|

Proprietary Data Insights Top Mortgage Financier Stock Searches This Month

|

|||||||||||||||

Mortgage Financiers |

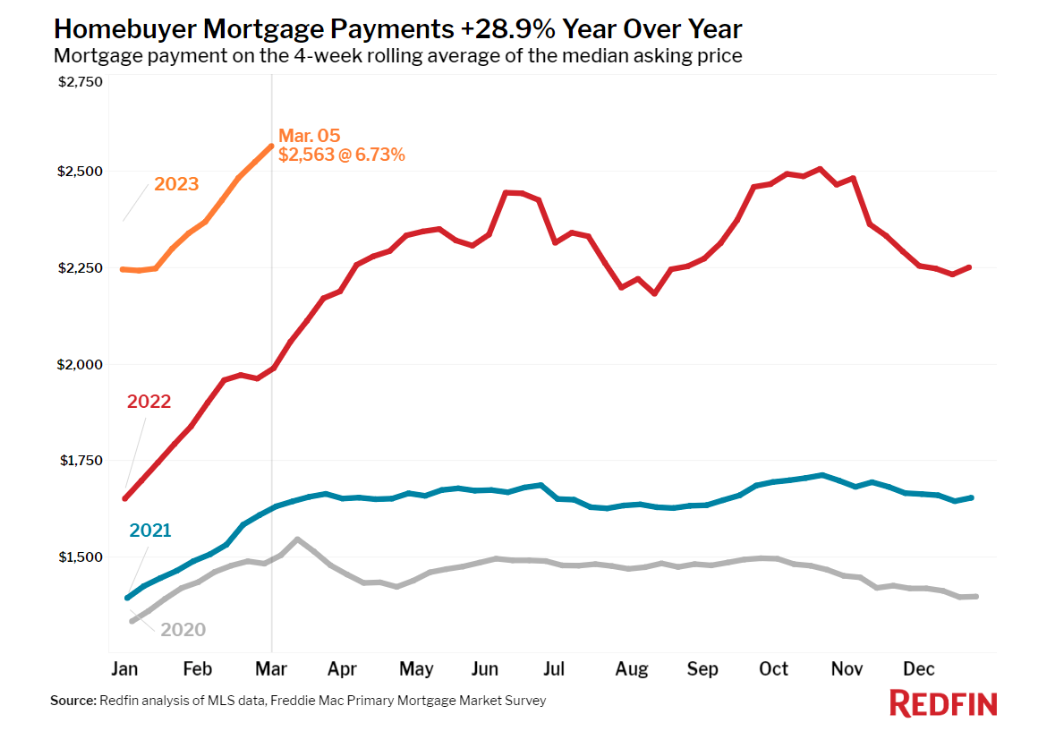

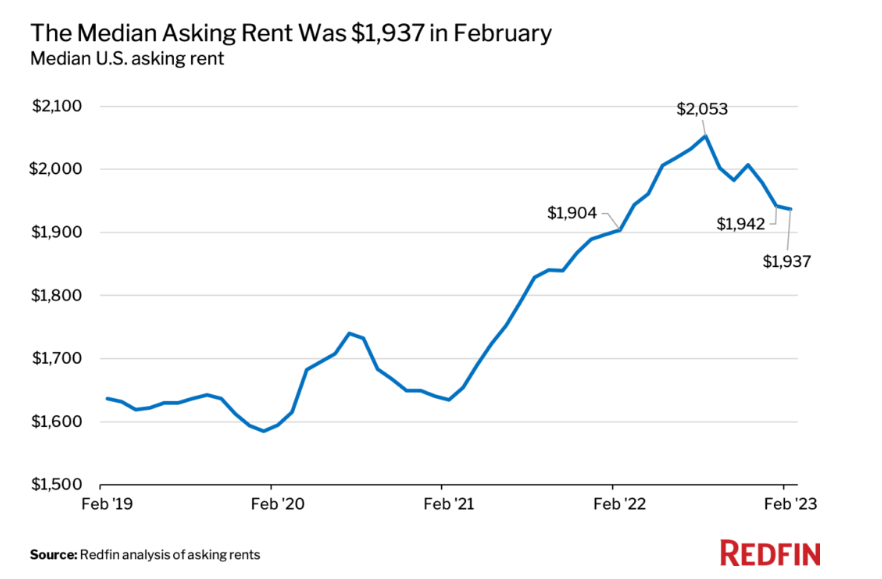

According to Redfin, the typical U.S. homeowner’s monthly payment hit a record high of $2,563 last week. That’s up 29% from a year ago, thanks largely to mortgage interest rates still hovering around 7% and housing prices that, despite the recent cooldown, remain high. If your housing budget is $2,500 a month, you can afford a $376,000 home, down from the $400,000 crib you could’ve snagged last year. This creates conundrums for home seekers as well as home sellers. Prospective home sellers, particularly those locked into low interest rates, might be hesitant to sell because they’d presumably need to secure new shelter. If they plan to buy again, they’ll likely face higher prices and definitely higher interest rates. If they want to rent, they’re up against a national median rent of roughly $2,000 a month. Like real estate prices, rent is down, but it’s still historically expensive, particularly in big cities:

Which brings us to renters thinking about becoming homeowners. If your rent is cheap, it might be hard to let that go in this environment. Giving up a sweet deal for considerably higher monthly costs doesn’t sound too attractive, especially if your financial situation has you only on the cusp of affordability. Realtors aren’t exactly helping matters. To entice would-be homebuyers to take the plunge, they’re using the pickup line, “Marry the house, date the rate.” Cute talk to say you can get the house you love today at a high rate and refinance later at a lower rate. But it’s not that simple. First, what if rates don’t come down anytime soon? Prior to spring 2022, we enjoyed nearly three years of sub-4% rates on a 30-year mortgage. In the previous decade, a rate of around 5% was more common. Second, even if rates come down, refinancing might not be the best option. Let’s say you take out a $750,000 mortgage today. After a couple years living with a monthly payment of approximately $5,000, you’ve barely put a dent in the principal. You’ll have to run math based on your own real or hypothetical situation to determine if refinancing is worth it. Closing costs on the refinance (typically 3% to 5% of the loan) may be so high that you won’t actually realize any monthly savings for years. Plus, refinancing may not even be possible after building only a couple years’ worth of equity. The Bottom Line: The Juice can’t remember another time the housing situation was this scary. Knowing if you should buy or sell hasn’t been this complicated in quite a while. It reinforces the money mantra that personal finance is personal. It’s not just about how much money you have. It’s about how much risk and uncertainty you have the appetite for. Because nobody knows where housing prices and mortgage interest rates will go over the next few years. Not even Realtors and lenders. |

|

News & Insights |

Freshly Squeezed |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |