|

Proprietary Data Insights Financial Pros Top Telecom Searches in Nov.

|

What we’re watching

|

|

AT&T is too cheap following the company’s plans to spin off Time Warner in a combination with Discovery.

|

|

Stock Analysis |

AT&T Is Now Too Cheap |

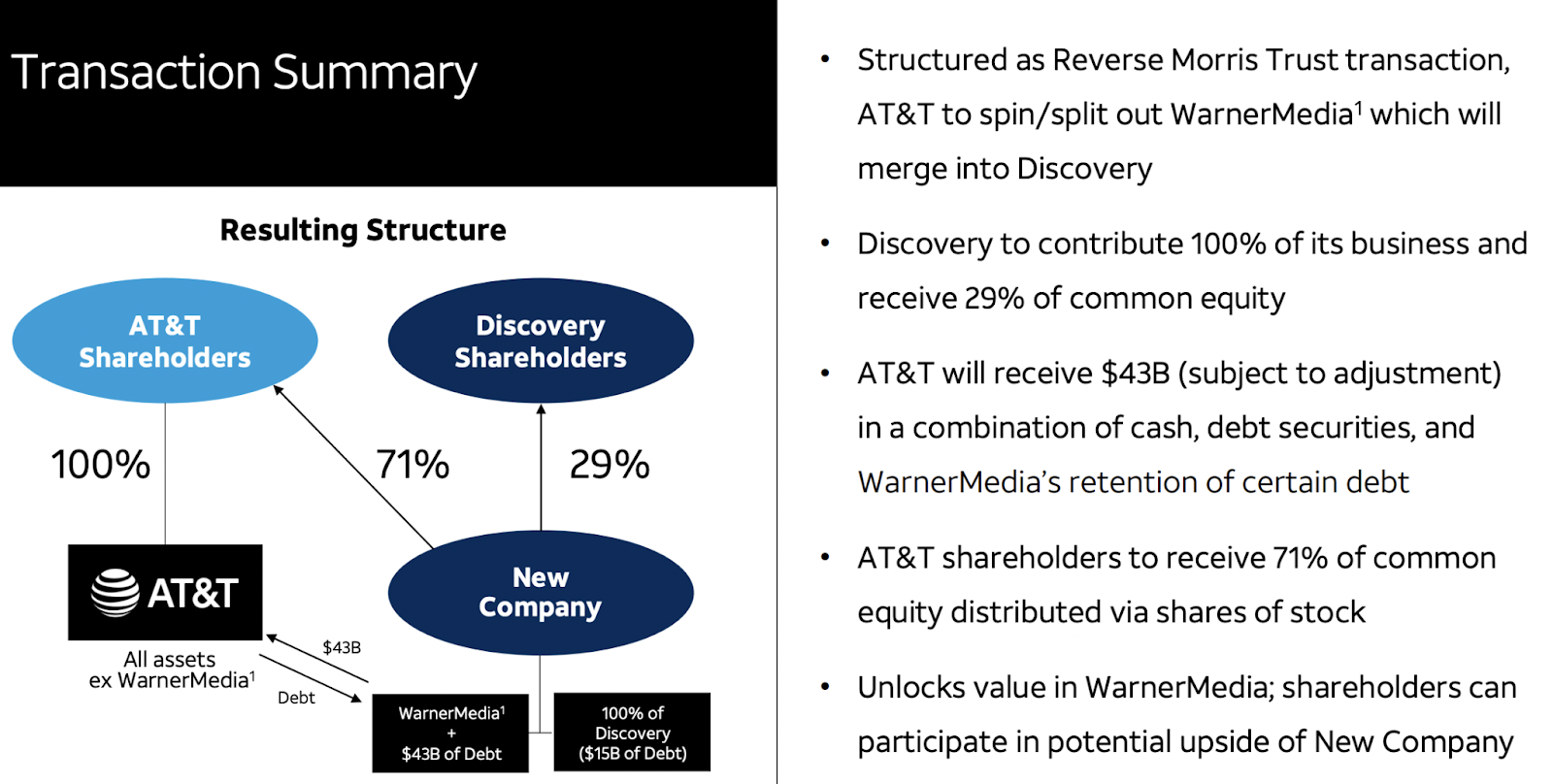

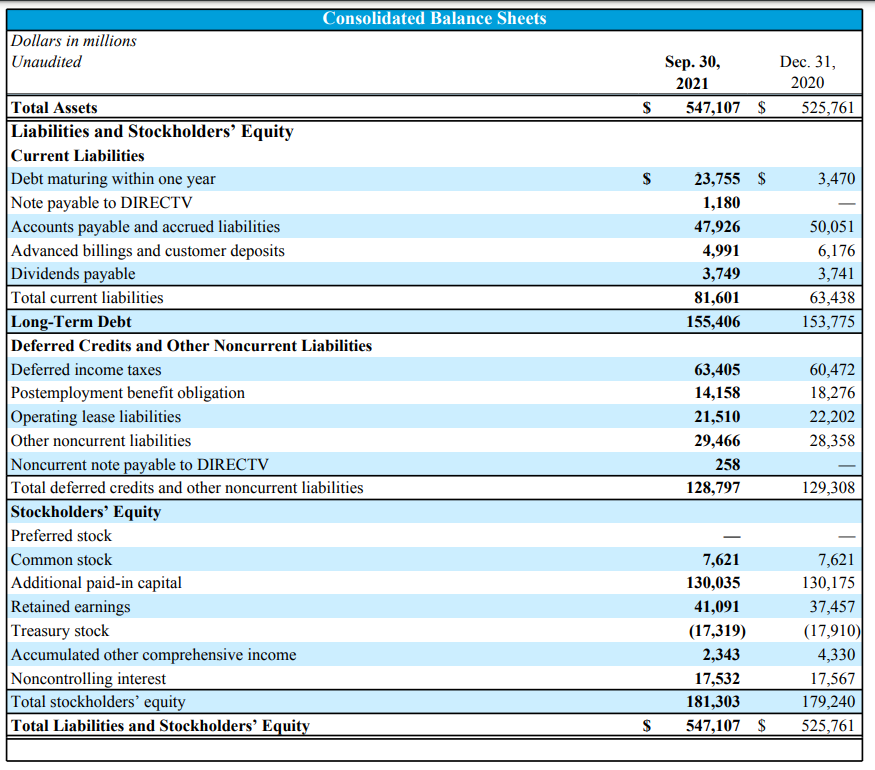

Investors were worried when AT&T (T) cut its dividend in May by a significant chunk. In a major shakeup, the company announced plans to spin off TimeWarner into a combination with Discovery (DISCA). The smaller AT&T aims to refocus on expanding its 5G network. With shares trading at lows not seen since the 2008 crash, we wondered if AT&T was a buy. As the top telecom services search by financial pros, we expect the stock to find a bottom soon. The question is where and at what price? Let’s start by looking at all the moving pieces to the AT&T Puzzle. AT&T’s Business We all know AT&T as a telecommunications provider of wireless and landline services. Their profitable landline business has been slowly shrinking over the years while the company accumulated more and more debt. Recently, AT&T decided it failed with its acquisition of Time Warner back in 2018. The new company would merge with Discovery Channel to become its own publicly traded company. Below is the slide from AT&T that explains the new structure. In a nutshell, AT&T will own 71% of the new company. The rest of AT&T will focus on investing aggressively into its fiber and 5G network. Wireline segments now include fiber and broadband as traditional telephone services have become negligible. Financials The biggest question for AT&T investors is what will the new company look like. We start by taking management’s statement that after the spinoff, AT&T will generate +$20 Billion in free cash flow. At that point the company expects to adjust its annual dividend to reflect 