Note to the reader: “High-frequency trading” also known as “HFT” is done by firms established for sole purpose of gaining an unfair advantage over other stock market participants. Please keep that in mind as you read on.

Why has the Securities and Exchange Commission (SEC) failed to abolish HFT? Wasn’t the 60 Minutes report about illicit HFT enough to shame the agency? Or will the American public need to wait a few years for the Hollywood movie to come out?

After 80 years of practice, is today’s SEC really better than previous versions from previous eras? What did the SEC learn from its recent colossal failures to protect the investing public like the Enron, Madoff, and mutual fund late trading scandals (Nasdaq:VFINX)? Remember Harry Markopolos?

What’s the real purpose of HFT? Does the SEC know? Is it really to create market liquidity as purported?

Isn’t it true the only market liquidity HFT seemingly create is purely incidental to their other dishonest activities, which always take priority? What legitimate and legal purpose does quote-stuffing by HFTs really serve? How does it benefit real buyers and sellers? Or does it help HFT to front-run stock trades?

AUDIO: Wall Street HFT Scandal Exposed, Momentum Stocks Begin to Lag (Ron DeLegge talks with Eric Hunsader, CEO at Nanex.net)

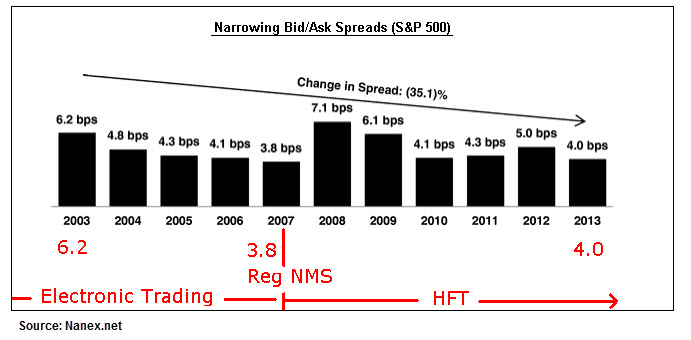

What about allegations that HFT narrows bid/ask spreads (NasdaqGS:NDAQ)? What does the data show? Isn’t it factually true that since Reg. NMS was initiated in 2007, bid/ask spreads have widened? (See chart below) How does this prove the frictional costs of stock market investing have been reduced?

What about all the research studies showing that HFT is good for the stock market (NYSEARCA:SCHB)? What about it? Why does the SEC rely on industry sponsored HFT research studies to govern its affairs? Is it really to help the SEC to properly monitor the trading in financial markets (SNP:^GSPC)? Or is it to solidify the SEC’s relationship with Wall Street? Is the SEC that short on money that it can’t afford to buy independently produced conflict-free research?

What’s the identity of the SEC official that told Brad Katsuyama to get out of the way of HFT firms? Has that person been fired?

Since when is protecting HFT cheating the SEC’s definition of “fair and orderly markets?” Isn’t it the SEC’s job to protect the investing public instead of the unlawful interests of HFTs? Has the SEC become a corrupted accomplice to HFT? When will the SEC live up to its theoretical premise of building an even-playing field in the stock market (NYSEARCA:DIA)?

What did the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 do to protect the investing public? For instance, did the Act outlaw HFT cheaters? And since the Act mentions the word “reform” in its title, what did it do to correct and reform rogue regulators?

Why haven’t any of the currently serving SEC commissioners been fired over the HFT scandal? Were they unaware of illicit HFT rigging or did they endorse it? What about previously serving SEC commissioners? Did they know about HFT front-running? And if they did, why did they allow it to happen? Isn’t it time the law imposes financial clawbacks for financial regulators who show a dereliction of duty? Who’s policing the police?

Why are the FBI and DOJ investigating HFT? Isn’t that the SEC’s job? And if the SEC isn’t capable of executing its public duty, why not just consolidate the agency into another governmental department? Maybe foreign affairs?

To read more about the epic incompetence of regulators, see “Gents with No Cents: A Closer Look at Wall Street, its Customers, Financial Regulators, and the Media” by Ron DeLegge II. Mr. DeLegge is also publisher of the ETF Profit Strategy Newsletter exclusively available at ETFguide.com.

Follow us on Twittter @ ETFguide