|

Proprietary Data Insights Financial Pros’ Top Footwear Stock Searches in the Last 30 Days

|

|||||||||||||||||||||

|

Consumer Cyclical |

Foot Locker Earnings Exclusive |

For the first time… The Spill is covering a stock BEFORE its earnings report. Here’s why. You’ve been told malls are dead… and that you shouldn’t touch apparel companies. Respectfully, we disagree. As our proprietary Trackstar data highlights above, Nike (NKE) was financial pros’ top footwear stock search last month. But when we compared the top five companies, another stood out… Foot Locker’s Business Foot Locker (FL) is the sneakerheads’ athletic shoe and apparel store. The company operates websites, mobile apps, and its flagship retail stores. Although three-quarters of its sales come from the U.S., Foot Locker has a global presence. Beyond its main namesake brand, the company owns and operates Champs Sports. In the last year, Nike, one of Foot Locker’s strategic suppliers, reduced the number of sneakers it sold outside its website. That hasn’t really fazed Foot Locker. Despite a negative outlook, it’s turned toward online sales, customer service, and diversifying its offerings. Some highlights include:

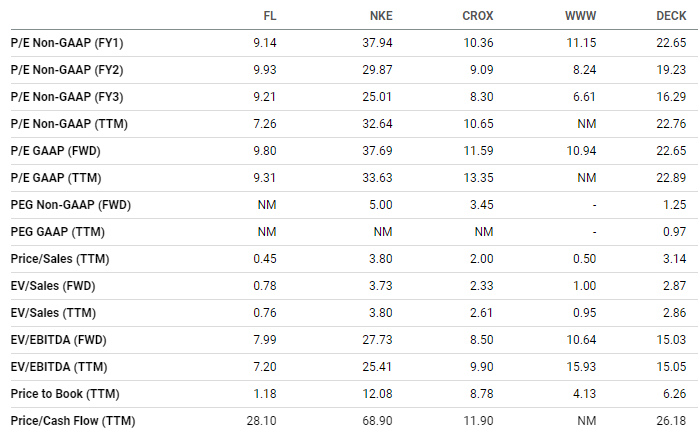

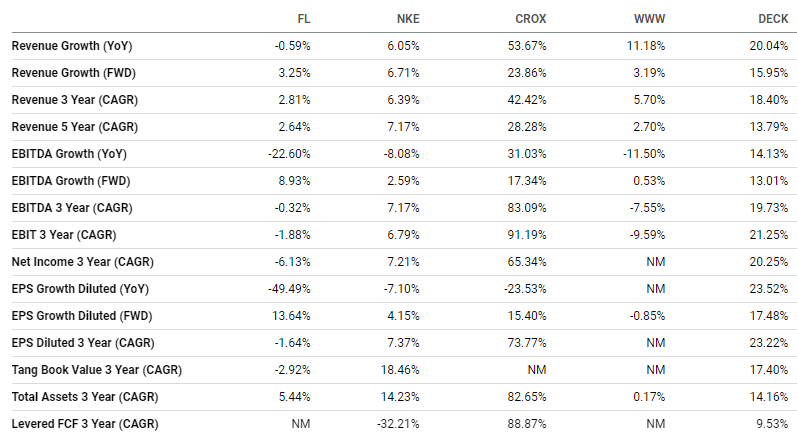

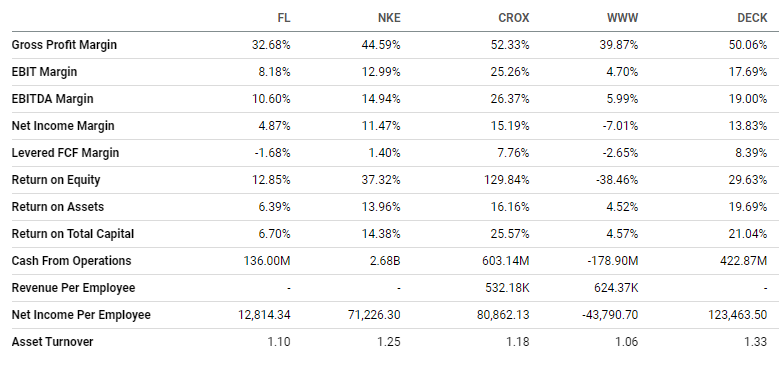

Additionally, FL is likely to deliver cost optimization worth $300 million in annual savings. Financials Source: Stock Analysis Foot Locker is a cash cow. It hasn’t had the greatest growth, but it’s still grown. And its margins are juicy. Plus, the company pays a whopping 4% dividend yield that’s been consistent for years. While cash flows declined during the spring and summer quarters last year due to inventory changes, they quickly rebounded last quarter. Annually, the company generates just shy of $1 billion in operational cash flow, with free cash flow just above $500 million. Add in the $200 million in cost savings, and it has a nice bundle of cash. Plus, it has only $448 million in long-term debt. Valuation Source: Seeking Alpha Foot Locker beats all the peers we compared it to across every value metric except price-to-cash-flow ratio. But if you normalize for inventory changes, Foot Locker comes out on top. Growth Source: Seeking Alpha FL doesn’t come close to the growth of its peers across revenue measures. But its forward-looking EBITDA and EPS growth put it in the middle of the pack. Profitability Source: Seeking Alpha Foot Locker doesn’t have the best profitability, especially on its gross margin, which is now 32.7% but used to be in the low 40s. We’d like to see the company improve its gross profit margin. We expect its cost savings initiatives to help with overall profitability. Our Opinion 8/10 Foot Locker currently trades above $40.50. It’s set to report earnings on March 20. Its last two earnings announcements sent the stock higher the following day. But we’d let the current volatility work in our favor and wait for a dip to the low $30s for an even better entry. |

|

News & Insights |

Just Spilled |

|

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |