What we’re watching

|

|

A look at interior design and home furnishing store Ethan Allen.

|

|

Stock Analysis |

Ethan Allen’s Massive Dividend & Value |

Furniture is hard to come by. Try ordering a bed frame and you’re likely to wait six months or more. That puts pricing power in the hands of sellers. We think this is a multi-year trend that lasts into 2025. Interior design and home furnishing store Ethan Allen (ETD) saw earnings nearly triple from their 2019 levels. Plus the stock pays a healthy 4.26% dividend. Now, the home furnishings industry isn’t well known for its fundamental value. So, this is a stock pick with some timeliness to it. And here’s why. Ethan Allen Interior’s Business Ethan Allen Interiors manufactures and sales interior design products that cater to the home furnishings market. The company operates 302 design centers across the US and worldwide of which 161 are independently owned and 141 are company operated. Revenues are broken down into two categories:

Like many retailers, Ethan Allen has increased its online presence with applications like their 3D Room Planner that allows designers to conduct virtual design sessions without entering the customer’s home. Client’s can also use a lighter version of the 3D Room Planner to design a solace personalized to their own room’s dimensions and features. Additionally, digital channels are now the primary way of communicating with customers. 75% of Ethan Allen’s products are manufactured in American workshops, limiting their exposure to the supply chain problems that plague many of their competitors. Currently, the company offers three strategic merchandising projections:

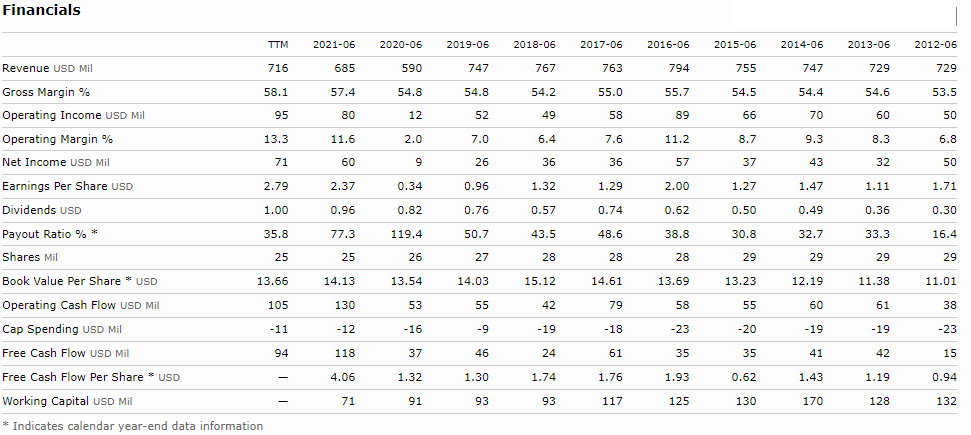

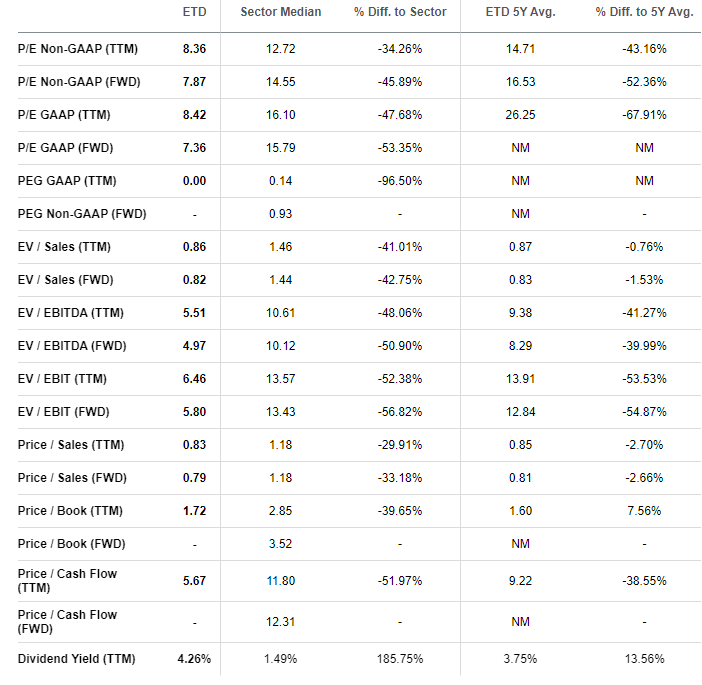

However, Ethan Allen is especially adept at customization, giving customers greater flexibility in design and choice. Financials In the last decade, Ethan Allen’s financials were nothing to write home about. While they paid a consistent dividend that grew over time, margins remained relatively flat as did sales. It wasn’t until recently the company saw revenues shoot up along with gross margin and operating income. That led to the company’s best earnings year ever not to mention significant cash flows. Notably, Ethan Allen doesn’t spend much capital and maintains a fairly consistent operating cash flow. That’s helped the company keep its capital leases to a bit more than $100 million with zero long-term debt. However, the nearly $100 million in cash covers all capital leases. And with more than 300 million in property and equipment plus an average of $150 million in inventory, Ethan Allen’s balance sheet is strong enough to support their current dividend payouts. Valuation Despite improved financials, shares of Ethan Allen are only up 16.23% for the year. That’s put the stock at a pretty sweet valuation. Compared to the consumer discretionary sector, Ethan Allen’s stock is essentially running a 50% off sale. Normally, price-to-earnings ratios can be a bit misleading. However, with the low debt and consistent performance, we feel it accurately represents the company’s value. Given the robust balance sheet where assets outweigh liabilities, combined with a price-to-cash flow ratio of 5.67x, we believe shares are extremely undervalued. Our Opinion – 9/10 To be fair, management doesn’t seem to have any designs (pun intended) to generate additional growth through acquisitions or product expansion. Nevertheless, we look at the valuation and shareholder friendly dividend as creating more than enough reason to like the stock at current price. Given the current valuation and outlook, we see $30 per share as an easy target within the next year, leaving +30% upside. |