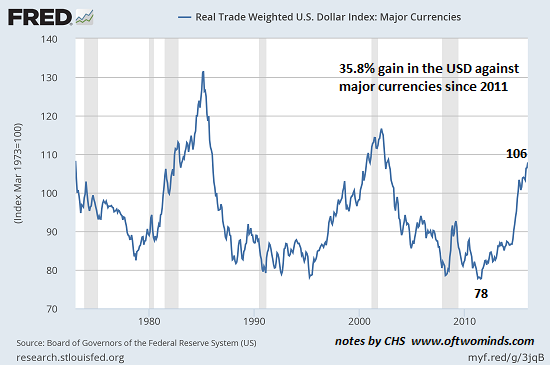

The U.S. dollar (USD) has gained over 35% against major currencies since 2011.

China’s government has pegged its currency, the yuan (renminbi) to the USD for many years. Until mid-2005, the yuan was pegged at about 8.3 to the dollar. After numerous complaints that the yuan was being kept artificially low to boost Chinese exports to the U.S., the Chinese monetary authorities let the yuan appreciate from 8.3 to about 6.8 to the dollar in 2008.

This peg held steady until mid-2010, at which point the yuan slowly strengthened to 6 in early 2014. From that high point, the yuan has depreciated moderately to around 6.5 to the USD.

Interestingly, this is about the same level the yuan reached in 2011, when the USD struck its multiyear low. Since 2011, the USD has gained (depending on which index or weighting you choose) between 25% and 35%. I think the chart above (trade-weighted USD against major currencies) is more accurate than the conventional DXY index.

Due to the USD peg, the yuan has appreciated in lockstep with the U.S. dollar against other currencies. On the face of it, the yuan would need to devalue by 35% just to return to its pre-USD-strength level in 2011. This would imply an eventual return to the yuan’s old peg around 8.3–or perhaps as high as 8.7.

Longtime correspondent Mark G. submitted this article China’s Subprime Crisis Is Here:

The dynamic is clear. A splurge of new lending can help to dilute existing bad loans, but only at a cost. This is a game that can’t continue forever, particularly if credit is being foisted on to an already over-leveraged and slowing economy. At some point, the music will stop and there will have to be a reckoning. The longer China postpones that, the harder it will be.

Mark also submitted the following commentary:

It seems the best way to assess the likely effects and outcomes is to look at what the Chinese government can control, and at what it can’t control. And we should observe at the start that the yuan is not a global reserve currency.

1. Beijing can control the amount of yuan in existence. It can therefore easily pay off all these bad internal debts, at least in a strict book keeping sense. And it can also recapitalize its bankrupt banks to any degree necessary, at least in yuan. The process of doing so involves assigning winners and losers. The latter group will comprise anyone earning a subsistence working wage in yuan and anyone whose assets primarily consist of savings in yuan.

2. Undertaking #1 will lead to a large increase in the amount of yuan in existence. Here Beijing will be acutely sensitive to any increase in food prices since this can swiftly lead to mass food riots and the concomitant rapid and bloody end of the regime. Therefore food prices have to be insulated somehow from this huge internal devaluation.

3. Beijing cannot permanently control the yuan-dollar exchange rate or any other FOREX rate involving yuan. It can do so in the short term but only to the limit of its usable foreign exchange reserves. This total is minus the FOREX working capital China needs to pay for imported raw materials and fuels. And also food: China’s Growing Demand for Agricultural Imports (USDA)

It appears that one certain outcome will be a huge depreciation in the value of yuan. Bailout of the bad bank debt is reason #1 to print yuan. The decline of yuan will lead to lower prices and a temporary relief of U.S.-based automation pressure on export market share. This begins to become a Reason #2.

How this will be received outside China is the immediate question. Probably not too favorably.

One way to paper over impaired loans is to issue a flood of new credit: this dilutes the problem and enables defaulted loans to be “paid down” with new loans that are doomed to default once the ink is dry: China Created A Record Half A Trillion Dollars Of Debt In January (Zero Hedge)

Here’s the larger context of China’s debt/currency implosion. From roughly 1989 to 2014–25 years–the “sure bet” in the global economy was to invest in China by moving production to China.

This flood of capital into China only gained momentum as the yuan appreciated in value against the USD once Chinese authorities loosened the peg from 8.3 to 6.6 and then all the way down to 6 to the dollar.

Every dollar transferred to China and converted to yuan gained as much as 25% over the years of yuan appreciation. Those hefty returns on cash sitting in yuan sparked a veritable tsunami of capital into China.

Now that the tide of capital has reversed, nobody wants yuan: not foreign firms, not FX punters and not the Chinese holding massive quantities of depreciating yuan.

This is why “housewives” from China are buying homes in Vancouver B.C. for $3 million. That $3 million could fall to $2 million as the yuan devalues to the old peg around 8.3 to the USD.

Who’s left who believes the easy money is to be made in China? Nobody. Anyone seeking high quality overseas production is moving factories to the U.S. for its appreciating dollar and cheap energy, or to Vietnam or other locales with low labor costs and depreciated currencies.

For years, China bulls insisted China could crush the U.S. simply by selling a chunk of its $4 trillion foreign exchange reserves hoard of U.S. Treasuries. Now that China has dumped over $700 billion of its reserves in a matter of months, this assertion has been revealed as false: the demand for USD is strong enough to absorb all of China’s selling and still push the USD higher.

The stark truth is nobody wants yuan any more. Why buy something that is sure to lose value? the only question is how much value? The basic facts suggest a 30% loss and a return to the old peg of 8.3 is baked in.

But that doesn’t mean the devaluation of the yuan has to stop at 8.3: just as the dollar’s recent strength is simply Stage One of a multi-stage liftoff, the yuan’s devaluation to 8 to the USD is only the first stage of a multi-year devaluation.

We need a new system, one we control from the ground up:

A Radically Beneficial World: Automation, Technology and Creating Jobs for All. The Kindle edition is $8.95 and the print edition is $20.82.