|

Proprietary Data Insights Financial Pros’ Top Automotive Stock Searches in the Last Month

|

|||||||||||||||||||||

Why We Pick GM Over Ford |

|

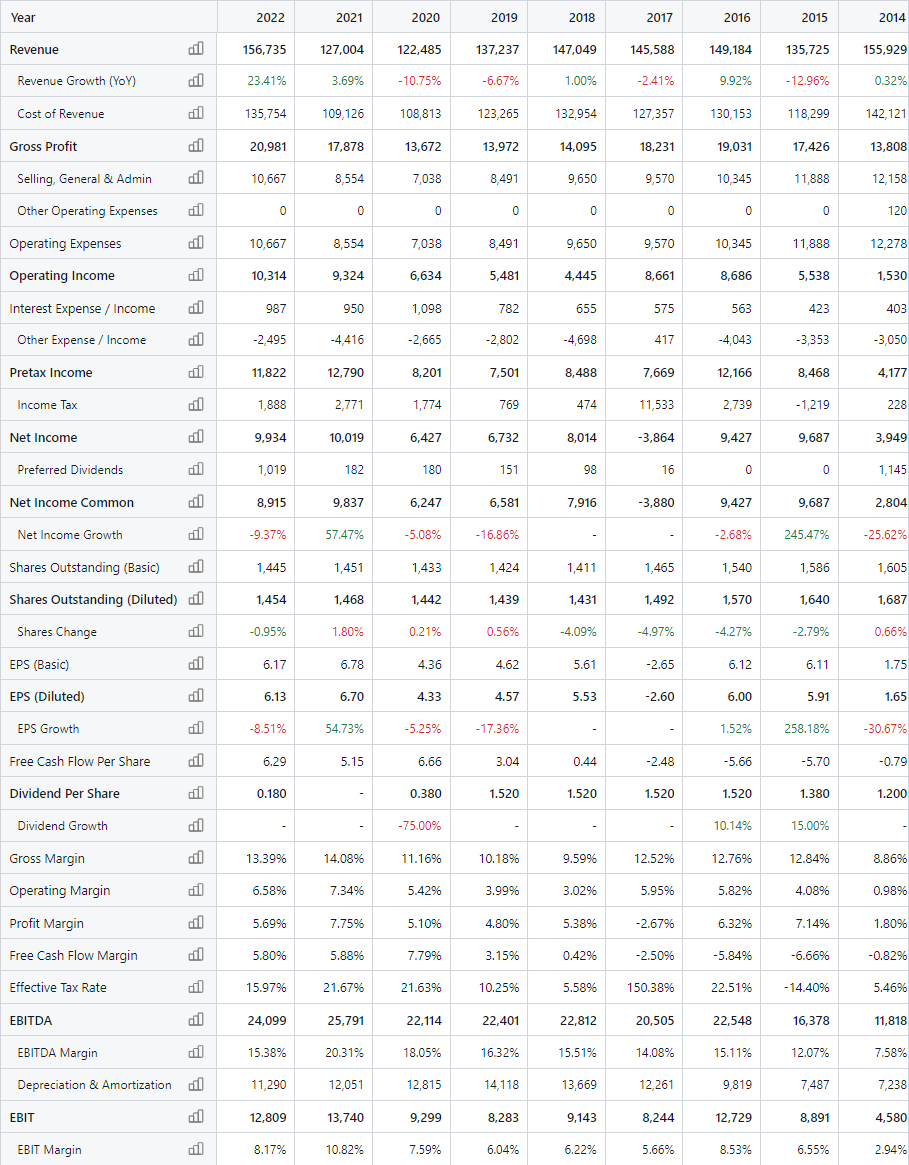

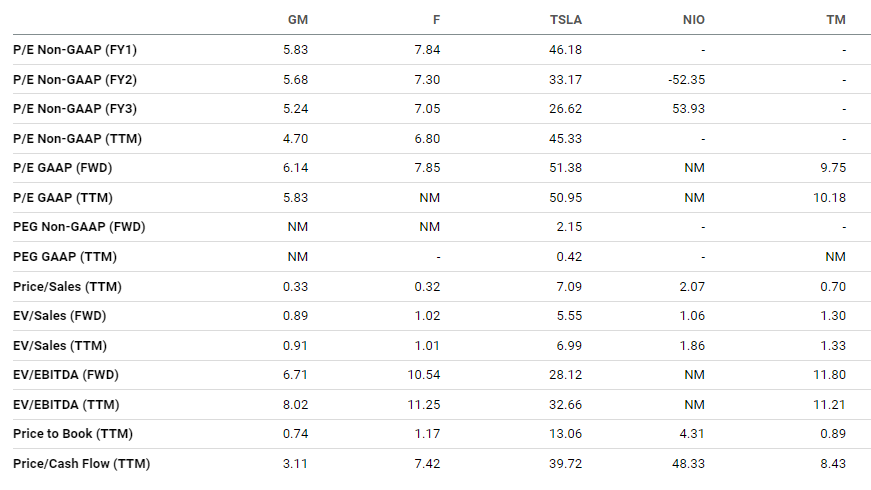

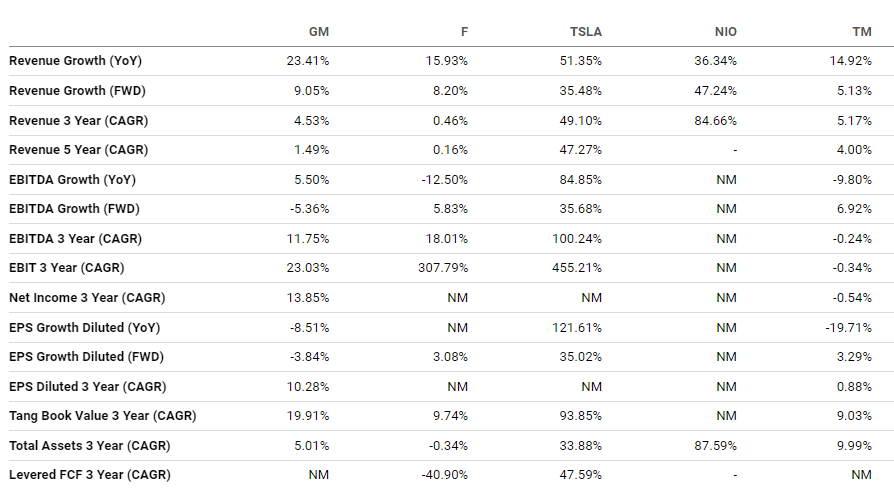

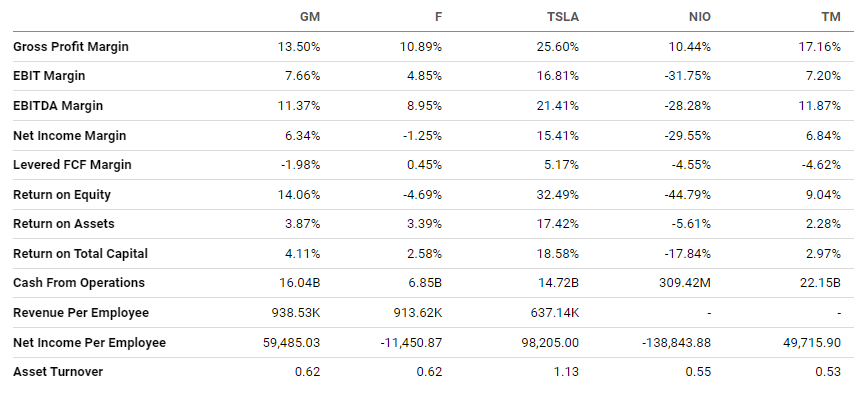

Tesla (TSLA) is still the undisputed leader in electric vehicles. But America’s biggest automakers are nipping at its heels. Today, we look at General Motors (GM). According to our proprietary Trackstar database, there was a startling surge in retail searches for the stock over the past 14 days. Ford (F) aims to go 100% electric by 2030. GM’s shooting for 2035. Interestingly, both garner the same annual sales. But GM’s stock is slightly cheaper than Ford’s. And we think GM’s a better buy… General Motors’ Business Since 1908, General Motors has produced automobiles from its headquarters in Michigan. Although GM International (GMI) sells roughly as many vehicles as GM North America, GMI barely turns a profit. This has been a perpetual problem for the company, which divested from its European operations in 2017 after 20 straight years of losses. Meanwhile, more than a decade after the financial crisis, GM’s financial arm still makes up a sizable, albeit smaller, portion of the company’s profits. The company’s inventory has recently bounced back from supply chain shortages, though it’s below pre-pandemic levels. Inflation also took a bite out of profits, costing GM $5.5 billion in 2022. The company expects to spend $35 billion through 2025 on electric and automated vehicle development. Financials Source: Stock Analysis Despite growing commodity pressure, GM has managed to improve its margins in most categories. This is largely thanks to higher sticker prices padding the bottom line. GM has a whopping $27 billion in cash on its balance sheet as it ramps up spending on research and development. Long-term debt has held steady around $15.5 billion, while divestiture debt sits around $60 billion, with another $36.8 billion due within the next year or so. Interest expenses cost the company as much as 10% of its operating income, which is a lot. Valuation Source: Seeking Alpha GM trades for incredibly cheap based on both its price-to-earnings and price-to-cash-flow ratios. Ford is more expensive, but not by much… Growth Source: Seeking Alpha At first, one might assume growth is behind the discrepancy between Ford and GM. But both have roughly the same revenue growth looking backward and forward. And Ford’s earnings growth isn’t much better. Profitability Source: Seeking Alpha GM does better than Ford across nearly every profitability measure, including returns on equity, assets, and total capital, not to mention cash from operations.

Our Opinion 8/10 We can only assume Ford trades at a higher multiple because of its more ambitious EV targets. But GM generates so much more cash for similar revenues, it’s hard to ignore the company’s value. That’s why we’re more inclined to pick GM here as we abandon post-pandemic inventory shortages and move toward an EV future. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |