|

Proprietary Data Insights Financial Pros Top Stock Semiconductor Searches Last Two Weeks

|

What we’re watching

|

|

Intel has a lot of value and a path to growth but can it execute it?

|

|

Stock Analysis |

Is Intel A Value Trap? |

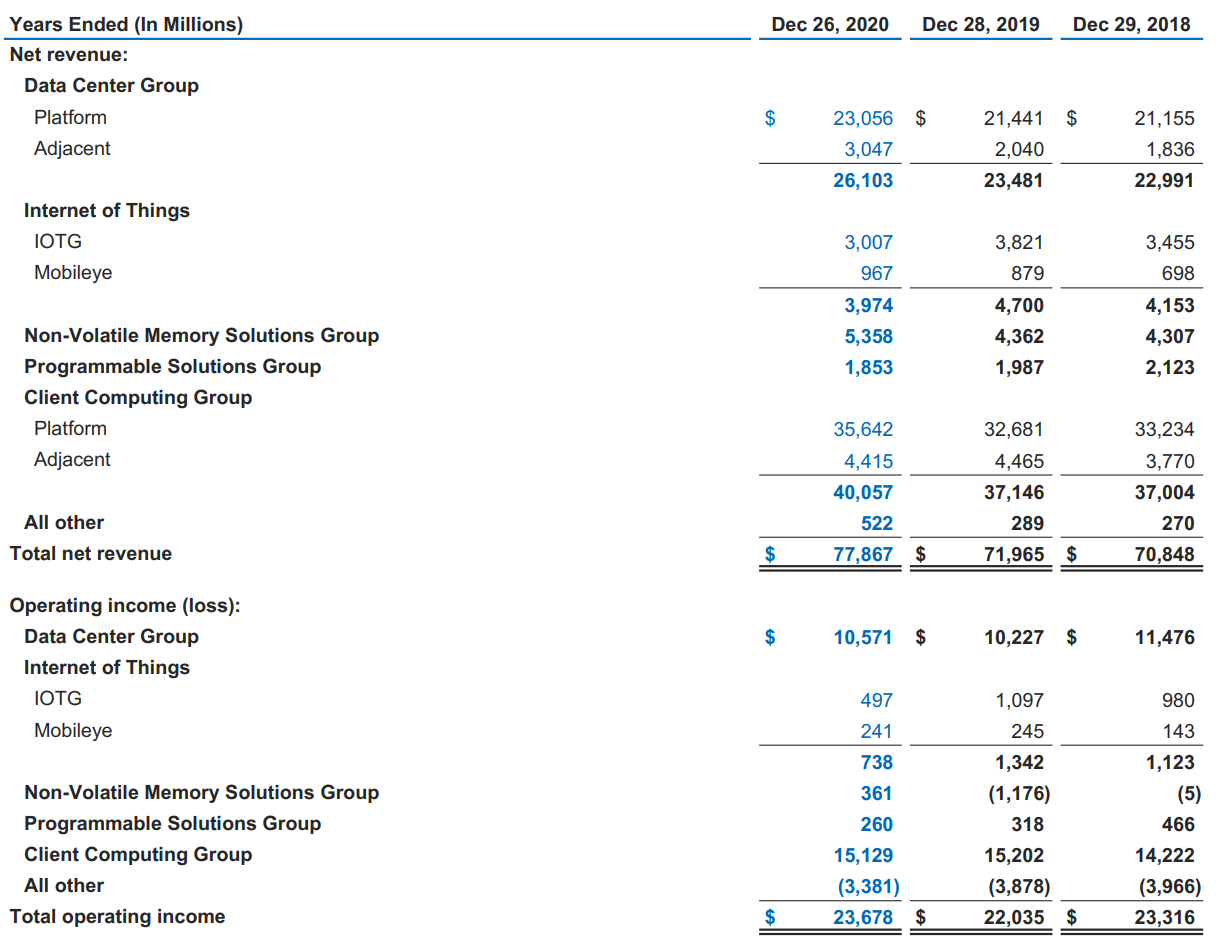

You would think that at less than 10x earnings, Intel (INTC) would be a steal. Yet, shares have languished between $45-$65 per share since they acquired Mobileye in 2017. Which makes the news of Intel’s decision to spin off Mobileye into its own publicly-traded company through an initial public offering (IPO). As the 3rd most searched semiconductor stock amongst financial pros in the last two weeks, we decided to take another look at the perpetual laggard. What we found was a stock with a lot of value and a reasonable pathway to growth. The question is can they execute. Intel’s Business As the world’s largest semiconductor company and supplier of microprocessors and chipsets, Intel has struggled to keep pace in the last several years. The company relied heavily on personal computers, missing the mobile growth story. Over the years, Intel’s vertically integrated business hamstrung the company as they lost focus on innovation, falling behind Advanced Micro Devices (AMD) who outsourced manufacturing. Last summer, Intel’s stock sold off as the company disclosed a delay in the production of its 7-nanometer scale processor, putting it further behind Taiwan Semiconductor Manufacturing (TSM) which already mass produces chips at a 5-nanometer scale. On March 23, the company announced plans to spend $20 Billion to build two new semiconductor fabrication facilities in Arizona, giving them more production capacity in a tight supply market. Intel’s business breaks down into

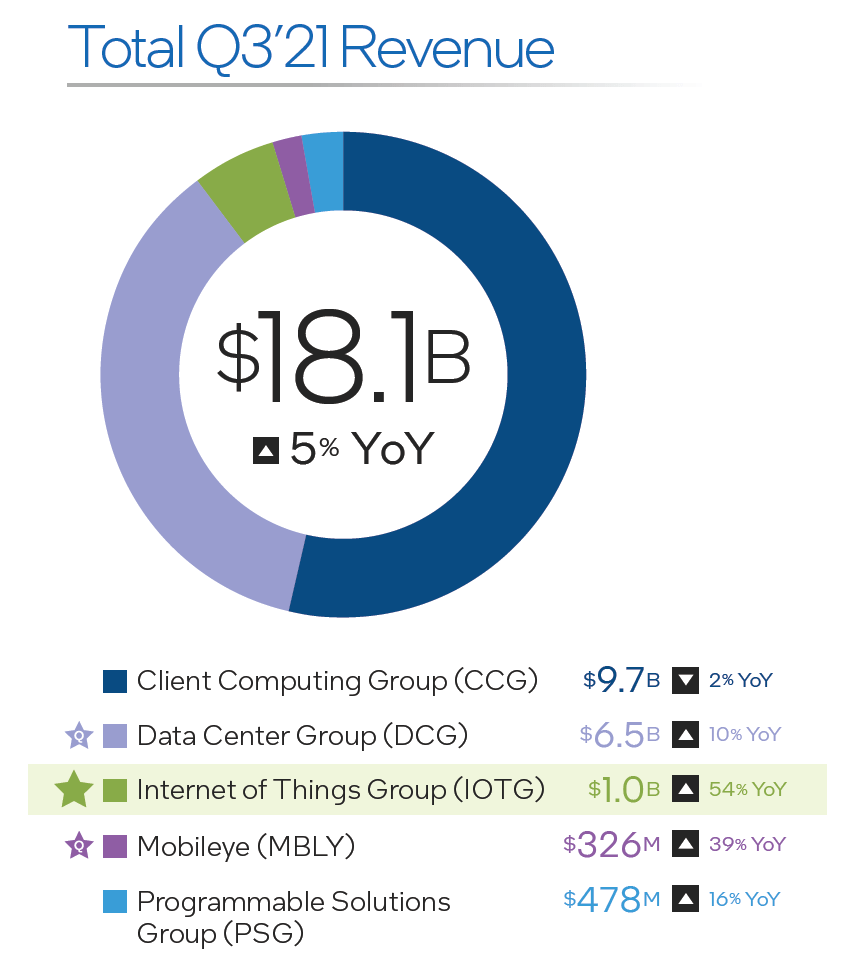

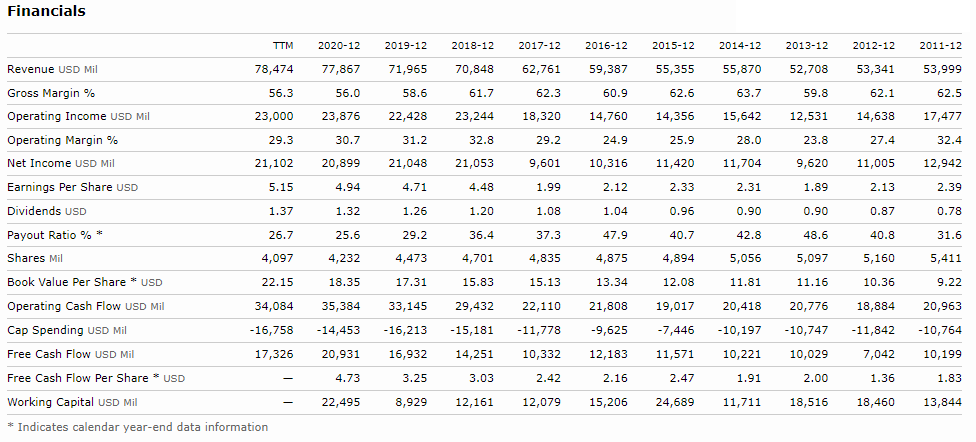

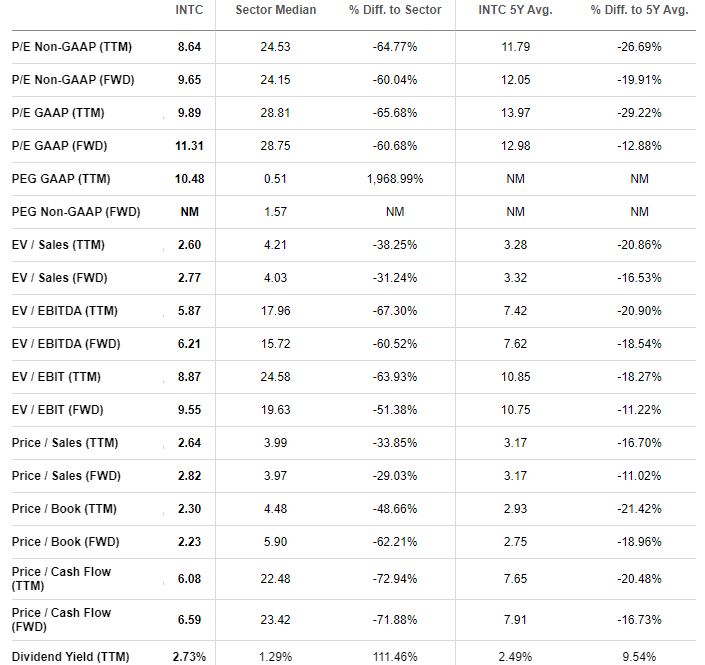

Recently, Intel began to reduce its reliance on the client computing group for growth as it hopes to take advantage of more profitable segments. Financials To that end, it’s worth a look at the revenue and operating contributions for each segment over the last several years. As you can see, the margins on the Data Center Group of 45.8% come in markedly higher than the 37.8% for the Client Computing Group. The most recent quarter showed significant gains in the segments Intel is focused on growing. Now, there are two important points we want to highlight that we feel get lost in the discussions about why Not to buy Intel. First, Intel’s revenues continue to grow, even in the client computing group. It’s not as robust as AMD’s or NVIDIA’s, but it’s still strong. Second, and more importantly, Intel generates an insane amount of cash – like $34 Billion per year in operating and $17 Billion in free cash flows. So when people point out that the company carries $35.6 Billion in long-term debt and say the $5.5 Billion dividend payout per year isn’t sustainable, you have to question what numbers they’re looking at. Valuation When you look at Intel’s valuation, it’s hard not to wonder whether it’s a value trap. Value traps occur when a company is barely growing, stagnant, or in a slow decline relative to the rest of the industry. According to these metrics, Intel is cheaper than the rest of the sector and itself over the last five years. That’s why we think management’s plans to shift their revenue streams are crucial to the company’s future. Our Opinion – 8/10 The current semiconductor shortage favors Intel and buys them time to execute on their transition to focus more on data centers. However, we want a nice margin of safety on this stock. So, we’d be interested in it below $50, ideally at $45. That would set up a nice dividend payment while we wait on their transformation. |