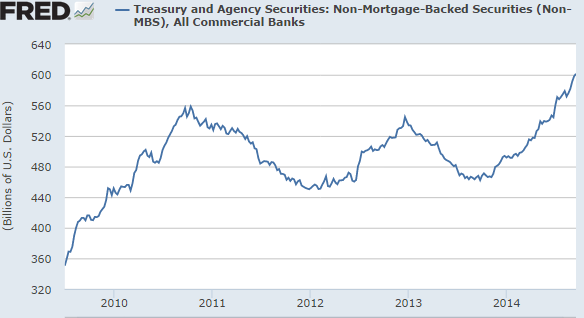

One of the factors contributing to treasury market’s strong performance this year has been the Liquidity Coverage Ratio (LCR), a Basel III-based requirement for banks. These rules go into effect in 2015 and are phased in gradually through 2017 in the United States (the implementation period is longer in some countries). LCR requires that banks hold sufficient amounts of liquid assets to withstand a significant loss of funding sources (such as depositors withdrawing). This need for liquid assets has resulted in banks accumulating treasuries – which they’ve ramped up to record levels this year – and to a lesser extent GSE debt.

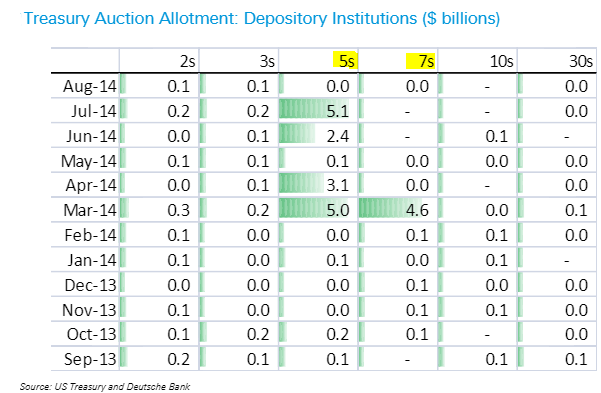

One would expect banks to buy treasury bills or short-term notes to meet their LCR requirement but that did not turn out to be the case. Lenders showed willingness to take rate risk and ended up focusing on 5- and 7-year paper.

|

| Source: Deutsche Bank |

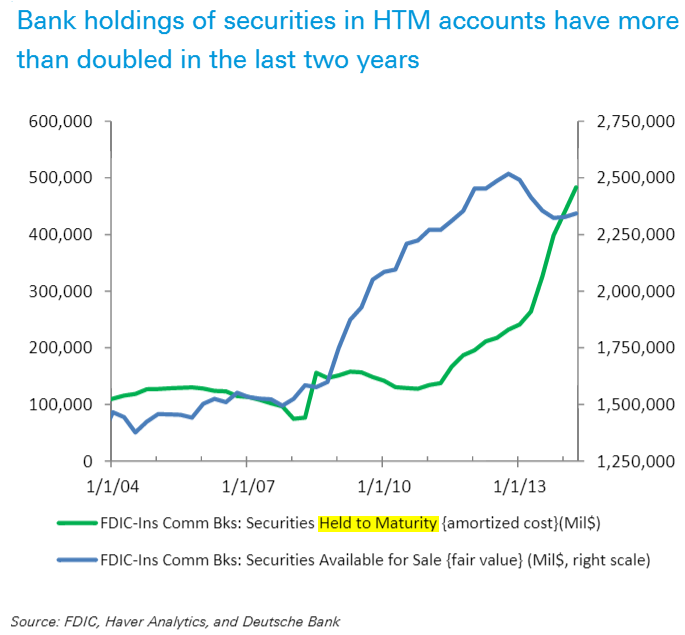

It seems that the bulk of recent purchases have been placed into the so-called “Held-to-Maturity” (HTM) accounts as opposed to “Available for Sale”. HTM accounts allow banks to avoid mark-to-market treatment, accruing the coupon and accreting/amortizing discount/premium. At current extraordinarily low cost of funds banks can generate a positive net interest income on these intermediate-term notes while “avoiding” rate risk using HTM accounts. Treasury bills on the other hand would have resulted in interest income that is below interest expense.

|

| Source: Deutsche Bank |

The question for fixed income investors is how much more will banks be forced to buy in order to comply with the LCR rules. According to DB, most US banks are nearly there.

DB: – Deutsche Bank’s bank analysts believe most banks have already added the highly liquid assets they would need for LCR, and the industry is about 80% to 90% there. Therefore, LCR-related bank demand for Treasuries could continue, although the majority of flows might have occurred.

The answer also depends on how quickly deposits continue to grow going forward because LCR requirements are partially based on the size and stability of deposit-based funding. Deposit growth in the US has remained fairly steady at around 7.5% per year. If this trend continues, we should see LCR-based demand for treasuries decline to more moderate levels in the near-term.

_________________________________________________________________________

Sign up for our daily newsletter called the Daily Shot. It’s a quick graphical summary of topics covered here and on Twitter (see overview). Emails are distributed via Freelists.org and are NEVER sold or otherwise shared with anyone.

From our sponsor: