Here’s Kevin Erdmann (aka kebko):

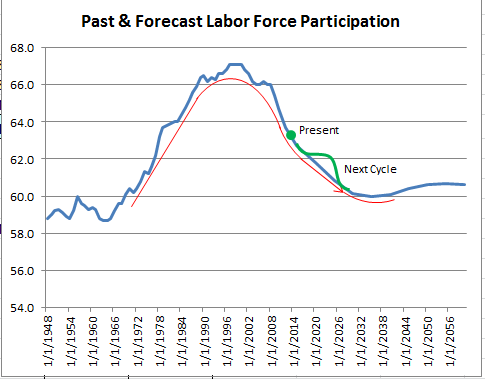

Here is the forecast, appended to actual past LFP rates (in blue):

..................The most important thing to note here is that the current slope of the line basically tracks the slope we have seen since 2000. You don’t need a disillusioned labor force that’s given up in order to explain this decline.

There are periods in the late 70′s, late 80′s, late 90′s, and mid-oughts, where LFP goes above trend during especially strong labor markets. The sharp curvature of the curve makes it hard to see these, but once we correct for this trend, there is nothing special about LFP behavior.

One mistake I see a lot of people making is that they compare the current LFP rate to the rate at the peak of 2007, so they are capturing all of the cyclical variation plus 6 years of a very sharp secular decline. Because the secular decline started in the late 90′s, conventional wisdom also attributes the secular trend in the labor market of the 2002-2007 recovery to a weak recovery. In truth, the LFP in 2007 was well above trend, and a very strong labor market was masked by demographics. So the demographic factors here tend to be dismissed as a result of placing errors on top of errors in our analysis.

I don’t have strong views on this subject, but his analysis seems plausible to me.

This also reminded me that it can be misleading to compare “depressions” in tiny countries with depressions in huge countries. A tiny country like Latvia can produce at a level much further above it’s natural rate than a very large economy like the US. Thus a 25% drop in RGDP from the peak might lead to a milder depression in Latvia than in the US.

PS. The labor market is still in bad shape. But if it was in as horrendous shape as the employment numbers suggest, then I very much doubt Obama would have easily been re-elected. The 7.4% unemployment rate captures the current situation pretty well. And that’s still a bad economy.