Encouraging and supporting asset bubbles is essentially the only force remaining to keep the system intact as we know it.

The Singularity is based on the idea that machine intelligence will soon exceed human intelligence, and human history is unknowable beyond that point. This concept draws from a variety of sources, but for me the foundational idea comes from the physics of black holes, in which gravity concentrates the material of a collapsing star into a point of infinite gravitation, i.e. a singularity, that is surrounded by an event horizon that marks the line beyond which observers will inevitably be pulled to their destruction in the black hole. Observers cannot go back once they cross the event horizon, but they cannot see the inside of the black hole without going beyond the event horizon.

Longtime correspondent B.C. recently proposed that the global stock markets have reached a Financial Singularity in which trading machines now control the markets. Here are excerpts of B.C.’s emails on the topic:

In some respects, “The Singularity” has occurred in the financial markets, only humans are incapable of perceiving it except by inference.I will reiterate from the past my assertion based on direct and highly suggestive personal evidence that the major US, UK, and EZ equity markets are being “managed” offshore by the TBTE (too big to exist) banks’ dark pools’ pass-through entities in the Caribbean banking centers, levering up US Treasury and MBS (mortgage-backed securities) holdings to jam equity index with the assistance of NYSE-Euronext exchange-sponsored HFT (high fequency trading) at the price margin.

Were the discerning investing/speculating public to learn of the process, its objective, and successful outcome to date, I strongly suspect that most would approve, permitting the scheme to become institutionalized and expand to additional asset classes.

Within this context, then, in the event of another bear market or crash, I fully expect the central banks will overtly print to buy bank and insurer stocks, as well as equity index futures, perhaps not unlike the way POMOs are conduct with weekly announcements about purchases, run-offs, rollovers, and various portfolio-balancing actions. There is nothing in the Fed charter that would prohibit any of this.

Given the hyper-financialized economy and society we now have, including profits of 10-11% og GDP, financial profits/GDP at 4.5-5%, and net annual flows to the financial sector exceeding annual growth of nominal GDP, banking system liquidity, leverage, and bank book entry profits, encouraging and supporting asset bubbles is essentially the only force remaining to keep the system intact as we know it. (CHS emphasis added)

The Fed officials and their TBTE bank owners and their rentier Power Elite owners and benefactors all know this better than anyone, and I cannot today conceive of why they would pull the plug on the bubble-pumping process at this point.

Though the fat thumb of manipulation has long been discernable in market action– the “ramp and camp” of up days, when markets open high and stay there with virtually no change, the absurd regularity of end-of-the-day “saves” when a down day is magically reversed in the final minutes into an up day–there is a mountain of more direct evidence that central banks and states are propping up markets to serve their perception management purposes: an ever-rising market projects an image of prosperity and rewards the few who own the assets bubbling higher in value.

It’s Settled: Central Banks Trade S&P500 Futures (Zero Hedge)

B.C. went on to explain why the Elites who own most of the stock market wealth have no need to sell their shares, even in a sharp decline:

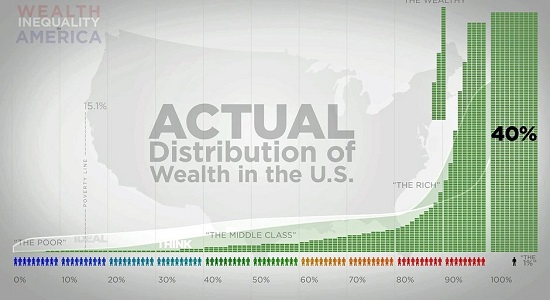

With 40% of financial wealth concentrated to the top 1% and 85% in the top 10%, and the largest share of increase in net flows and income derived therefrom within the top 0.1-0.5% (increasingly circulating between the top-performing hedge funds, private equity, etc.), one can make the case that wealth and income inequality is in effect as high as it has ever been, even going back to the 19th century when most people had farms/homesteads, livestock, equipment, timber, and lived in villages and towns with little access to credit and a cash economy.Today, the bottom 80-90% have effectively no net financial wealth outside of imputed real property “equity”, which is in effect the lender’s “equity” until the mortgage debtor borrows his own “equity” from the lien holder.

This extreme wealth inequality and hoarding of overvalued financial assets at no velocity in the rest of the economy exacerbates the drag effects of indebtedness of the economy, reducing velocity further and growth of economic activity overall.

The unprecedented hyper-financialization and associated indebtedness and wealth concentration permit the financial markets, and the top 0.1-1% who own a controlling share of the assets, to increasingly detach from the activity of the underlying economy, which is effectively not growing per capita and after price changes.

This situation is similar to Japan since the early 2000s and in the late 19th century, although the dividend in the 1890s-1900s averaged 5% compared to 2% today. But the low dividend, low or no prospective real total return, low inflation, slow or no growth of real final sales per capita, and low discount rate is practically Nirvana-like conditions for the top 0.1-1% rentier hoarders.

Because of the low discount differential to rates, dividends, and expected CPI, equity implied volatility will be lower but so will total returns. The top 0.1-1% are in “the domain of gains” and can afford NOT to need to earn a return above the low discount rate

In other words, those who own most of the financial assets and receive the largest net flows and income from financial assets don’t have to sell, nor is there a net benefit from selling at the low capital gains tax rate and 0-2% discount rate.

If those who control leverage and equity index futures prices and forward hedging at the margin are similarly influenced and situated, which they generally are, they have little motivation to pull the plug and ruin nearly perfect conditions for maintaining the status quo.

That’s a long-winded explanation for “the top 0.1-1% don’t need to sell, therefore, they won’t.”

Thank you, B.C., for explaining the Financial Singularity: those programming the trading bots and high-frequency trading machines have every incentive to push equity valuations ever higher, and no meaningful incentives to sell. Meanwhile, J.Q. Citizen is delighted to see his IRA, 401K, pension fund, etc., rise in value due to the permanent levitation of stocks.

The question all this raises in my mind: could all these forces of financial gravitation lead to an unforseen implosion, a financial black hole that neither money nor wealth can escape? Those operating the machines are confident they control all the inputs and can calibrate the Financial Singularity to produce the desired output: ever-higher stock markets.

But complex systems are not entirely controllable–even with the amassed intelligence of thousands of trading bots and HFT machines. The only way to control the markets is to own all the assets, and perhaps that is the end-game of the Financial Singularity.

The ideal Back-to-School reading for high school/college seniors:

Get a Job, Build a Real Career and Defy a Bewildering Economy,

a mere $9.95 for the Kindle ebook edition and $15.47 for the print edition.