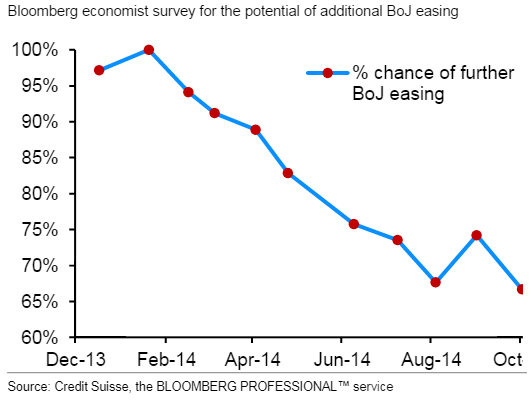

Expectations of Bank of Japan accelerating securities purchases at the October meeting have fallen considerably. Majority of economists now expect any type of change in policy to take place no earlier than December/January, if ever. In fact an increasing proportion of Japan watchers are suggesting that faster securities purchases are unlikely to take place at all. The chart below shows the percentage of those who believe further easing is imminent.

|

| Source: Credit Suisse |

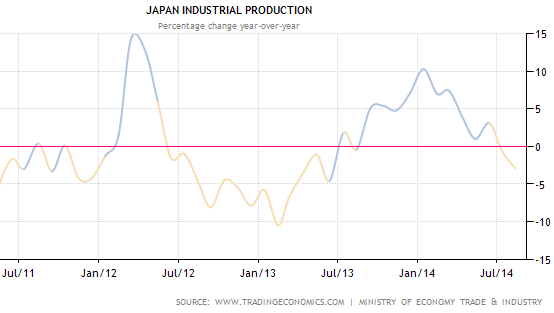

This relatively sudden change in views is not due to any significant economic improvements in Japan. Japan’s consumption tax hike has created a material drag on growth, with industrial production starting to decline again.

The BoJ in fact admitted that a substantial slowdown is taking place and the tax hike is to blame.

WSJ: – The Bank of Japan said Tuesday that industrial production was showing signs of weakness, acknowledging for the first time since the sales tax was raised in April that the move has had a notable negative impact on a key driver of economic growth.

The admission confirms what private economists have been stressing for months—that the higher tax rate has taken a significant toll on the economy. It also comes as a separate government indicator pointed toward the possibility that Japan may have already entered a recession.

In a statement released after a two-day meeting, the BOJ’s policy board maintained its assessment that the economy “continues to recover moderately as a trend,” but that “some weakness, particularly on the production side, has been observed.”

Moreover, the central bank’s 2% inflation target remains elusive. Inflation expectation (breakeven) implied by the 10-year JGBs is barely above 1%.

|

| Source: Japan Bond Trading Co |

So why do many economists now think the central bank is not going to accelerate QE – at least not in the nearterm? The reason has to do with the increasing uncertainty around the benefits of a weak yen (discussed here). While large exporters benefit from currency depreciation, smaller businesses and consumers are hurting.

Bloomberg: – Debate is increasing over the costs and benefits of the weakening yen, which is increasing costs for importers and households while it bolsters profits for some companies. Further depreciation could risk support for the Bank of Japan’s unprecedented stimulus program, even as the government says there is no gap with the BOJ in its stance on the yen. …

Exchange-rate depreciation has raised the cost of imported products including energy, something that’s helped end Japan’s deflation and stoked profits for companies with earnings abroad. Smaller businesses have become increasing vocal in opposing the fall, even as Kuroda says that the negative effects are outweighed by the positive.

Kuroda was told by business leaders in the industrial city of Osaka last month that the yen’s slide was boosting costs of imported fuel and raw materials and may spell trouble for the economy.

With wage growth remaining sluggish (particularly for non-union workers), rising import costs could undermine consumer demand – particularly in the face of higher consumption taxes. Given these headwinds, there may be sufficient political pressure to put the BoJ into a holding pattern.

It is important to point out however that even without adjusting its policy, the BoJ’s current QE effort is by far the most ambitions monetary expansion program by a developed economy in recent history.

_________________________________________________________________________

Sign up for our daily newsletter called the Daily Shot. It’s a quick graphical summary of topics covered here and on Twitter (see overview). Emails are distributed via Freelists.org and are NEVER sold or otherwise shared with anyone.

From our sponsor: