|

Proprietary Data Insights Financial Pros Top Social Media Stock Searches Last Month

|

|||||||||||||||||||||

|

Technology |

SNAPped in Pieces |

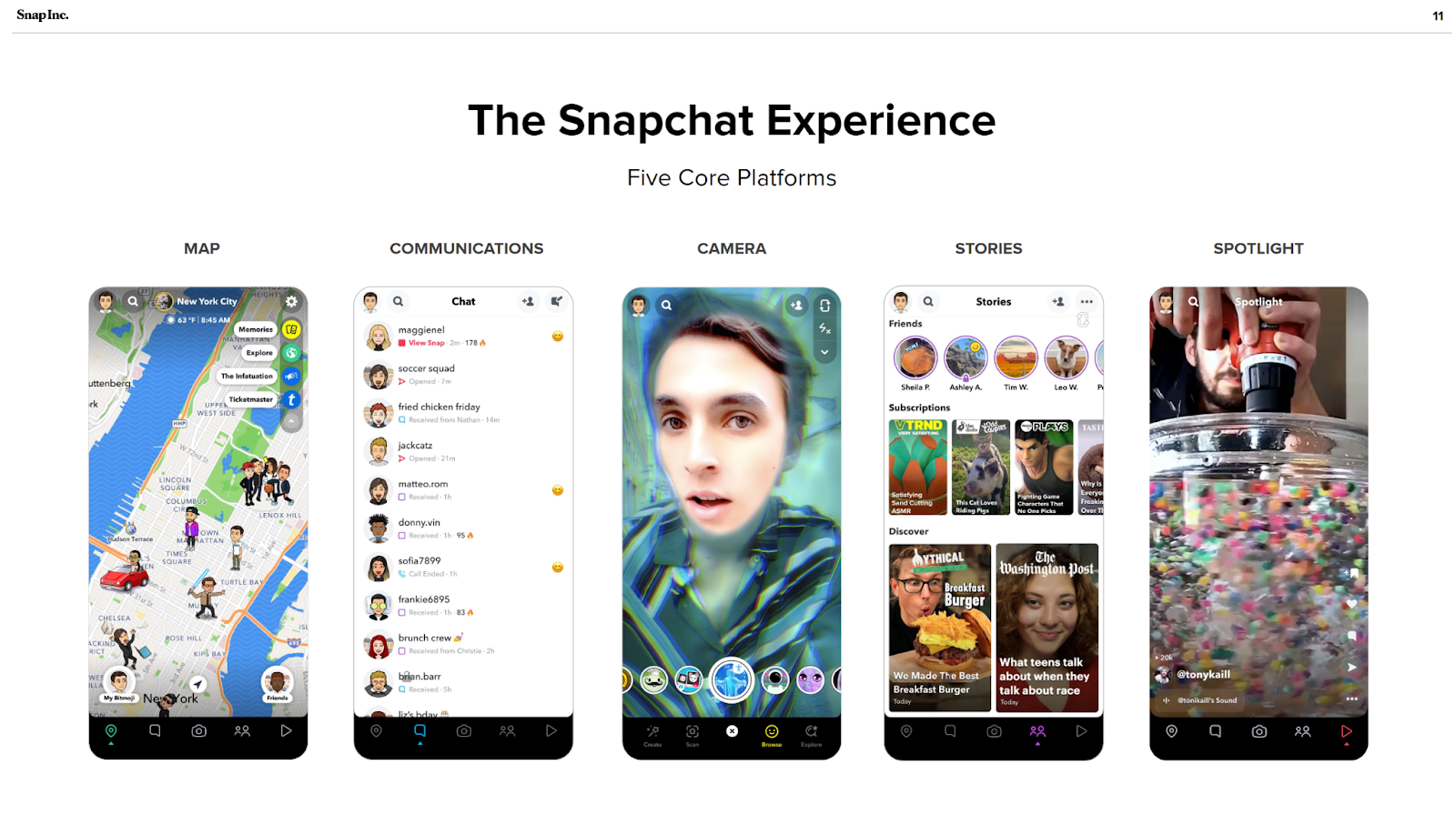

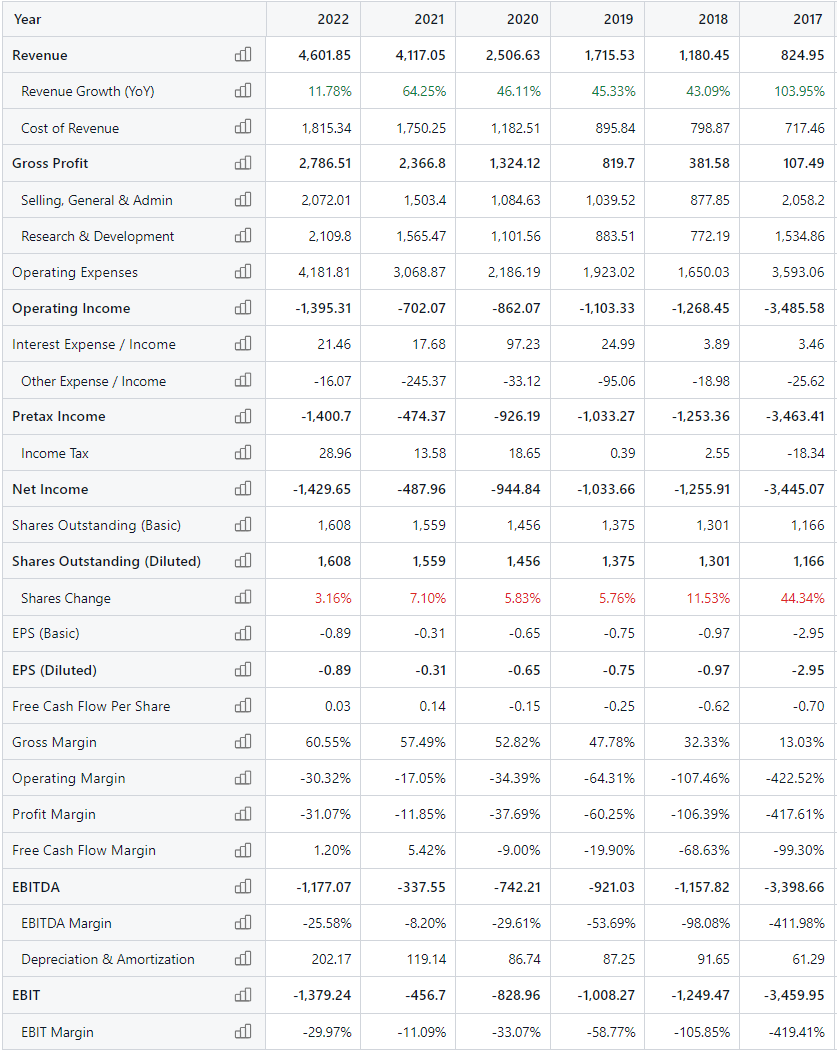

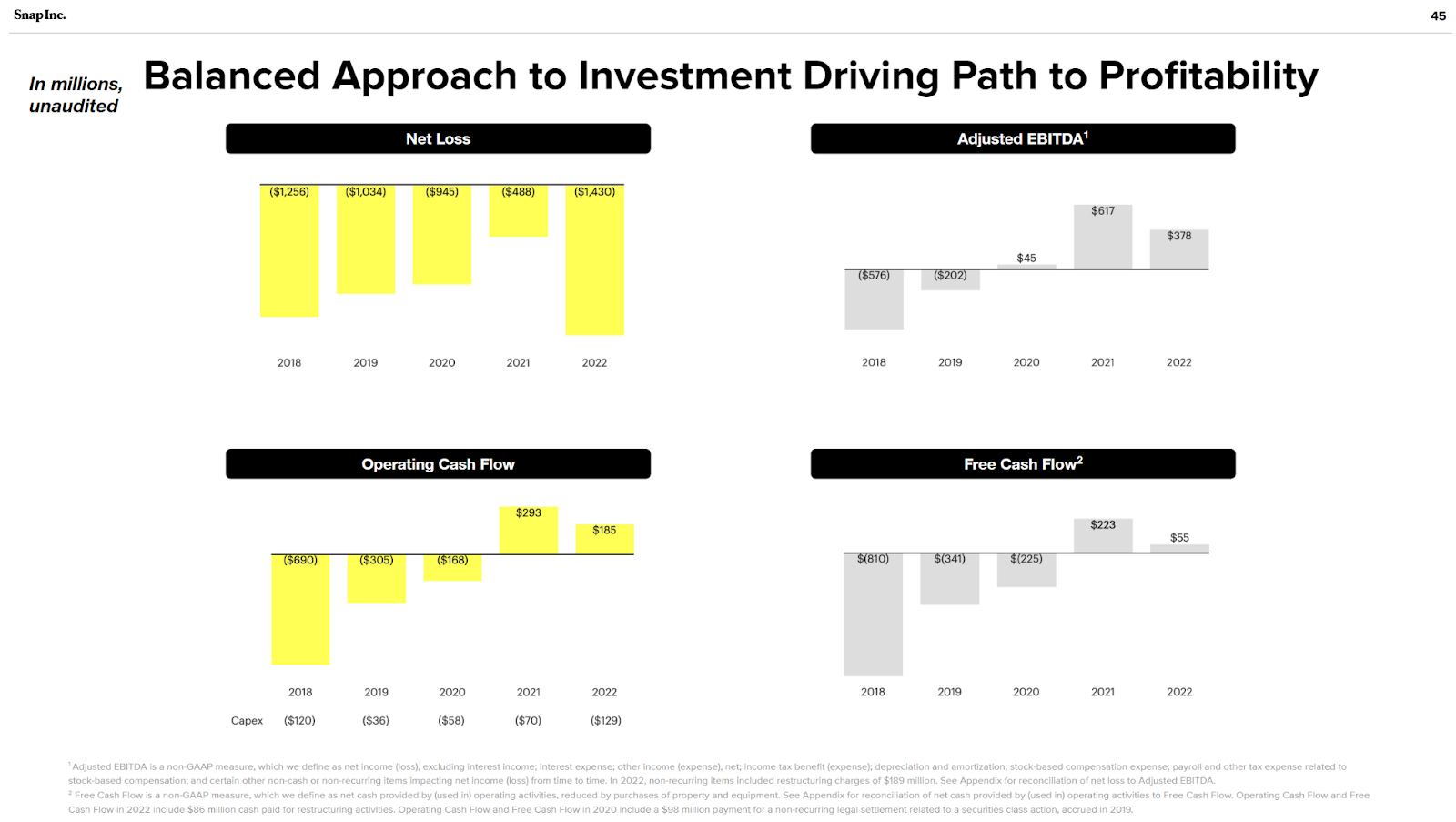

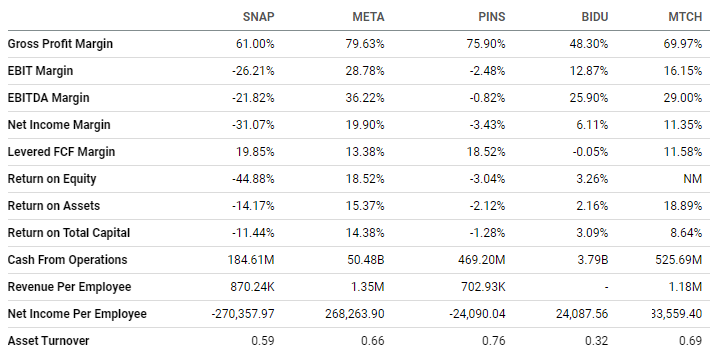

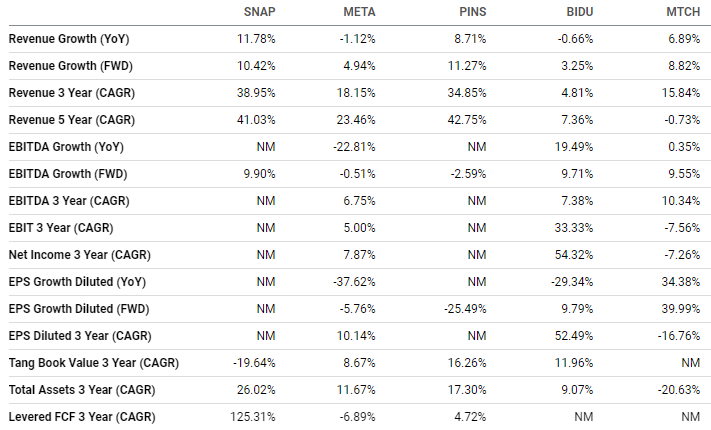

How do you know when a stock is garbage? When it rallies 20% on immaterial news. That’s what happened in the last week as Snap (SNAP), one of the worst stocks we’ve ever covered, rallied off a potential TikTok ban. At the end of May last year, we rated SNAP a 3/10, which was probably generous. The stock had come off horrid earnings and was trading around $15.00, well off the $83.34 high it made in late September 2021. Since then, the stock has fallen even more, trading around $12.00 today. Keep in mind that this is after its recent rally from trading below $10.00. That means the stock had dropped another 33% since we ran our story. Normally, we wouldn’t want to kick a bad stock when it’s down. But our proprietary Trackstar database shows there’s been a surge in interest from both financial pros and retail investors. We don’t blame