|

Proprietary Data Insights Retail Top Grocery Stock Searches This Month

|

What we’re watching

|

|

A look at a grocery chain with great growth rates, Sprouts Farmers Market.

|

|

Stock Analysis |

Sprouts is seriously undervalued |

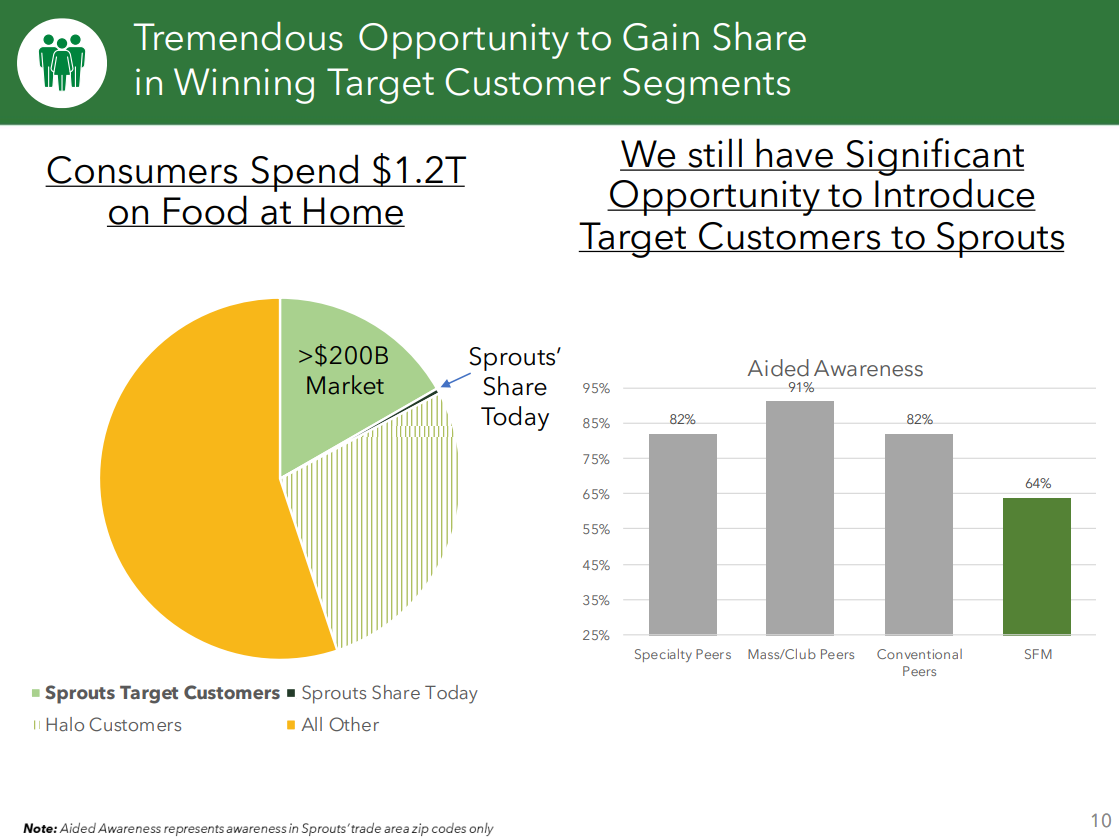

Grocery is a tough business. It relies on high volume and low margins. Growth comes mainly from acquisitions and population increases. That’s why Sprouts Farmers Market (SFM) is so unique. It’s a grocery chain that averaged 12.5% revenue growth over the last five years. Yet, it’s priced as if people believe it will only grow in the single digits. Which means there is a ton of upside here. In fact, Sprouts was the #2 grocery stock searched by retail investors this month. Heck, in the last three weeks, shares have shot up more than 25%. And while we wouldn’t mind a pullback, we think there’s a good case to be made for the equity right here and now. Sprouts’ Business Based out of Phoenix, Arizona, Sprouts Farmers Market operates a fragmented grocery store chain. Their main draw – fresh produce, foods, and a vitamin department. To meet the changing needs of customers, Sprouts has expanded into more health and wellness products including plant-based, gluten-free, keto-friendly, and grass-fed foods. Additionally, the company has focused on natural and organic foods, one of the fastest-growing segments in the industry. With 366 stores across 23 states, the company segments its business as follows:

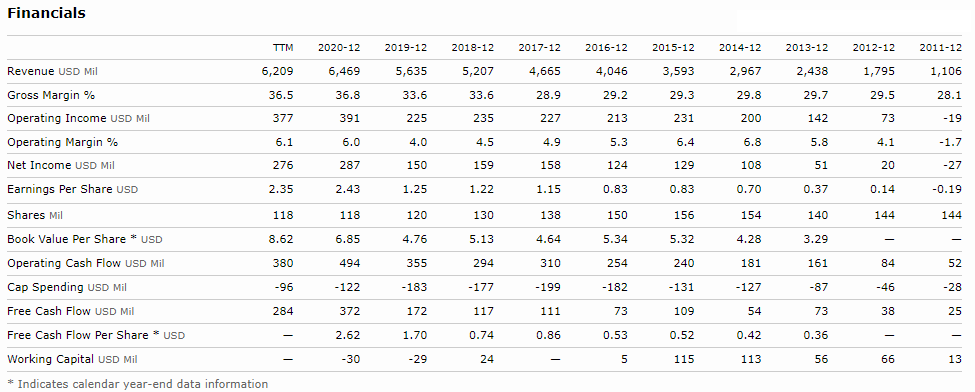

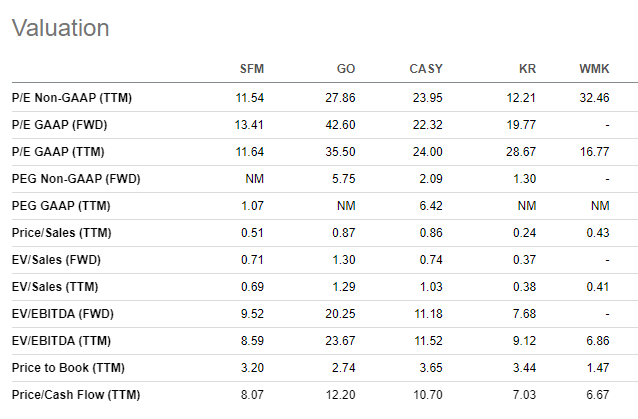

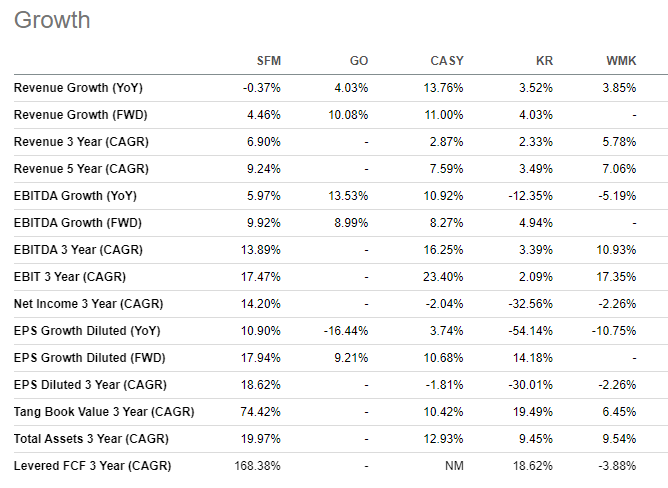

Management is targeting +10% annual growth beyond 2022. It’s worth noting that the company’s private label program accounted for 16% of 2020 revenues and features ~3,500 products. KeHE Distributors is the main supplier of dry grocery and frozen food products to Sprouts. They accounted for 42% of the total purchases in 2020. As the company looks into the future, they continue to target Gen-Z customers with strong ESG values and improve their digital marketing. In the graphic below from the company’s quarterly presentation, Sprouts sees a massive opportunity for growth. Lastly, we want to highlight two key growth drivers for the company. E-commerce is a major growth market pretty much everywhere. Yet, Sprouts only has around 10%-12% penetration with its customers, something they could vastly improve upon. Second is the update to their supply chains. Sprouts wants to create meaningful partnerships with farmers and increase local buying. Financials One of the things we love about Sprouts is the continuously improving sales and margins. Over the last decade, gross margins increased from 28.1% to 36.5% while operating margins went from 4.1% to 6.1%. To give you an idea, Kroger (KR), one of the largest grocery chains in the US, runs a 22.5% gross and 1.7% operating margin. And Kroger’s annual growth rate averaged less than 4% over the last 5-years. That said, in their most recent earnings call, Sprouts’ management mentioned inflation 17 times. Bank of America analysts put out a note saying they believed the grocer would lose traffic due to inflation. It is likely that in the near-term Sprouts’ margins will come under pressure as food and labor costs rise. Valuation The best way to evaluate Sprouts is with a comparison to its peers. When we look at the basic valuation metrics, we find that Sprouts, even after a 25% run, is still cheaper on nearly every metric. The only ones where it falls a bit short are the EV/EBITDA and price to cash flow. However, we think the growth numbers Sprouts puts up relative to its peers more than makes up for that. No, the year-over-year growth numbers aren’t great. But the compounded growth numbers over the last 3-5 years look better than their peers. Plus, it’s the only one of the companies listed here that shows growth in EVERY category. Our Opinion – 9/10 We love the strategy and focus of Sprouts. And given the growth and low valuation, even after a 25% run, we think it’s a steal. |