Yesterday the Eurozone received some positive (though largely symbolic) news. Moody’s decided to upgrade the rating on Greek government debt from C to Caa3. It’s an important psychological step for the area because Greece was the flashpoint for the Eurozone crisis. Here is the rationale for Moody’s action:

Moodys: –

(1) The significant fiscal consolidation that has taken place under Greece’s structural adjustment program despite low growth and political uncertainty. As a result, Moody’s expects that the government will achieve (and possibly outperform) its target of a primary balance in 2013, and record a surplus in 2014 in accordance with the adjustment program.

(2) The improvement in Greece’s medium-term economic outlook supported by a cyclical recovery in the economy and also the progress made in implementing structural reforms and rebalancing the economy.

(3) The significant reduction of the government’s interest burden following previous restructurings and official sector repayment assistance.

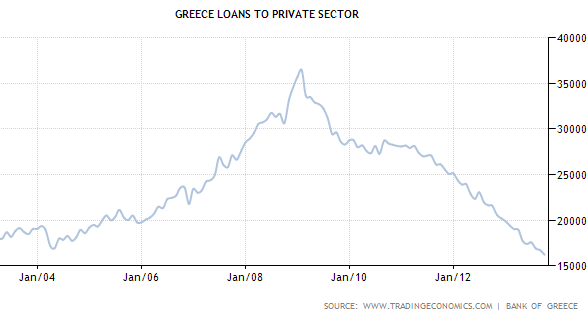

To be sure, most economic data out of Greece continues to resemble a full-scale depression. The unemployment rate is at 27% and youth unemployment is at 57%. Credit to the private sector has fallen 56% from the peak and continues to decline. Manufacturing, new orders, industrial production, retail sales, etc. are all contracting (though the rate of contraction has slowed). Moody’s nevertheless is betting on the following:

1. The country’s debt to GDP ratio, while still horrible, seems to be moving in the right direction.

2. With the domestic demand in shambles, the nation’s current account is in the black. To the extent some of the planned reforms are implemented, the economy could benefit from this trend. Also as discussed last summer (see post), Greek businesses have been showing surprising optimism. Moody’s is hoping that all this will eventually translate into a “cyclical recovery in the economy”.

3. As discussed last year (see post), the restructured Greek government debt (including the EU/EFSF loans) carries extraordinarily low interest burden and extended maturities, giving the Greek government a great deal of flexibility. This is Moody’s third reason for the rating upgrade.

The bond markets have been reflecting these improvements for some time and the upgrade should have relatively little impact on yields.

|

| Greek 10y government bond yield (source: Tradingeconomics.com) |

While the upgrade comes as welcomed news, major risks to Greek economic recovery and fiscal stabilization remain. Apart from some nasty political risks (see story) as well as pressure from the Eurozone leadership and the IMF, Greece is facing two key concerns that are tied into the rest of the Eurozone periphery:

1. The banking system remains all but frozen, with nonperforming loans, undercapitalization, and poor deposit base hampering credit creation. Achieving a sustainable economic recovery will be extraordinarily difficult unless this issue is addressed.

2. Persistent strength in the euro (in spite of tepid economic data) is believed to be detracting from the overall economic growth across the Eurozone. Strong currency is particularly painful for the more vulnerable nations that depend on exports. Further increases in the value of the euro could make the situation worse.

From our sponsor: