The New York Federal Reserve just announced that older Americans are carrying more debt than ever before and, believe it or not, spins this as a good thing:

New York Fed Finds Large Increase in Debts Held by Those Over Age 50

(NASDAQ) – Americans in their 50s, 60s and 70s are carrying unprecedented amounts of debt, a shift that reflects both the aging of the baby boomer generation and their greater likelihood of retaining mortgage, auto and student debt at much later ages than previous generations.

The average 65-year-old borrower has 47% more mortgage debt and 29% more auto debt than 65-year-olds had in 2003, according to data from the Federal Reserve Bank of New York released Friday.

The result: U.S. household debt is vastly different than it was before the financial crisis, when many younger households had taken on large debts they could no longer afford when the bottom fell out of the economy.

The shift represents a “reallocation of debt from young [people], with historically weak repayment, to retirement- aged consumers, with historically strong repayment,” according to New York Fed economist Meta Brown in a presentation of the findings.

Older borrowers have historically been less likely to default on loans and have typically been successful at shrinking their debt balances. But greater borrowing among this age group could become alarming if evidence mounted that large numbers of people were entering retirement with debts they couldn’t manage. So far, that doesn’t appear to be the case. Most of the households with debt also have higher credit scores and more assets than in the past.

“Retirement-aged consumers’ repayment has shown little sign of developing weakness as their balances have grown,” according to Ms. Brown.

An important barometer of household financial health is the percentage of this debt that is in some stage of delinquency, and that percentage has been steadily dropping. Only 2.2% of mortgage debt was in delinquency, the lowest since early 2007. Credit card delinquencies also declined, while auto loan and student loan delinquencies were unchanged.

“The household sector looks much better positioned today than in 2008 to absorb shocks and continue to contribute to the economic expansion,” said New York Fed President William Dudley in prepared remarks.

Part of the yearslong improvement in credit delinquencies owes to the fact that older borrowers hold a growing share of the debt. Not only were borrowers with the best financial situation able to maintain their debt during the financial crisis, they have had an easier time taking on new debts in recent years as credit standards have tightened.

By contrast, the overall debt balances of most young borrowers haven’t grown or have declined. The average 30-year-old borrower has nearly three times as much student debt as in 2003. But these borrowers have so much less home, credit card and auto debt that their overall debt balances are lower.

This shift for young borrowers could have “consequences in terms of both foregone economic growth and young consumers’ welfare,” said Ms. Brown.

When government economists speak, it frequently sounds like they’re teasing their listeners with a parody of “other things being equal” academic nonsense. But then you realize they’re serious…

So here are the obvious, common-sense reasons why the above trends are unambiguously bad:

Older people are carrying more debt not because they’re optimistic about the future but because they’re struggling in the present. Their mortgages aren’t paid off because they’ve used all their free cash on health care and their kids’ upkeep and education. One of the notable features of recent (supposedly strong) US employment reports is the large number of new jobs going to workers 55 and older. The implication is that people who in better times might be retiring are now taking whatever work they can get to make ends meet.

And while it’s true that older people default on their debt less frequently than younger, it’s also true that when economists start extolling low default rates in a given sector it’s generally a sign that that sector is about to blow up. Go back through the history of junk bonds, for instance, and you’ll find the same kinds of statements just before defaults spike. This is from a 2014 Barron’s article:

Junk Bond Default Rate Steady At 2.1% In May – Moody’s

Junk-rated corporate bonds don’t yield much these days, but they don’t default much either. Moody’s just reported that the U.S. high-yield default rate held steady at just 2.1% in May, while the global rate fell to 2.3% in May from 2.5% in April. Things look pretty good for the year ahead too, according to Moody’s:

“Default rates have been remarkably stable as expected. Looking ahead, our default rate forecasting model predicts that the global default rate will edge lower to 2.1% by the end of this year before rising to 2.4% a year from now.

Junk-rated companies have been big beneficiaries of the Federal Reserve’s low-interest-rate policies, which have fueled a clamor for high-yielding debt among investors while allowing companies to refinance older bonds issued at higher interest rates with new, lower-coupon debt. At this point in a normal credit cycle you might see defaults starting to pick up, but this Fed-subsidized credit cycle looks poised to last longer than most.

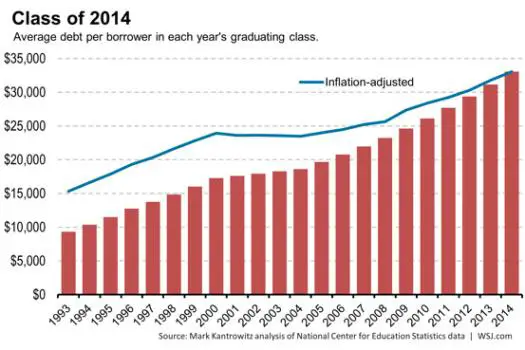

Now about the supposedly-improved finances of younger people: If you’re 25 years old and already carry $30,000 of student debt, you’re not going to borrow much more. The following chart goes through 2014; in 2015 the average rose by another $2,000.

Meanwhile, the jobs available to the relatively-young are skewing towards “service,” which is to say waiters, bartenders, medical receptionists, etc., which don’t pay enough to cover $32,000 of student debt, let alone new car loans and maxed out credit cards.

The upshot: like most evolving financial trends in the developed world, this one is unambiguously bad and getting worse. Debt, once it passes a certain point, sucks the life out of a society and no amount of positive spin can hide this fact from the victims.