|

Proprietary Data Insights Retail Top Stock Searches in November

|

What we’re watching

|

|

Tesla routinely tops searches for both retail and institutional investors according to our proprietary data, so what is it really worth?

|

|

Stock Analysis |

What is Tesla actually worth? |

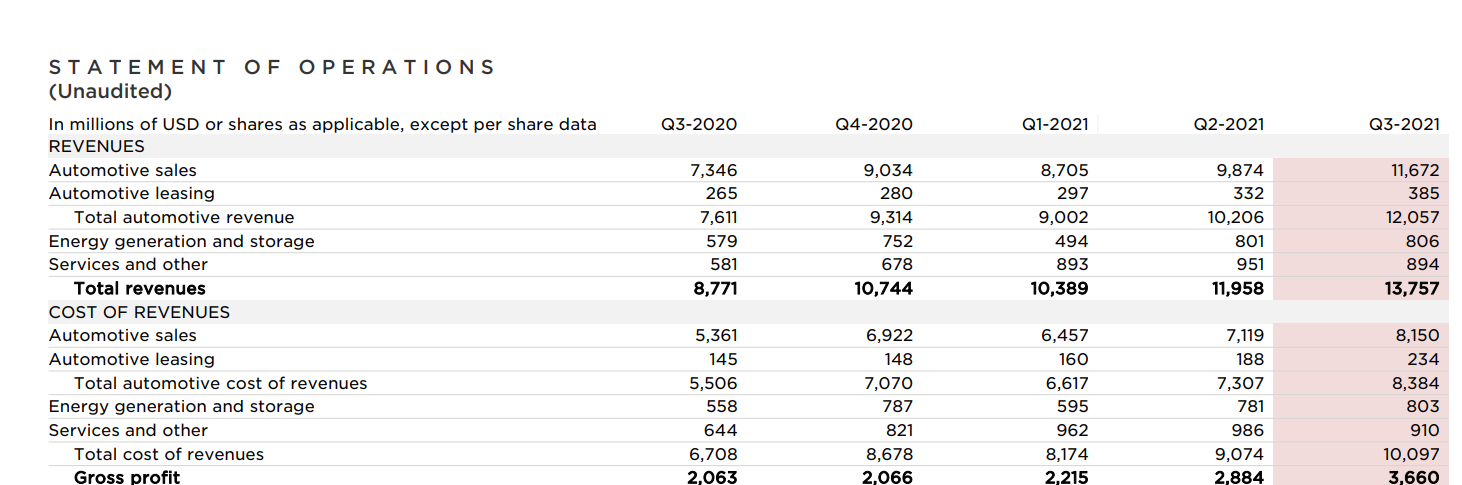

At $1.135 Trillion, Tesla is the 6th largest company by market capitalization in the world. That might seem ridiculous for some. For others, including famed investor Cathie Woods, it’s still cheap. Every week for the last month, Tesla topped the search results across every category for both retail and institutional investors according to our proprietary database. So, we wanted to determine what Tesla was actually worth. Elon Musk took his vision from paper to reality. Just a few short years ago he wasn’t sure the company would survive. In the last 12 months, the company generated nearly $10 Billion in operational cash or around $8.80 per share. That might not seem like much, but considering Tesla generated ~$6 Billion in 2020 and $2.4 Billion in 2019, it’s some stunning growth. We won’t sit here and tell you that shares of Tesla are cheap. They’re not. But we can tell you where we would like to pick them up and why. Tesla’s Business In A Nutshell We all know Tesla makes electric vehicles. If you didn’t, then shame on you! What you may not know is the company also has a sizable energy generation and storage business. This includes the design, manufacturing, installing, sales, and leasing of solar generation and energy-related products for residential, commercial, and industrial customers.

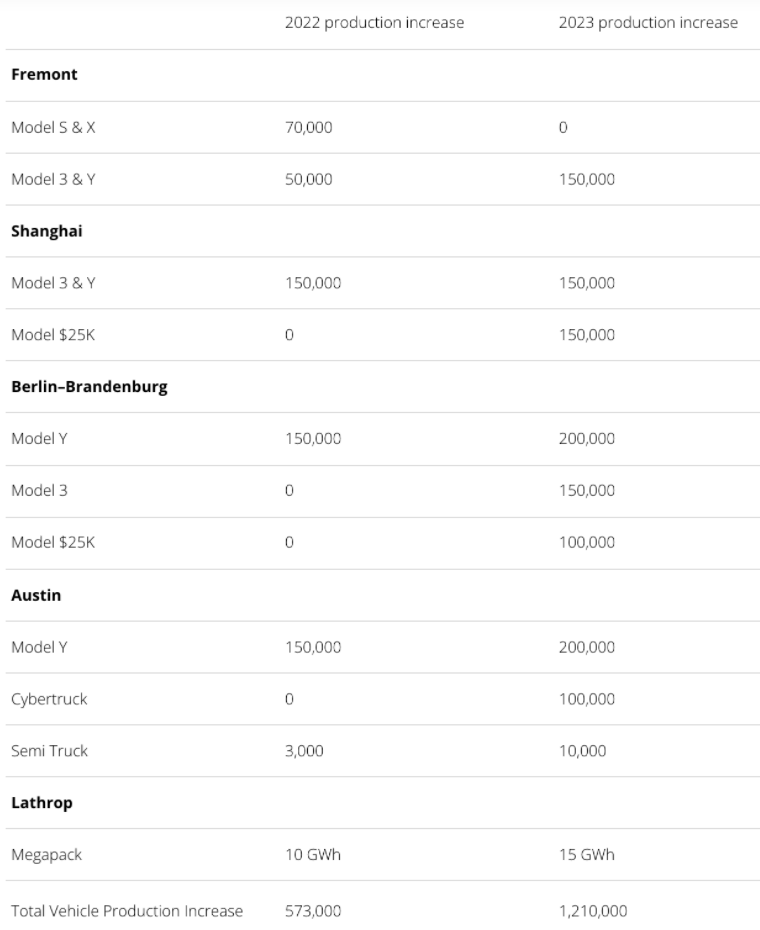

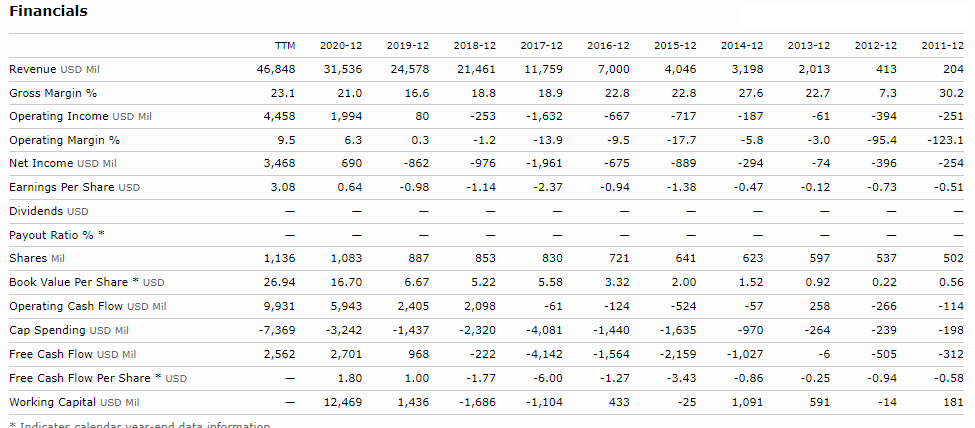

Some quick math shows that Tesla’s managed to improve its gross margins over the last year. For example, auto sales increased from 27% to 30% while overall gross margins improved from 23.5% to 26.6%. Beyond the glamor of investing in Tesla, the company exhibits and expects remarkable growth. Right now, Tesla plans to hit long-term annual growth of 50% per year! So far, Elon has been on it. Right now, Tesla manufacturers in Freemont, California as well as Shanghai, China, with production plants opening in Austin, Texas, Berlin, Germany. Tesla Energy plans to build a Megafactory in Lathrop, California to supplement its current production in the Nevada and New York facilities. So, yeah, Tesla can hit the growth it’s projecting. Its expansion into consumer and commercial trucks also lends itself to massive growth. Unlike many of its competitors, Tesla managed to get around semiconductor shortages by leveraging its programming expertise to incorporate processors it could get its hands on. Lastly, we want to touch on what we call ‘moonshots.’ Tesla has yet to deliver a fully autonomous vehicle. If it can, that changes everything. Why? Because consumers no longer need to own cars (or garages for that matter). Tesla would simply build a ton of autonomous vehicles that could be called on like an Uber. Imagine a ride to work for $5-$10 where you could work the entire time. More important, consider how that would impact commercial deliveries for trucks. Hours of service and labor constraints would disappear. We’re not there yet. Nor are we very close. But it’s definitely possible in our lifetime. Financials It’s pretty cool to look at Tesla’s financials below and see the growth over the last decade. Going from $204 Million in sales to $46.8 Billion is just incredible. Now, we want to highlight the higher capital spending as Tesla expands its network. Nonetheless, free cash flow, the cash after capital expenditures, still lands at a hefty $2.5 Billion. What you might be surprised to learn is that Tesla has a solid balance sheet. Long-term debt dropped by almost half in the last year. Plus, the company carries $16 Billion in cash. That puts it in a fantastic position to deploy capital if and where it needs to. Valuation We won’t bother trying to use valuation models because the stock is stupid expensive compared to earnings right now. Instead, we want to do a little discounted cash flow analysis to just get a sense of what shares might be worth. A discounted cash flow looks at the future cash generated by the company and then discounts it at some interest rate to see what all that cash is worth today. We took some liberties with the calculations to give you a sensitivity analysis. Yes, these models can produce very wide range of prices. The point isn’t so much to get the exact value. It’s to understand how different inputs influence the outputs. For example, we assumed a lofty 50% growth rate every year for a decade in the first two scenarios and a 30% average in the second two. Is it likely Tesla hits 50% for a decade? Probably not since that would mean the company would generate almost $2.7 Trillion in sales. Could they do it for 5 years? Probably. If you made the adjustment from 50% to 20% growth in Year 6, you get a price range per share of $537 – $774. The point is that at a current +$1100 price, you need a lot to go right to get more upside from here. Our Opinion – 6/10 We like Tesla near $800. That’s where we would start to get interested. $600 would be ideal There’s no doubt this is a great company with a bright future over the next several years. We just aren’t willing to overpay for the ‘moonshots’ right now. |