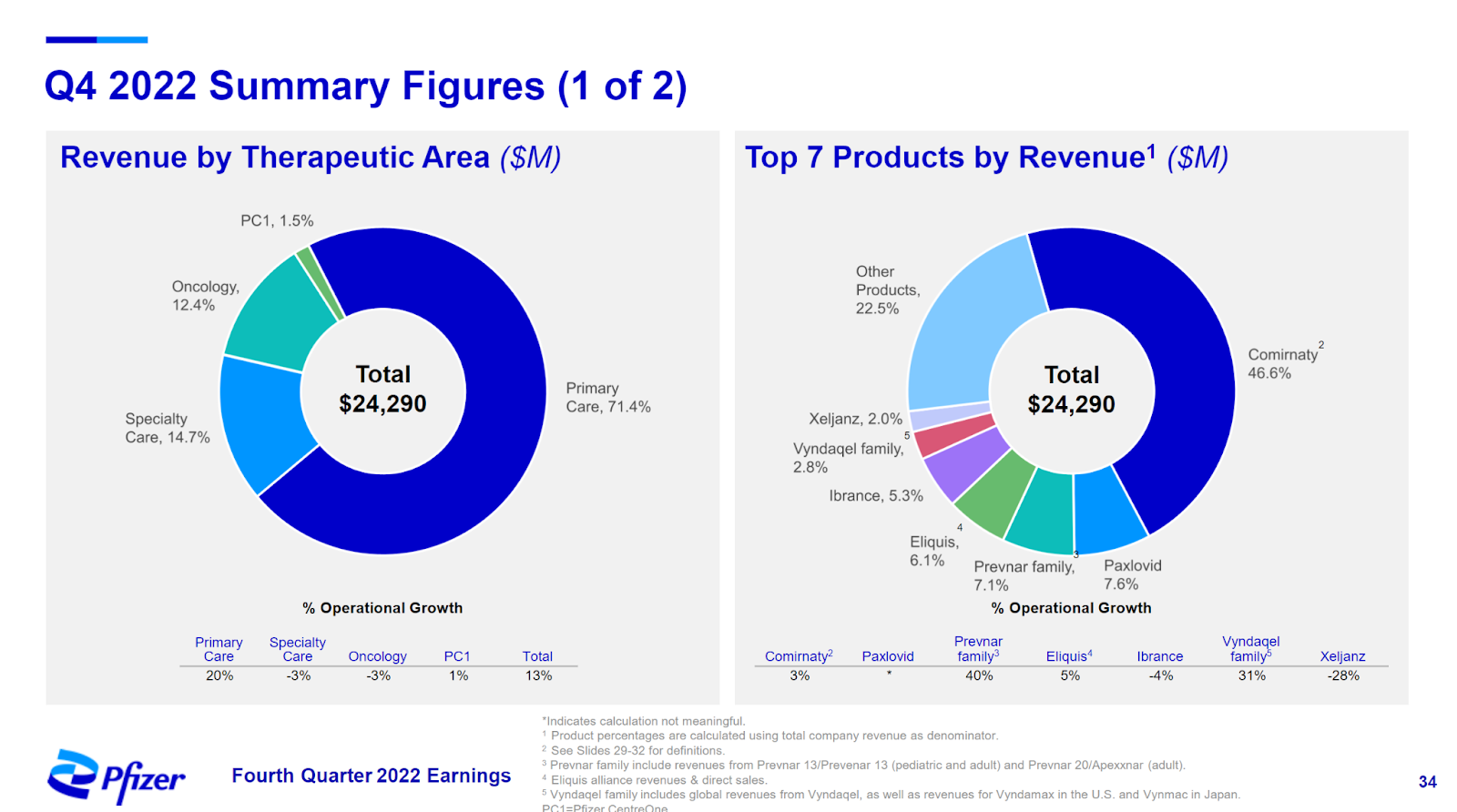

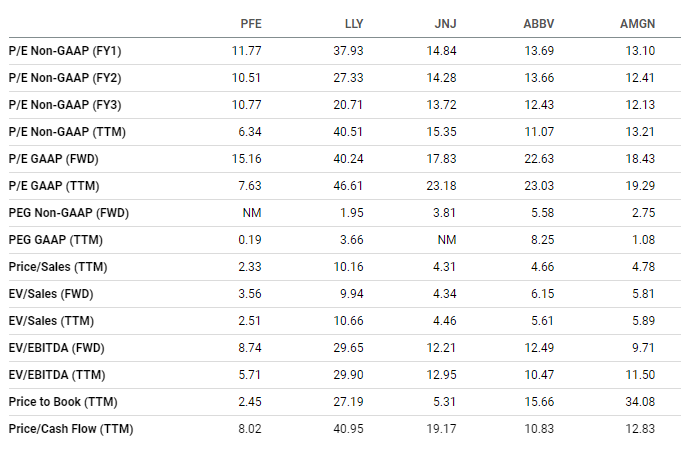

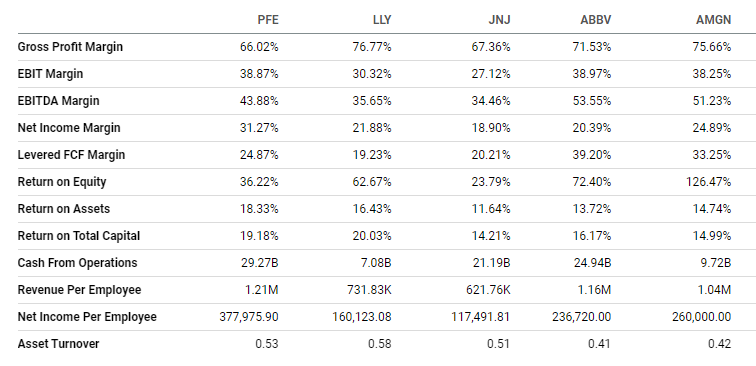

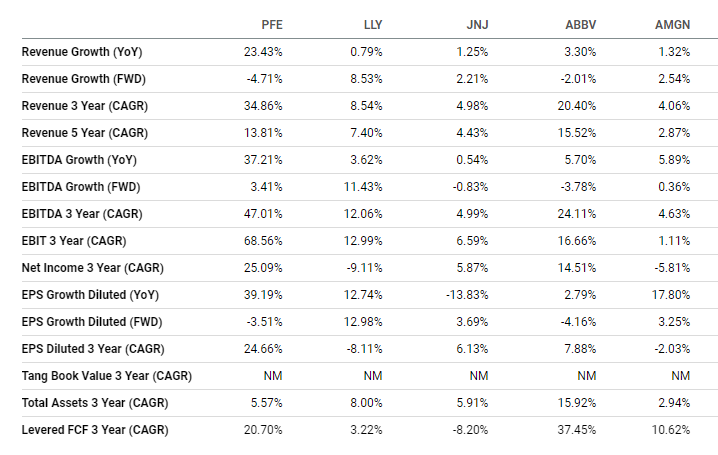

You may view Pfizer (PFE) as the savior or satan born out of the pandemic. Pfizer’s partnership with BioNTech helped it deliver a vaccine in record time using mRNA technology, making it one of only two companies to do so, the other being Moderna (MRNA). At the time, Johnson & Johnson (JNJ) was the only other company to create a successful, though less effective, vaccine, one that enabled easier distribution and required only one injection. Pfizer banked on the pandemic. It sold $37.8 billion of its vaccine in 2022, a 3% increase over the prior year. And we can’t overlook Pfizer’s COVID antiviral pill, Paxlovid, which hit $18.9 billion in sales last year. But the world has been returning to normal. And Pfizer expects revenues to fall as much as 33% to $67 billion this year $71 billion last year as COVID remains in the background. It projects its COVID vaccine sales to plummet as much as 64% from $37.8 billion to $13.5 billion this year. That translates to a nearly 50% drop in earnings from a record $6.58 earnings per share in 2022 to $3.25-$3.45 this year. Financial pros searched for Pfizer stock more often than any other industrial name. So we’re digging into the pharma giant’s outlook today. Pfizer’s Business Pfizer has been around since 1849. It’s one of the world’s largest pharmaceutical companies and has its headquarters in New York City. It develops and manufactures medicines, vaccines, and consumer healthcare products. It also provides services to healthcare providers, governments, and other organizations. As a healthcare behemoth, the company’s products touch many health areas, including cancer, cardiovascular disease, psychiatry, and veterinary care. Pfizer first rose to prominence with Terramycin, an antibiotic it developed in 1950 and commercialized in 1953. It also makes the blockbuster antidepressant Zoloft. Pfizer products are sold in over 150 countries through a salesforce of over 15,000 individuals. The company lists its revenues as either Biopharma or Pfizer CentreOne (global contract development and manufacturing) and then by geography: Source: Pfizer SEC filing By therapeutic area, primary care accounts for nearly 75% of total revenues, with nearly half the revenues coming from Comirnaty, Pfizer’s COVID vaccine. Source: Pfizer Q4 2022 presentation Financials Source: Stock Analysis Pfizer’s remarkable growth is largely due to the company’s COVID vaccine and antiviral. But excluding those items, management still expects 7% to 9% revenue growth. We noted earlier the expected decrease in revenues due to declines in COVID-related sales. But management isn’t resting on its laurels. The company recently announced deals that push it into migraine and sickle cell disease treatments. Plus, its current pipeline has an RSV vaccine for adults 60+ set to launch in the first half of this year and a maternal vaccine to prevent RSV-associated lower respiratory tract infections set for the second half. Pfizer currently has a massive $22.7 billion in cash against long-term debt of $33.2 billion, though $20.1 billion of that debt is non-current liability. Nonetheless, with PFE’s current ratio of 1.2x and quick ratio of 0.9x, plus operational cash flows the company expects to be over $20 billion, investors aren’t worried about solvency nor the company’s ability to pay its healthy 3.93% dividend. Valuation Source: Seeking Alpha Notably, Pfizer’s trailing performance isn’t indicative of its future. So it’s worth considering only future metrics for