Below I’ve collected links to some of my favorite white papers and presentations on volatility. I’ve organized them in the following categories:

- Volatility Concepts & Volatility Trading

- Probability Distributions—Normal and Otherwise

- The VIX and VIX Futures

- Volatility Contagion—Will Short Volatility Destroy the World?

- Variance Swaps—the Technology That Underlies VIX & VIX Futures

For an index of my 60+ posts on volatility see here.

Volatility Concepts & Volatility Trading

- “Volatility: A New Return Driver?” by Greggory Flinn & Roger Schreiner

- A good non-mathematical overview of volatility, volatility products including futures and a couple example trading strategies using volatility Exchange Traded Products

-

Easy Volatility Investing by Tony Cooper

- Available via free download on the SSRN repository, this paper provides a good non-mathematical overview of volatility investing. It includes a good discussion on the Volatility Risk Premium (VRP) which is an important concept. It also provides detailed analysis of several volatility based trading schemes

Probability Distributions—Normal and Otherwise

-

Tales of the Unexpected by Andrew Haldane

- This accessible paper (only one equation) is the best that I’ve ever read on the differences between processes accurately modeled by Gaussian/normal distributions and those better matched by power law distributions. I have seen this distinction made many times, but this paper provided examples and reasoning that really helped me internalize the differences. Most of our stock market computations (including Black & Scholes for option pricing) and risk management formulas assume normal (or log-normal) distributions but this paper lays out a compelling case for why power law distributions are often a better match.

-

The normal distribution is the log-normal distribution by Werner Stahel & Eckhard Limpert

- This presentation does a very nice job of distinguishing between the normal and log-normal distribution and providing guidelines for when they should be used. Bottom line, for stock price distributions we should use the log-normal distribution.

The VIX® and VIX Futures

-

Understanding VIX Futures and Options by Dennis Dzekounoff

- This article contains an excellent, non-mathematical overview of the peculiarities of VIX options including their Greeks and term structure. Most broker’s Greeks for VIX options are completely wrong to start with, but Dennis points out some other issues like steep call skew, dangerous calendars, and slower than expected theta decay.

-

VIX White Paper provided by the Cboe

- Complete details on the VIX calculation, recently updated (August-2018) to reflect the new methodology that reduces the chances that bad quotes on the SPX options will glitch the VIX.

- “The VIX-VIX Futures Puzzle?” by Ivan Oscar Asensio

- A paper testing the forecast accuracy of VIX futures that starts with a good non-mathematical overview before diving into a comprehensive technical overview of the VIX, VIX Futures, and volatility term structures. It skips the calculus but provides a clear description and comprehensive formulas.

-

VIX Settlement Process by Dominic Salvino & William Speth

- This presentation, included in a session from the Cboe’s 2014 European Risk Management Conference, provides a very good overview and some detailed examples of how the Cboe handles the controversial expiration process for VIX options and futures

-

A Tale of Two Indexes by Peter Carr and Liuren Wu

- This paper briefly goes over the Cboe’s first try at a volatility index, now called the VXO but most of the paper is a mathematical tour de force taking us through the equations underlying the VIX, VIX Futures, and VIX options

Volatility Contagion—Will Short Volatility Destroy the World?

I’ve listed three sources below with varied views on the odds of a volatility spike causing wide-spread damage to the world’s financial assets.

-

Is Short Volatility a “Crowded Trade” by William Valentine

- This paper reviews the common arguments regarding the risks of short volatility. I particularly liked the discussion on the widely mis-interpreted Commitments of Traders report from the CFTC that tallies long and short positions in VIX Futures.

-

Everybody’s Doing It: Short Volatility and Shadow Financial Insurers by Vineer Bhansali and Lawrence Harris

- This paper, published February 16, 2018 narrowly missed “I told you so” honors for foreshadowing the record February 5, 2018 volatility spike and the mauling of the short volatility Exchange Traded Products: XIV, SVXY, and VMIN.

-

Volatility and the Allegory of the Prisoner’s Dilemma: False Peace, Moral Hazard, and Shadow Convexity by Christopher Cole

- This link takes you to a list of interesting and entertaining white papers provided by Artemis Capital Management (including the title above) on the risks associated with short volatility positions.

Variance Swaps—the Technology That Underlies the VIX

-

Just What You Need to Know about Variance Swaps by Sebastien Bossu, Eva Strasser, and Regis Guichard (JPMorgan)

- This technical paper includes a very good discussion and accompanying graphs regarding the “Static Replication of Variance Swap”—which happens to be underlying mechanism of the Cboe’s VIX. Technically the VIX is a variance swap priced in volatility points.

- “Variance and Convexity: A Practitioner’s Approach ”

- My favorite paper from the CBOE’s 2013 Risk Management Conference. Sparse and very technical it addresses some of the differences between variance and volatility with regards to VIX futures.

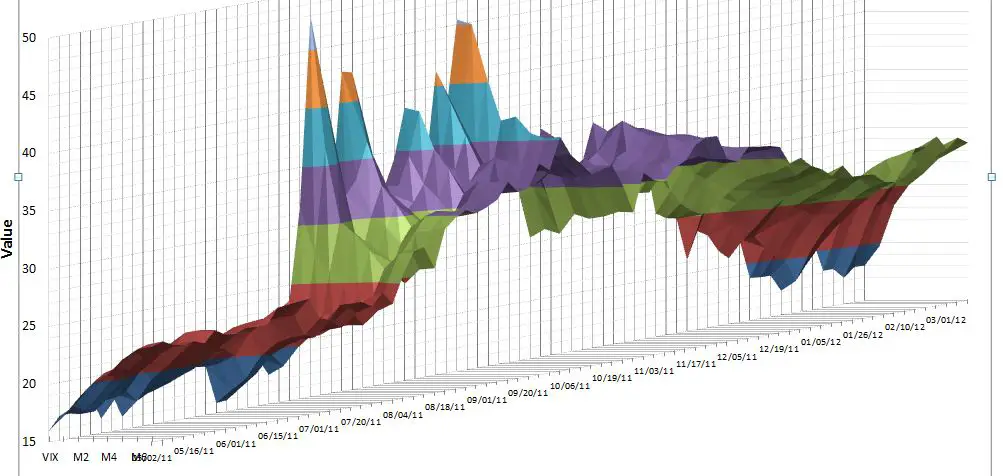

VIX + VIX Future Term Structure May 2011 – March 2012