In trying to assess the trajectory of the US economy, one is struck by the recent divergence between the manufacturing and the services sectors. Manufacturing in the United States has picked up steam recently in spite of some weather-related headwinds (see chart). The service sector on the other hand took a turn for the worse, which is negatively impacting the labor markets in this service-oriented economy (see story). A couple of key indicators point to slower non-manufacturing activity:

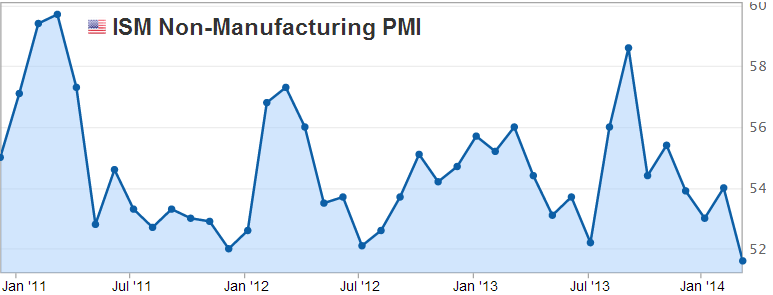

1. The ISM non-manufacturing PMI came in at the lowest level in years.

|

| Source: Investing.com |

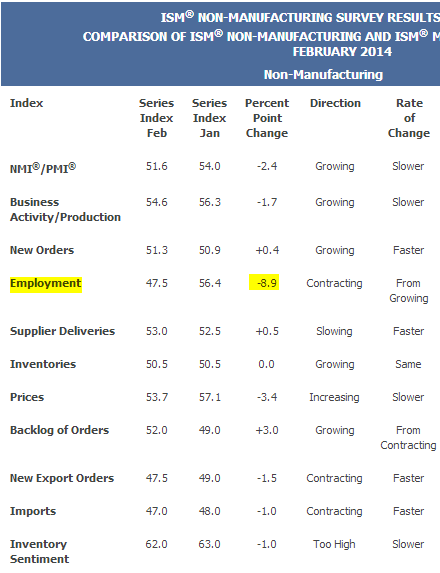

The detail behind the decline shows the big hit to employment in the service sector, which is what we see in the ADP private payrolls today.

|

| Source: ISM |

2. The Markit PMI measure paints a similar picture.

Markit: – Adjusted for seasonal influences, the final Markit U.S. Services PMI™ Business Activity Index dipped sharply to 53.3 in February, from 56.7 in the previous month. Although the index was above the 50.0 no-change mark and signalled a solid pace of expansion, the latest reading was the lowest since October 2013 [US government shutdown]

Most analysts blame this weakness in the service sector and the resulting softness in the labor markets on the weather.

ISI: – There’s hardly a lamer excuse than weather, but that’s probably the case for ADP’s +139k for Feb. It presents downside risk to our best guess for payroll employment of +185k.

Markit: – With the exception of last October, when the government shutdown hit the economy, the service sector grew at its slowest rate since March of last year. This time, the extreme weather was to blame for the slowdown.

If that is indeed the case, as temperatures cimb, we should see a material rebound in service oriented businesses and therefore some big improvements in the jobs picture later this spring. That would mean more Fed taper and higher yields.