|

Proprietary Data Insights Retail Top Communication Equipment Stock Searches This Month

|

What we’re watching

|

|

A look at a computing company that represents incredible value… HP Enterprises.

|

|

Stock Analysis |

The computing giant that’s super cheap |

Companies that don’t change are destined for failure. In 2015, Hewlett Packard split into two entities. We aren’t interested in the PC-focused business. Instead, we think the HP Enterprise (HPE) side is an incredible value. Most investors ignore this stock because…well the company hasn’t done well over the last several years. In fact, it only got the 10th most searches by retail investors amongst communication equipment stocks according to our proprietary data. But we think that’s about to change. And the growth prospects are pretty exciting, especially when you consider shares trade at 7.46x Non-GAAP forward earnings and 4.71x forward cash flows. So what exactly will this future company look like? HPE’s Business Hewlett Packard Enterprise focuses on enterprise-facing hardware and services. Revenues breakout as follows:

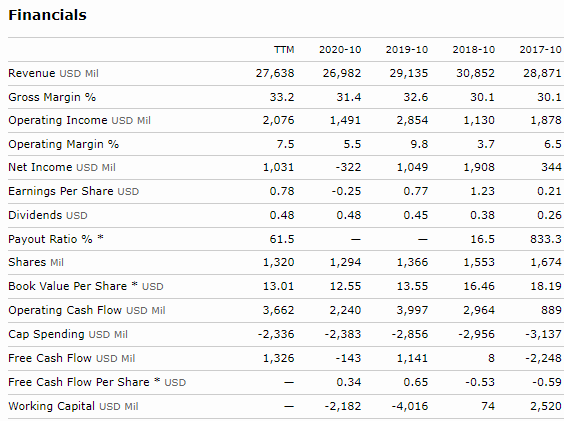

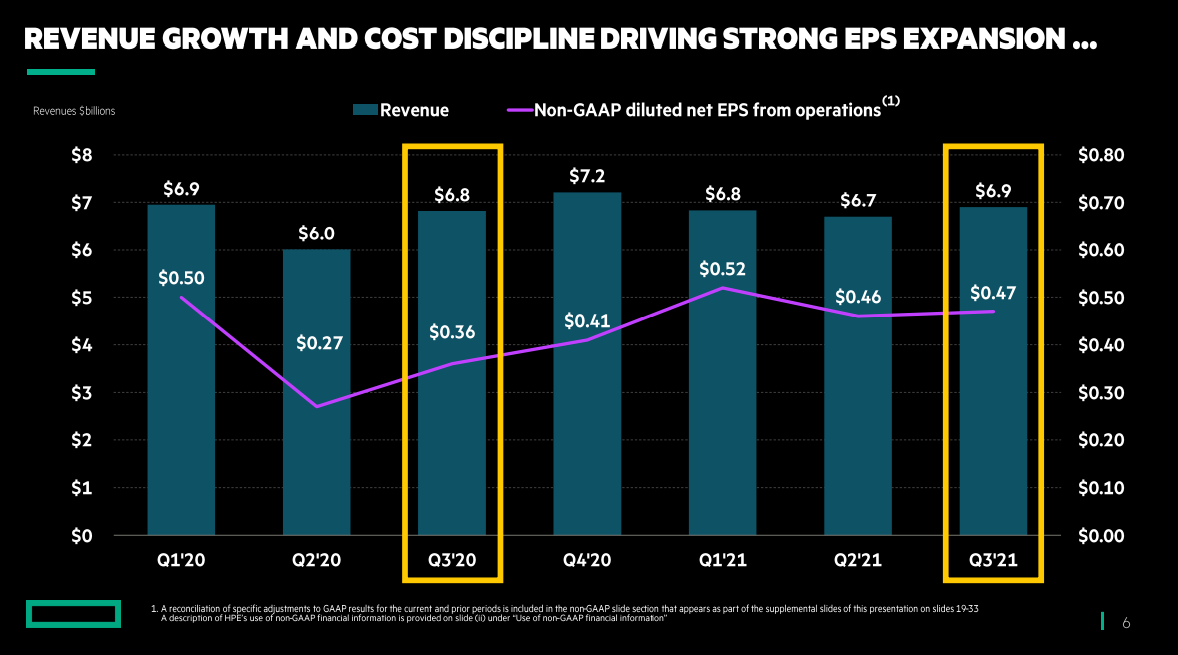

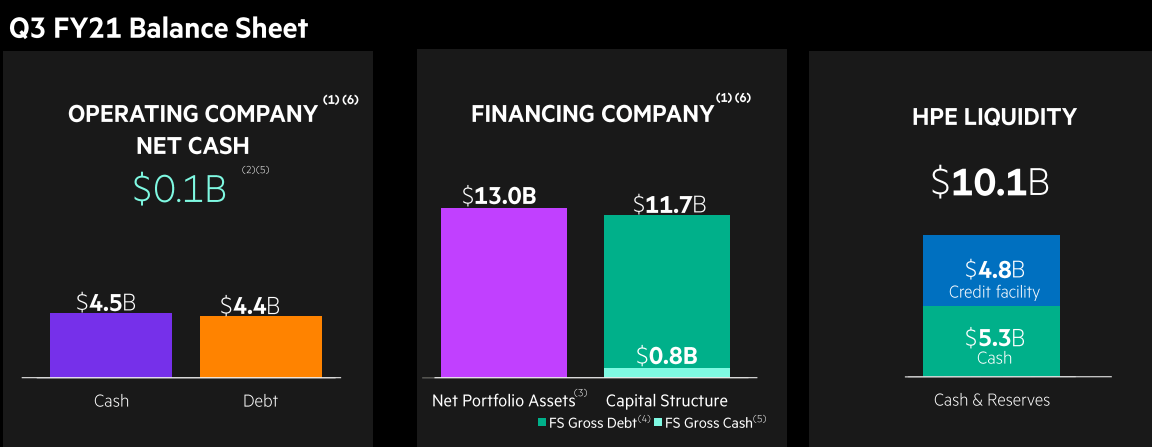

Since the spinoff, HPE remains focused on restructuring and realigning its business to deliver sustainable long-term growth. Translation – mergers and acquisitions while shedding non-core assets. In 2021, HPE acquired Ampool, Zerto, Determined AI and Cloud Physics to create capabilities and add products to the fast-growing cloud space. This comes after prior pickups of Silver Peak, Cray and MapR, as well as five other businesses acquired in 2018. All these units aim to push HPE more towards the higher-margin hybrid IT model such as enterprise-class server and storage markets. Lastly, HPE sees AI and the industrial internet of things as its next major markets. Consequently, the company committed $4 Billion in investments to enhance capabilities across its network. HPE Financials The most relevant period to look at for HPE is after the spinoff. While revenues declined from 2018 to 2020 they’ve turned around as the economy reopens. Margins also expanded nicely to record levels, helping drive some spectacular earnings results. Normally, we would be bit concerned at the $12.5 Billion in long-term debt as well as the $7 Billion in contract liabilities held under ‘other non-current liabilities.’ However, the majority of the debt is held at the finance company and is non-recourse to HPE. That means it’s actually their customers’ debt and HPE collects fees and interest on it. Plus, HPE has access to plenty of cash and credit to continue its transformation.

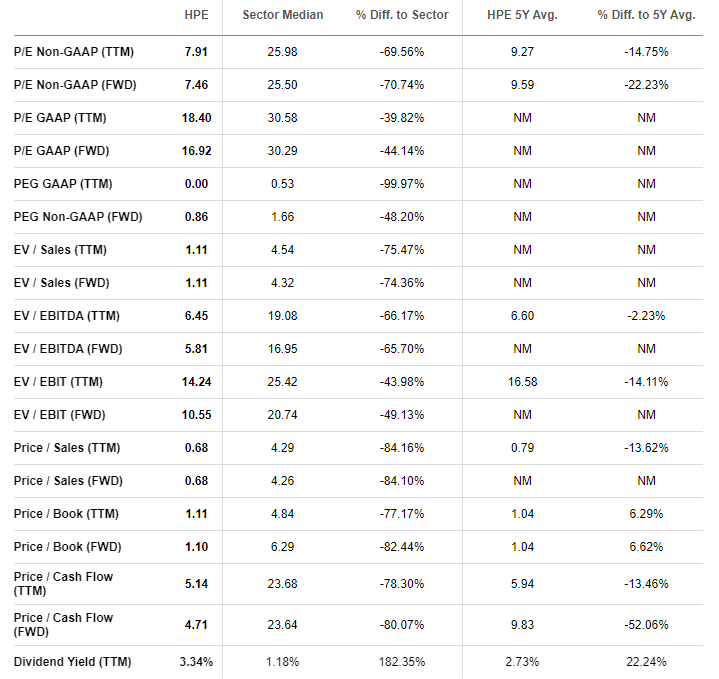

Valuation When we said the company was cheap, we weren’t lying. HPE smokes every comparison to the rest of the IT sector. And check out that juicy 3.34% dividend yield, which isn’t common in the sector. To be fair, analysts don’t expect much growth from the company over the next year or so as it continues its transformation. However, you can’t ignore these prices. Our Opinion – 9/10 This is what we’d call a deep value play. We expect the company to continue to sell or spin-off lower-margin business units while acquiring and investing in higher-margin growth segments like cloud computing. With a 3.34% dividend, shareholders can reinvest the dividend to help lower their average cost per share. Ideally, we like the stock at $13-$15 per share. |