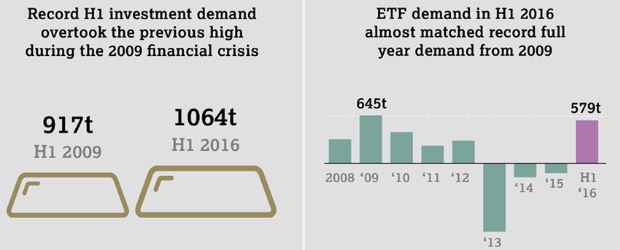

Gold investment demand surged to a record in the first half of 2016 and overtook the previous high seen during the 2009 financial crisis on a “perfect storm” for gold according to the ‘Gold Demand Trends Q2 2016’ report which was released by the World Gold Council today.

Western investors especially in Europe saw the greatest increase in gold investment demand and Europe was the “largest market for gold bars and coins in Q2.”

Gold investment in Germany remained very robust and UK demand rise significantly from low levels as smart money diversified into gold ahead of the Brexit referendum. Japan also saw continuing robust demand due to concerns about the outlook for the Japanese economy, the debasement of the yen and negative interest rates in Japan.

U.S. gold investment demand also rose very significantly:

“First half demand for gold retail investment products was 75% higher than 2015, boosted by the sharp price increase. Sales of gold coins by the US Mint went through the roof. The number of 1oz Eagle coins sold in the first six months of 2015 more than doubled – to 405,000 from 198,500 in 2015 – and these coins were far more popular than smaller denomination (half- and quarter-oz) coins. Trade data also showed a huge influx in imports of gold coins from other countries.”

The World Gold Council said that geopolitical risks including the U.S. election, “the slowing pace of U.S. interest rate hikes” and ultra loose monetary policies led to a perfect storm for gold and gold investment:

“A ‘perfect storm’ of conditions in the gold market this year has pushed investment to historic levels. Demand of 448.4t was a near-record for second quarter investment, only lower than Q2 2010’s stellar 606t. Consequently, demand for bars, coins and ETFs during the six months to end-June reached a first half record of 1,063.9t, worth a value of US$41.6bn.”

Key findings regarding global gold demand in Q2 and H1 are

- Overall demand for Q2 2016 increased by 15% to 1,050t, up from 910t in Q2 2015.

- Global investment demand was 448t, up 141% from 186t in the same period last year.

- Total consumer demand was 656t down 9% compared to 723t in Q2 2015.

- Global jewellery demand fell 14% to 444t versus 514t in the second quarter of 2015.

- Central bank demand fell 40% to 77t in Q2 2016, compared to 127t in the same period last year.

- Demand in the technology sector fell 3% to 81t in Q2 2016.

- Total supply was up 10% to 1,145t in Q2 2016, from 1,042t in Q2 2015. Mine production in Q2 2016 was virtually flat year-on-year at 787t.

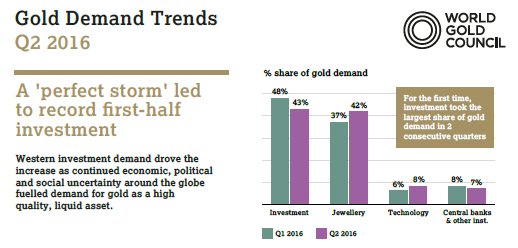

Importantly, for the first time ever something that we have flagged as likely to happen has taken place – for the first time, “investment has been the largest

component of gold demand for two consecutive quarters. And this has been in no small part due to demand from Western investors across the spectrum, from retail to institutional and for bars, coins and ETFs.”

The report is a leading industry resource for data on global gold demand. The quarterly publication examines demand trends by sector as well as geography.

It always gives good insights into the gold market and can be accessed here