them given the recent short squeeze. But that’s all it is. SNAP isn’t a penny stock. It isn’t a high-growth tech company either. It’s what we call dead money. Snap’s Business Social media was hotter than hot during the pandemic. But high demand and low supply across a broad range of industries meant advertisers didn’t need to get out their messages. Consequently, many social media companies saw advertising spend drop in the last year or so. Snap, the company behind social media app Snapchat, wasn’t immune to the trend. Known for its videos that are there and gone in a flash, the trendy firm that calls itself a camera technology company has struggled to grow at its once torrid pace. Snapchat’s business boils down to five main parts of its platform: Map, communications, camera, Stories, and Spotlight. Source: SNAP January investor presentation While its platform has some unique features and boasts some of the best augmented reality around, Snap has two main problems. First, it’s not unique. It started as short-form videos that disappeared after viewing. That’s just an automatic delete function. Second, Snapchat is in a unique position to cultivate a young audience that doesn’t have money to spend. And with politicians more concerned about children’s exposure to social media, Snap could see its core demographic wiped out. Financials Source: Stock Analysis Generally, companies that trade below $10 do so because they aren’t operating-cash-flow-positive or are barely so. Snapchat does generate positive operating cash flow, but barely. For a company that does $4.6 billion in annual revenues, the following slide (you can see a larger version at slide 45 here) isn’t that impressive. Source: SNAP January investor presentation The company hasn’t turned a GAAP profit. It only recently turned operating- and free-cash-flow-positive. But the amounts dropped from 2021 to 2022. The company now holds nearly $4 billion in cash against $3.7 billion in long-term debt. With a current ratio of 4.3x and a quick ratio of 4.2x, at least liquidity isn’t a problem. Valuation Source: Seeking Alpha SNAP doesn’t turn a profit, nor does Pinterest (PINS). Meta (META), Baidu (BIDU), and Match Group (MTCH) do, trading at 19.5x, 22.5x, and 18.9x forward earnings, respectively. Those are a bit rich for different reasons, but they’re not terrible. In price-to-cash-flow ratio, SNAP is grossly overvalued at 99.9x, while META trades the lowest at 9.5x. The only measure where SNAP doesn’t look terrible is its price-to-sales ratio of 4.1x, which is in the middle. META trades at 4.3x, PINS 6.3x, BIDU 2.9x, and MTCH 3.5x. Profitability Source: Seeking Alpha It’s somewhat disturbing for SNAP’s gross margin to be below its peers’ save BIDU’s. That tells you SNAP’s base operations aren’t where they should be. And the company’s other margin metrics are all negative. It’s worrisome that SNAP’s cash from operations is a third of PINS’, when PINS has the same market cap and 2x the revenue. Growth Source: Seeking Alpha As we noted earlier, SNAP’s growth has stalled. It grew only 11.8% in 2022 and is expected to grow revenues a paltry 10.4% this year. While none of the social media companies are expected to do well, SNAP is probably in the worst position. Our Opinion 2/10 We’re downgrading SNAP to a 2/10. It gets the two points because it generates cash from operations… barely. But it doesn’t have much in terms of growth prospects. That doesn’t mean it can’t squeeze shorts, shooting up 10% to 20% in a day or two. But long-term investors should steer clear. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |