The ability of oil exporters to trigger a short-term collapse in price does not automatically translate into an ability to control the financial conflagration such a crash ignites.

My BS detector went off when two stories with similar headlines touting $20/barrel oil were published on the same day. Color me skeptical, but it’s almost as if mere $40/barrel oil is no longer enough to get the blood flowing, so both stories blared the more extreme $20/barrel price point.

The reason oil could drop as low as $20 per barrel

Neither story depicted $20/barrel oil as a brief spike–rather, each presented a future of sub-$50/barrel oil that could last for years or even a decade or longer, matching the period of cheap oil that ran from the mid-1980s to the late 1990s.

I have no problem with the idea that geopolitics is driving supply excesses, the goal being to crash the oil revenues of enemies–that’s part of my Oil Head-Fake scenario: The Oil-Drenched Black Swan, Part 4: The Head-Fake Disruption Ahead(December 4, 2014).

The Financialized-Oil Dominoes Are Toppling (December 12, 2014)

The idea that global demand is stagnating is also common sense, given that the global economy is stagnating.

What seems less well-supported is the notion that any single oil exporter can single-handedly pump enough crude to keep prices at $20 or even $30/barrel for years or even a decade. Remarkably, few analysts seem to question this; it’s as if the extended period of low oil prices in the 1985-1999 time frame has generated an unquestioned faith in the Saudis’ ability to push prices down at will for years on end.

The current era is significantly different from 1985-1999. Let’s list a few of the critical differences.

1. Saudi oil exports make up less than 10% of global oil consumption. Saudi Arabia exported about 7.7 million barrels a day (MBD) in 2013, while total global production was 92.7 MBD and global consumption was 92.3 MBD. (Source: U.S. Energy Information Administration, EIA) Global Petroleum and Other Liquids

2. The OPEC oil exporters’ cartel provides about 40% of all oil produced.

3. Total OPEC surplus production capacity is estimated at 2.5 MBD. This relatively modest capacity is the leverage that can supposedly keep prices down for years on end, regardless of what other non-OPEC producers and major consuming nations might choose to do.

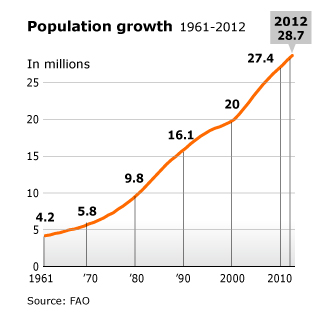

4. The Saudi population has doubled since the mid-80s:

5. Saudi Arabia is the largest oil-consuming nation in the Middle East. “Saudi Arabia consumed 2.9 million barrels per day (bbl/d) of oil in 2013, almost double the consumption in 2000.” (source: EIA) That’s as much as Australia (1.1 MBD) and France (1.8 MBD) combined.

6. These trends–rapid expansion of population, social welfare costs and oil/natural gas consumption–are continuing their upward trajectories. Many other exporting nations have similar profiles: rapidly expanding populations and domestic consumption, hefty fuel subsidies for residents, and expanding social welfare costs.

Saudi Arabia has 16% of the world’s proved oil reserves, is the largest exporter of total petroleum liquids in the world, and maintains the world’s largest crude oil production capacity.(EIA)

An analysis of 7 factors that influence oil markets (EIA)

7. Saudi Arabia and other major oil exporters derive a significant percentage of their national incomes (public and private) from investments in the global financial system–the same financial system that is being destabilized by crashing oil prices.

The collapse in collateral and income is not limited to oil exporters with marginally high costs–everyone with a stake in the interconnected global financial system will suffer losses as the financialized-oil trade unwinds violently and unpredictably.

8. The oil exporters’ ability to control a global financial meltdown triggered by crashing oil prices is nil.

All of which is to say that the ability of oil exporters to trigger a short-term collapse in price does not automatically translate into an ability to control the financial conflagration such a crash ignites, or an ability to effortlessly maintain oil at $20/barrel for years.