|

Proprietary Data Insights Financial Pros’ Top Drug Company Stock Searches in the Last 30 Days

|

|||||||||||||||||||||

|

Healthcare |

We Rate J&J… |

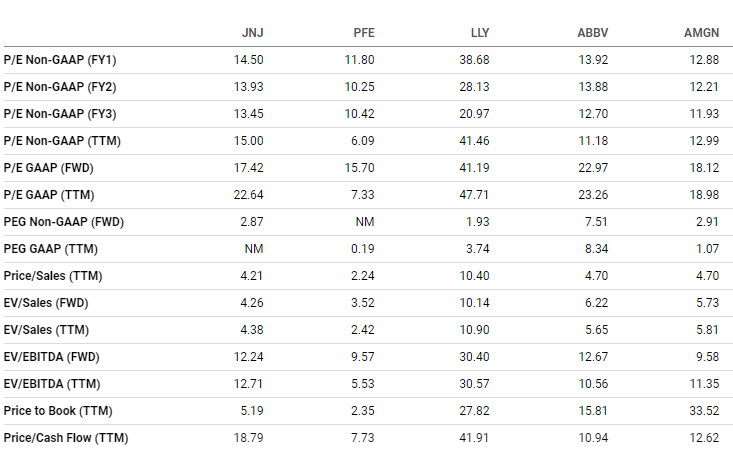

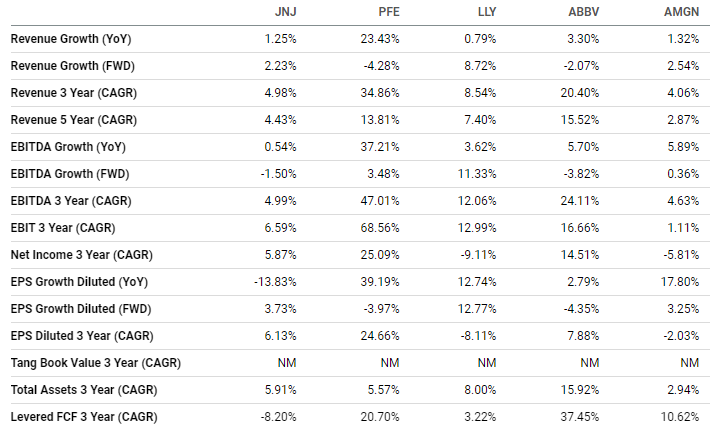

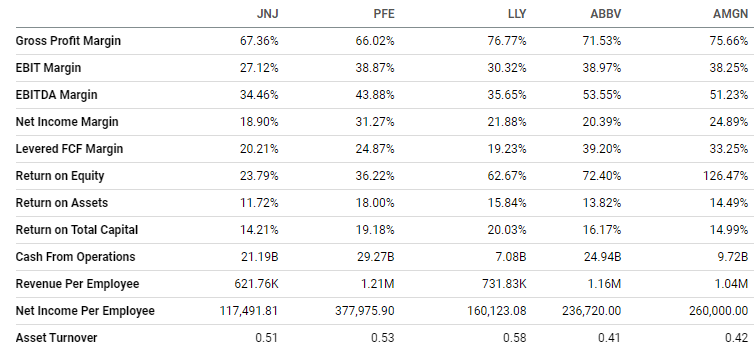

Year to date, the healthcare sector is down just shy of 7%. Johnson & Johnson (JNJ) is down nearly twice that, about 13.6%. Despite a massive pipeline of 109 drugs, with 43 in Phase 3 and 12 being registered, JNJ expects to grow revenues only 2.2% this year. Yet it consistently ranks #2 among financial pros’ searches for drug company stocks. Is there more to this story, or are financial pros just keeping tabs on a portfolio placeholder? Johnson & Johnson’s Business J&J is a diversified healthcare company with 250 subsidiaries it divides into these three areas: Consumer Health, Pharmaceuticals, and MedTech. Source: J&J Q4 earnings presentation Pharmaceuticals make up the lion’s share of the company’s sales, with MedTech (medical devices) about half the size of Pharmaceuticals, and Consumer Health (retail) half the size of MedTech. COVID has been a mixed blessing for J&J. The company’s vaccine made billions. Yet J&J’s MedTech divisions laid off hundreds of workers. Plus, macro headwinds, including inflation, continue to hang over margins. But the pharma unit shows promising growth with Darzalex (for cancer) and Stelara (for psoriasis). Financials Source: Stock Analysis J&J’s sales exploded with its COVID vaccine in 2021. But it expects them to decline substantially this year. Despite a strong pipeline, the company’s dealing with more generics hitting the market and numerous lawsuits related to talc and opioid products. Gross margins have steadily declined over the years, while operating margins have been pretty steady. But JNJ’s free-cash-flow margin dropped substantially in 2022 as the company faced higher income taxes. While some investors might be concerned with the $26.9 billion in long-term debt and current ratio below 1, J&J holds $23.5 billion in cash and generates more than $20 billion in operational cash flow annually. Valuation Source: Seeking Alpha JNJ isn’t cheap relative to its peers, but it’s not expensive either. Its price-to-earnings, price-to-sales, and price-to-cash-flow ratios are in the middle of the pack. Pfizer (PFE) is notably cheaper, largely due to waning COVID-related sales. Growth Source: Seeking Alpha Interestingly, JNJ’s forward revenue growth isn’t that bad compared to its peers. Only Eli Lilly (LLY) expects growth of over 5%. Otherwise, there’s nothing impressive across any of these companies considering the impact of COVID. Profitability Source: Seeking Alpha We were struck by how poor JNJ’s EBIT margin was compared to its peers. That flowed through to it having the lowest net income margin too. While it delivered decent returns on equity, assets, and capital, it was never at or near the top in those categories. Our Opinion 5/10 JNJ seems like a value trap, and not even a good one. We think it’s not worth buying unless it drops from its current $153.89 a share closer to $100. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |