New bank regulation focused on the so-called Leverage Ratio is expected to do major damage to the US repo market. The measure is a blunt tool that does not permit any netting. That means if a client has a repo trade with a bank and an offsetting (reverse repo) transaction, the two can not be offset. Furthermore, the Leverage Ratio will show double the exposure by grossing up the transactions.

According to JPMorgan, this inability to offset positions will result in some $180bn of new capital requirements for major banks.

JPMorgan: – The inability of banks to offset repos against reverse repos could increase the denominator of the Leverage Ratio by up to $6tr. Applying the 3% minimum capital requirement to this $6tr potentially results in additional capital of $180bn across G4 banks.

That is expected to shrink the market considerably. And lower repo balances will reduce trading and liquidity in the underlying securities – the two markets are closely tied.

|

| Source: JPMorgan |

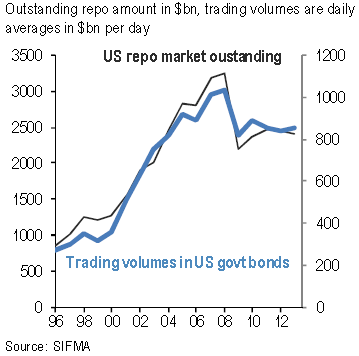

Some 80-90% of repo trades are collateralized with government securities, which will see declines in liquidity as the new rule goes into effect.

In 2008 financial institutions faced a major liquidity crisis that was in large part the result of short-term financing of highly illiquid securities. In order to address these problems, the regulators are now attacking the most liquid part of the market – the exact opposite of where they should be focusing. Ironically these new rules may actually introduce additional risks into the financial system by cutting trading volumes and reducing secured lending against government bonds, both of which are essential in a liquidity crisis.

From our sponsor: