Debt saturation and debt fatigue = diminishing returns on central bank tricks.

Debt Brings Forward Consumption & Income

The Only Trick To Expand Debt: Lower Interest Rates

The Trick To Increase Consumption: Punish Savers

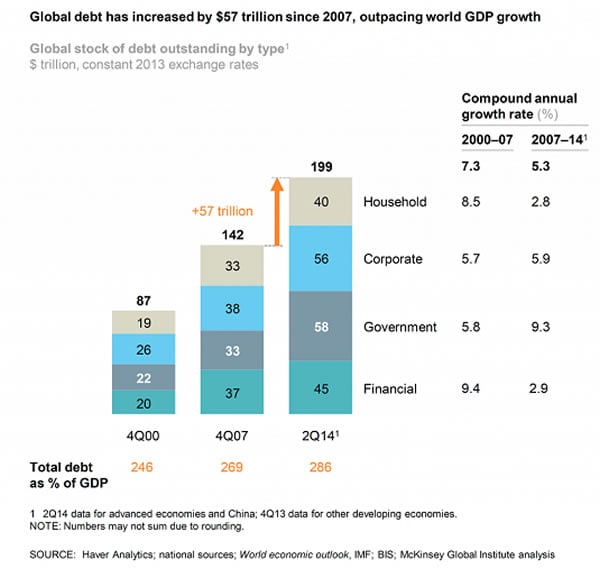

The Global Expansion Of Debt Has Increased Systemic Risks

Get a Job, Build a Real Career and Defy a Bewildering Economy(Kindle, $9.95)(print, $20)

Are you like me? Ever since my first summer job decades ago, I’ve been chasing financial security. Not win-the-lottery, Bill Gates riches (although it would be nice!), but simply a feeling of financial control. I want my financial worries to if not disappear at least be manageable and comprehensible.

And like most of you, the way I’ve moved toward my goal has always hinged not just on having a job but a career.

You don’t have to be a financial blogger to know that “having a job” and “having a career” do not mean the same thing today as they did when I first started swinging a hammer for a paycheck.

Even the basic concept “getting a job” has changed so radically that jobs–getting and keeping them, and the perceived lack of them–is the number one financial topic among friends, family and for that matter, complete strangers.

So I sat down and wrote this book: Get a Job, Build a Real Career and Defy a Bewildering Economy.

It details everything I’ve verified about employment and the economy, and lays out an action plan to get you employed.

I am proud of this book. It is the culmination of both my practical work experiences and my financial analysis, and it is a useful, practical, and clarifying read.

Test drive the first section and see for yourself. Kindle, $9.95 print, $20

“I want to thank you for creating your book Get a Job, Build a Real Career and Defy a Bewildering Economy. It is rare to find a person with a mind like yours, who can take a holistic systems view of things without being captured by specific perspectives or agendas. Your contribution to humanity is much appreciated.”

Laura Y.

Gordon Long and I discuss The New Nature of Work: Jobs, Occupations & Careers(25 minutes, YouTube)

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

| Thank you, Craig H. ($100), for your outrageously generous contribution to this site– I am greatly honored by your steadfast support and readership. |

for the full posts and archives.