40%-43% of this new FCF. That means $8 Billion for dividends and $12 Billion left over. With 7.2 Billion shares outstanding, that means a dividend of ~$1.11. Right now that would come to a dividend yield of ~4.8%. Now, we need to figure out what the ownership in DISCA is worth. In 2022, AT&T shareholders will get shares of the new TimeWarner/Discovery company. At 71% ownership, we can take DISCA’s current market cap to calculate an additional $37 Billion in value to AT&T shareholders, which comes out to around $5 per share. That’s a ton of value in the next year all things considered. Now, bears point to one key problem for AT&T – debt. The company currently has a stupid amount to the tune of $155 Billion. Right now that’s only generating an interest expense of $6.68 Billion. But when rates rise, you can bet your bottom dollar that those costs will as well. For reference, here’s their current repayment schedule and interest rates: That said, the company expects to take Net Debt to Adjusted EBITDA to 2.6x after the transaction closes and 2.5x by the end of 2023, down from around 2.9x now. Some of that will come from single-digit revenue growth while the rest will come from paying down debt. Keep in mind, free cash flow comes after Capital Expenditures, the investments AT&T needs to make into 5G of $24 Billion per year. Valuation – As a quick note on valuation, the metrics won’t matter much as the company’s new structure won’t reflect prior earnings and margins. Our Opinion – 9/10 This might seem like an odd pick of us given all the moving parts. Yet, when you consider the likely dividend and ‘special dividend’ in the form of the new media company shares, we’re looking at a yield of around 6.6% at current prices. Afterward, investors are rewarded with a nice 4%-5% dividend yield, investment in 5G growth, and, finally, an ability for AT&T to pay down its debt. |