the company. To that end, it’s still got the best forward-looking price-to-earnings (P/E) ratio of its closest peers, at 15.2x compared to Amgen (AMGN) at 18.4x, JNJ at 17.8x, AbbVie (ABBV) at 22.6x, and Eli Lilly (LLY) at an unhealthy 40.5x. It’s worth mentioning Pfizer’s forward-looking price-to-cash-flow ratio of 15.4x, which isn’t too shabby. But JNJ’s forward ratio here is slightly better at 14.1x, ABBV better at 12.1x, and AMGN even better at 12.0x. Only LLY’s 39.4x is an expensive outlier. Profitability Source: Seeking Alpha The recent profitability of COVID vaccines affected PFE’s margins. PFE has the lowest gross profit margin of the group and comes in the middle in terms of EBIT and EBITDA margins, but dominates on net income margin. We aren’t thrilled with PFE’s second-worst return on equity of 36.2%, especially considering LLY’s is 62.7%, ABBV’s is 72.4%, and AMGN’s is a whopping 126.5%. But PFE comes out on top for return on assets at 18.3% and second-best for return on total capital at 19.2%. Plus, it has the most cash from operations at $29.3 billion, with ABBV second at $25.0 billion. Growth Source: Seeking Alpha Forward revenue growth is negative for PFE, as expected. But none of the other companies have much to boast about either. LLY grew most at 8.5%, then AMGN at 2.5% and JNJ at 2.2%. ABBV’s revenues are expected to decline by 2% this year, not as bad as PFE at 4.7%, but still not good. Our Opinion 8/10 A lot of folks are unnecessarily down on Pfizer given the global post-pandemic return to normal. But the company now has tech capable of delivering vaccines in record time. It also produces oodles of cash and pays a large dividend. PFE now trades just above $40. Its 2020 low was $26.43. We like it at these levels and love it below $40. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |