|

Proprietary Data Insights Retail Investors Top Commercial REIT Searches November

|

What we’re watching

|

|

Easterly Government Properties leases 7,500 square feet to the US government.

|

|

Stock Analysis |

The Government’s Largest Landlord |

Easterly Government Properties (DEA) leases 7.5 million square feet to one of the most consistent tenants in the world – the U.S. Government. In fact, 99% of their income comes from this one source. That might sound like a risky venture. Yet, the stock and its dividends have been remarkably consistent over the last five years. According to our proprietary data, DEA came out as one of the top commercial REIT searches by both retail and institutional investors last month. We know that investors favor REITs for their tax treatment and healthy dividend payouts. So we were curious what kind of upside potential existed for a stock that already pays close to 5%. Easterly Government Properties Holdings As a real estate investment trust, Easterly must:

With the US government as their one and only tenant, Easterly has a pretty consistent cash flow and outlook. The company targets :

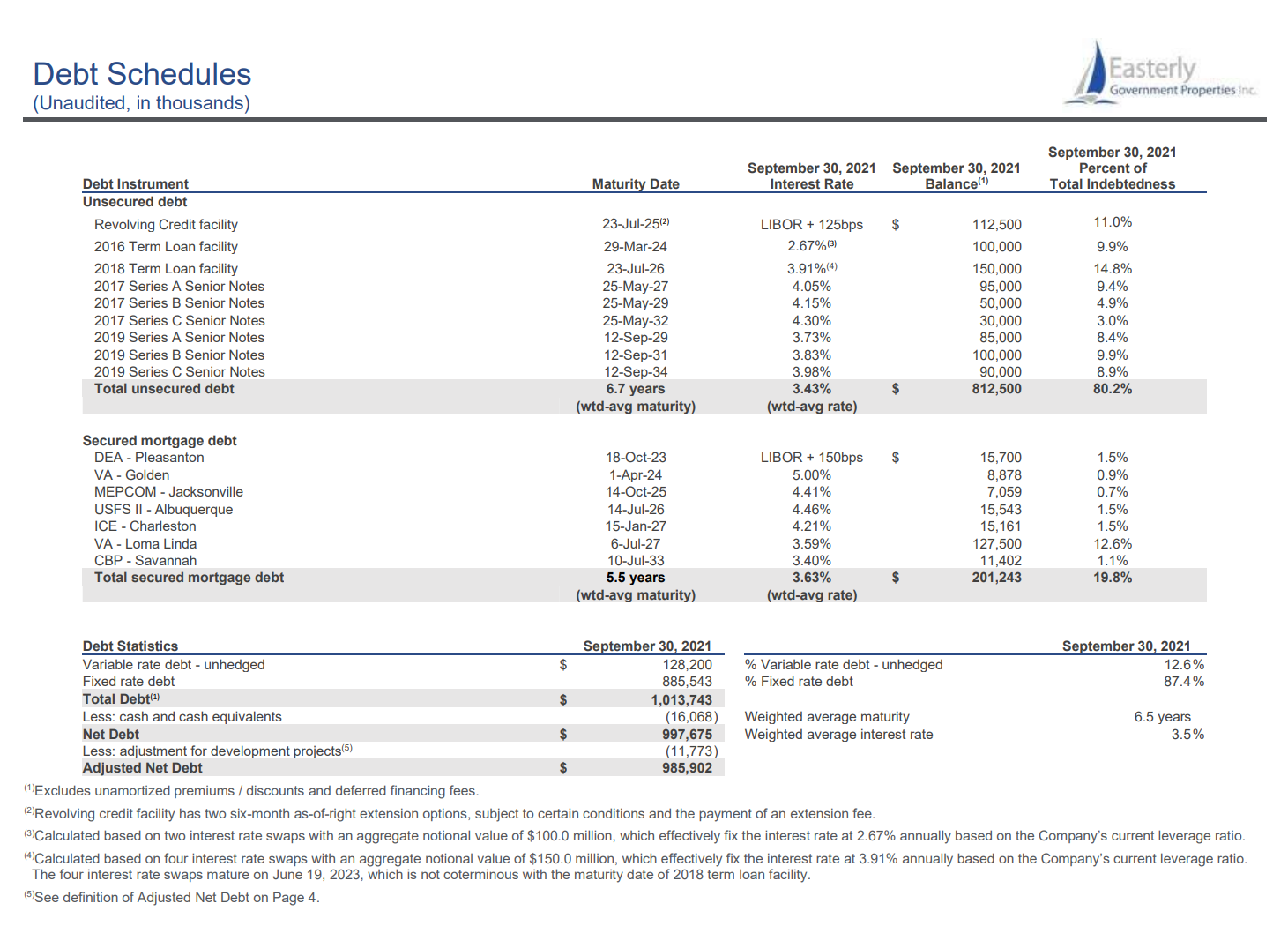

As government agencies expand, they need additional space tailored to their specific needs. Typically, the government solicits proposals from private companies to develop and lease such properties as published by the GSA. In the last three years, Easterly has added ~$410M, ~$381M, and ~$250M in acquisitions from 2018-2020 respectively. Currently, the company’s average remaining lease terms are the highest they’ve been since 2015 with 99% of their properties leased. Financials As we noted earlier, Easterly has shown consistent dividend growth that’s coincided with gains in revenues and margin expansion. As REITs are all about how they manage their debt, it’s important to look at the company’s financing. Currently, the company’s weighted average interest rate is 3.5% which is in line with all their current pro forma assumptions. We can also see below that the company has a heavy amount of debt scheduled to roll in 2027. Assuming they do not roll the debt earlier, they will be subject to higher interest rates should the Fed raise rates next year. One of the key ways to understand whether the company is doing well is to look at debt metrics and compare them to other REITs. So here are a two key metrics:

Growth for Easterly is slow but steady. Fed Considerations We expect the Federal Reserve to raise interest rates next year. That would impact REITs two ways. First, it increases the interest rates they would pay on their debt. Second, because investors treat REITs like treasuries with more risk, they’ll want higher dividend payouts should treasuries pay more. That means the price of a REIT needs to drop until the dividend yield is appropriate. However, we would like to point out that Easterly’s share price at $22 isn’t much different from the range from 2017-2018 of $18-$20 when rates were on the rise. Our Opinion – 7/10 We love Easterly below $20. But as a REIT, this is all about pennies. At the current price of $22, we aren’t interested. However, this is a stock we want to keep on our watchlist through next year. |