Near this time in 2012, I wrote a piece called “Expensive High Yield.” In it I argued that higher quality high yield bonds were overvalued, but that CCCs might still have some play.

Here was my conclusion:

Whether I look at the Merrill High Yield Master 2, BBs, or Bs, junk bonds look expensive. CCCs look a little cheap. The yields on the High Yield Master 2 look about 0.8% expensive in terms of yield (that’s the residual in the above graph). I will be lightening credit bond/loan positions in the near term. Of course this is just my opinion, so do your own due diligence.

And, please realize that movements in the stock market may swamp my observations. If the stock market runs, high yield can run further… but there will be an eventual snap-back. The bond market is bigger than the stock market, eventually the stock market reacts to bond market realities.

So what happened? The stock market ran, and all corporate bonds tightened, Investment Grade and Junk. Yield seeking continued, as people look for ways to earn 4% without undue risk.

But tonight I want to take a slightly different approach than last year, daisy-chaining the overvaluations in the corporate bond market. I’m using the same data as last time — the indexes are the Merrill Lynch Corporate Yield Indexes as published at FRED of the St. Louis Fed.

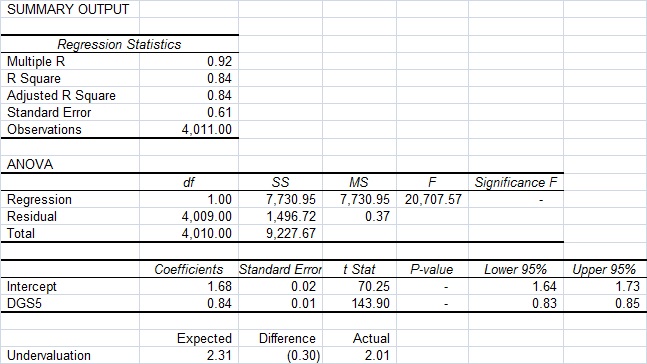

The baseline for corporates are the few large AAA issuers. The first check is whether AAAs are overvalued versus history. Here are my regression results:

Okay, what this shows is that the concept of spread over Treasuries even at the AAA level is not valid. The odds that the true coefficient versus the 5-year Treasury is one is minuscule.

This says that spreads on AAA bonds should widen when Treasury rates are low. It also indicates that the simple model expects AAA yields to be 0.30% higher than they are now.

Perhaps that stems from the actions of the Fed, which they are now perhaps beginning to regret. There are real costs when you force people to take more risk to get income.

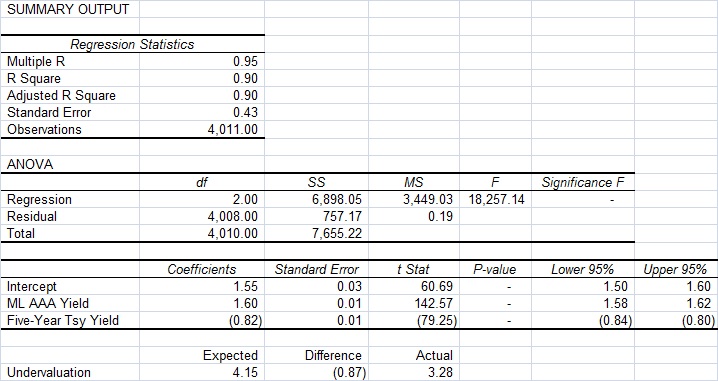

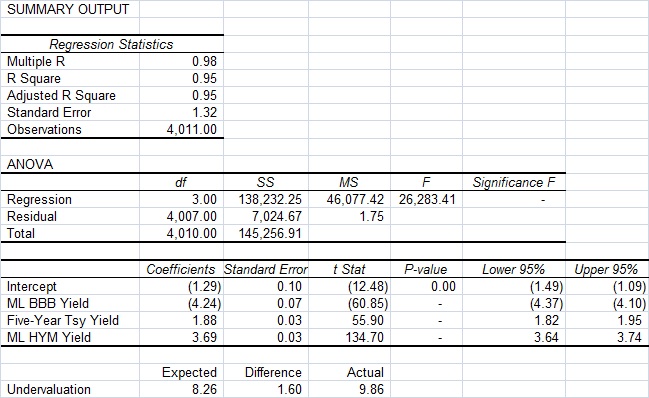

My next step is to consider BBB bond yields as a function of five-year Treasury yields, and the Merrill Lynch AAA bond index yield.

The current environment shows a great deal of desire for yield. BBB bonds are 0.87% lower than they should be relative to history. If I used what the earlier model said the AAA yield would be this would look worse by maybe 0.50%.

Perhaps that reflects the effects of QE as well, but with more vigor, as higher yields get competed down more.

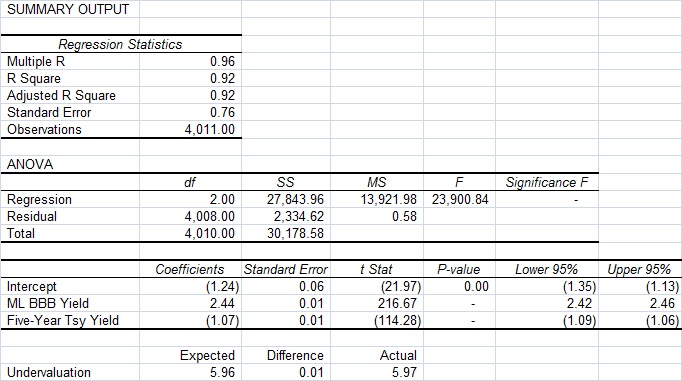

That brings me to the next link in the chain, where I compare Merrill High-Yield Master II versus their BBB index.

Now, relative to where BBB bonds are currently priced, junk bonds are fairly priced versus history.

I would still argue the BBBs are too tight versus history, which means the same for the High-Yield Master.

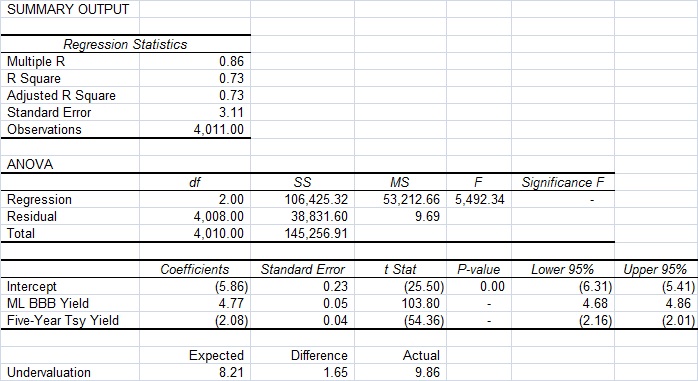

That brings me to look at the yields on the CCCs. I played this on two ways. First, like the way with the high yield master:

In this case, it looks like CCC bonds are still relatively cheap to BBBs. Let’s try a slightly different specification, because CCC bonds have equity-like aspects far more than BBB bonds.

So why not add in the high yield master?

It doesn’t have much effect on the ultimate result. CCC bonds still look relatively cheap. Do I trust this result? No.

All that said, all of this points to a kind of exponential effect with respect to yields on various bonds with credit ratings. Bond categories are highly correlated to those that are near them, but often negatively correlated to those a step or two beyond, when regressors are considered as a group.

Summary

All of the corporate bond market is expensive relative to history, perhaps excluding CCC bonds. That doesn’t mean it can’t get more expensive, particularly if stocks continue to move upward. But this won’t last for more than two years; the signs of speculation are here, and that should make us cautious.

As a result, I am investing my bond strategy cautiously now. What little yield I get comes from emerging market sovereigns. Credit risk from corporates is small.

By: David Merkel, CFA of alephblog

The post CCC Bonds Comparative Basis To BBB: Using Regression Analysis appeared first on ValueWalk.