Why is bitcoin considered such a big deal? Why has it grabbed so much mind-share, and why is it skyrocketing? And why is the cryptocurrency sector going bonkers?

The short answer is that cryptocurrency is the first major innovation in money in 300+ years, back when central banks first emerged in the late 1600s as centralized clearing houses for international payments and sole issuers of national bank notes/currency.

(Those who trace central banking to the Bank of Amsterdam’s founding in 1609 might say it’s the first major innovation in 400 years.)

Why is it an innovation? There are four basic reasons:

1. It’s a form of private-sector issued money. It is not issued or controlled by any government or central bank.

2. It is structured in a completely different manner than conventional central-bank issued currency: it is a digital form of money that is issued as payment for those who maintain the database (the blockchain) on their privately owned computers. Since the blockchain is distributed over numerous computers, it is decentralized and distributed rather than centralized.

3. It enables trusted transactions between parties without requiring the services of an intermediary, i.e.a bank which acts as a trusted clearing house for transactions.

4. In the case of the first cryptocurrency, bitcoin, its issuance of tokens (coins) is limited by its design to 21 million coins. No central authority can issue more bitcoins, nor does the structure of the bitcoin blockchain allow for further issuance.

To grasp the significance of these four characteristics, we have to go back to the early history of modern capitalism. My longstanding recommendation is to start with Fernand Braudel’s 3-volume history, Civilization and Capitalism, 15th-18th Century:

The Structures of Everyday Life (Volume 1)

The Wheels of Commerce (Volume 2)

The Perspective of the World (Volume 3)

Many of the functional pieces of modern capitalism were private-sector innovations, starting with banking and credit (some of which was borrowed from Arab traders). In the good old days of the 1500s, if the King of Spain wanted to finance a costly voyage around the world (Magellan’s circumnavigation in 1519-1522), he turned to private-sector lenders.

Insurance, stock markets, futures markets and options were all private-sector innovations designed spread the risk and reward of ventures such as trading voyages to the Spice Islands.

Since so many ships were lost at sea, backers sought insurance for the losses, and the trade in shares of the ship’s cargo and the insurance against its loss enabled a lively trade in these financial instruments that were the rough equivalent of modern-day options.

When a merchant vessel was seriously overdue, the value of the shares of its cargo plummeted as investors gave up hope of earning their hoped-for return. So some enterprising traders paid watchers to scan the shoreline for incoming ships matching the description of the overdue ships.

Should the overdue ship appear off the coast of France, runners would hurry to Amsterdam to inform the trader who would then promptly scoop up cheap shares of the cargo, scoring huge profits when the ship docked a few days later, cargo intact.

The rate of expansion of private-sector innovations is much higher than those of centralized authority. Centralized authority must act deliberately, and in consultation with all the various power centers of the society and economy. Disagreements can incapacitate the system for years or even decades.

The private sector, in contrast, is a free-for-all of a multitude of players with an enormous range of ideas, schemes, scams, risk appetites, insider knowledge (i.e. asymmetric knowledge), capital, expertise and so on, all networked through a fast-expanding spectrum of media and exchanges.

This private-sector ferment is on display in the cryptocurrency space. Scams and brilliant innovations are shoulder to shoulder in a fast-moving mob. No wonder so many players and traders want to join the mob and figure out some competitive advantage or gain some asymmetric knowledge, knowledge which can be as simple as the understanding that hard forks aren’t bad for bitcoin, as so many feared, as each new iteration claims to improve some aspect of bitcoin’s functionality.

Over 100 hedge funds and other institutional players are muscling into the market, anxious to scale in and scale up before competitors grab market share.

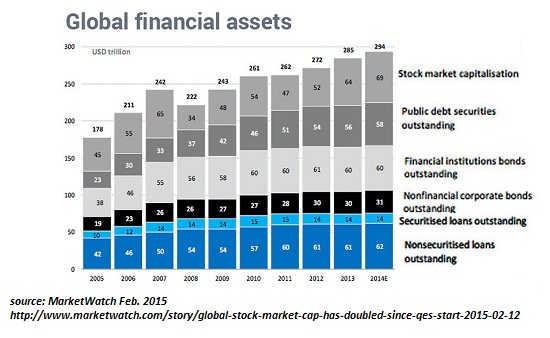

If we compare the market cap of all cryptocurrencies, currently $178 billion, with the total financial assets of the global economy ($300+ trillion) and real estate ($200+ trillion), we get a sense of “early days.” Bitcoin’s market cap of $100 billion wouldn’t even show up as a thin line on this chart of global financial assets:

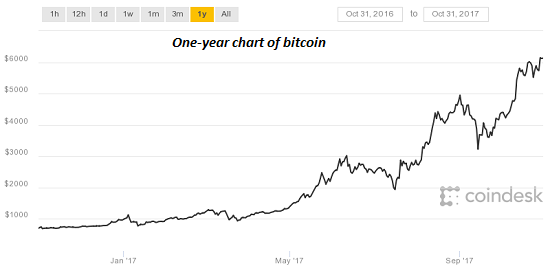

Here is a one-year chart of bitcoin:

As Marx presciently noted, capitalism melts all that is solid into air. (All that is solid melts into air.) Centralized banking and all other forms of intermediary rentier skims are presented as solid. If history is any guide, these supposedly solid entities may well melt into air.

Of related interest:

My labor-backed cryptocurrency community economy: A Radically Beneficial World: Automation, Technology & Creating Jobs for All

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.