|

Proprietary Data Insights Retail Investors Top Commercial REIT Searches November

|

What we’re watching

|

|

A look at Mohawk Industries, a housing stock which is yet to explode.

|

|

Stock Analysis |

A Cheap Way To Play Housing |

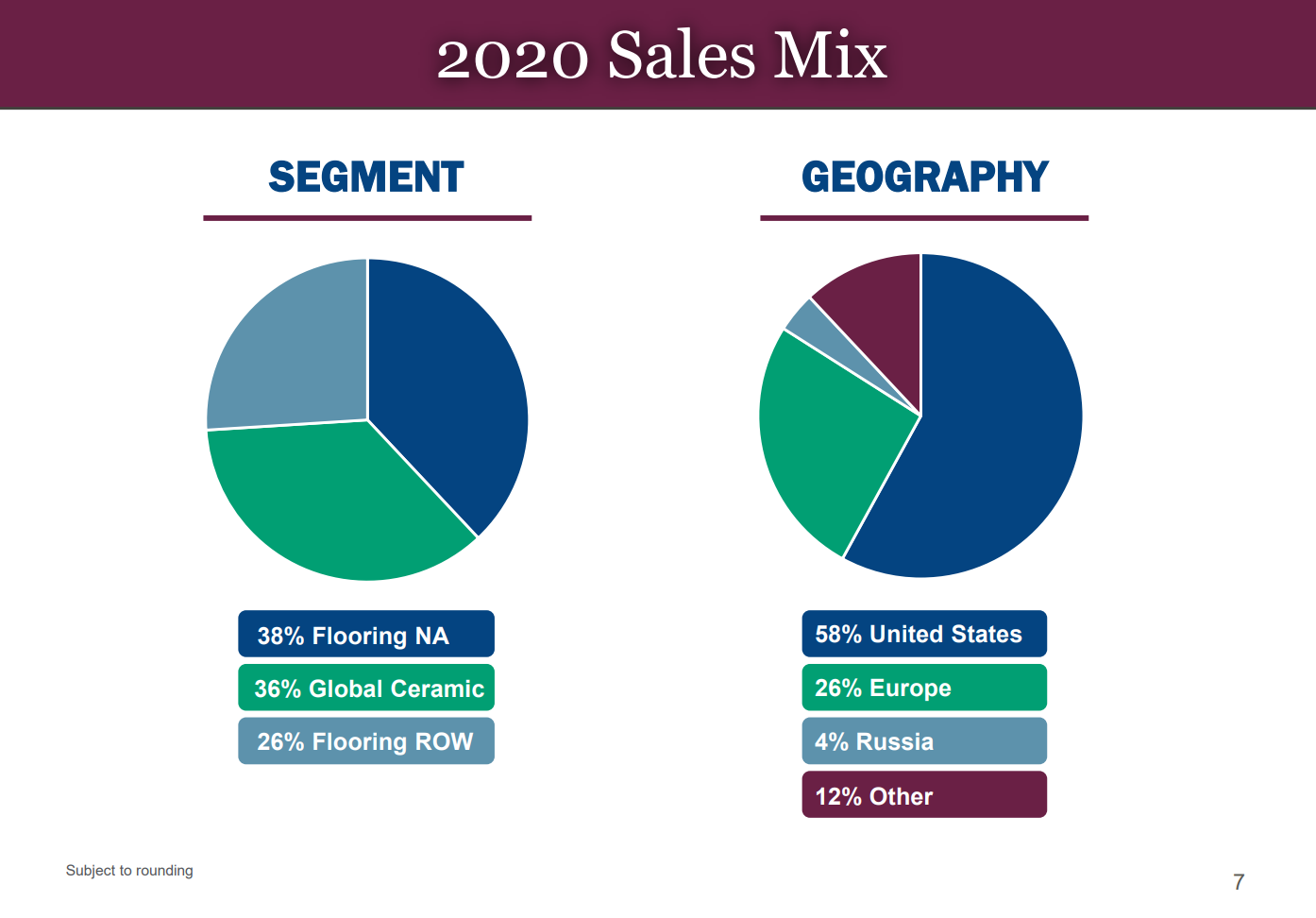

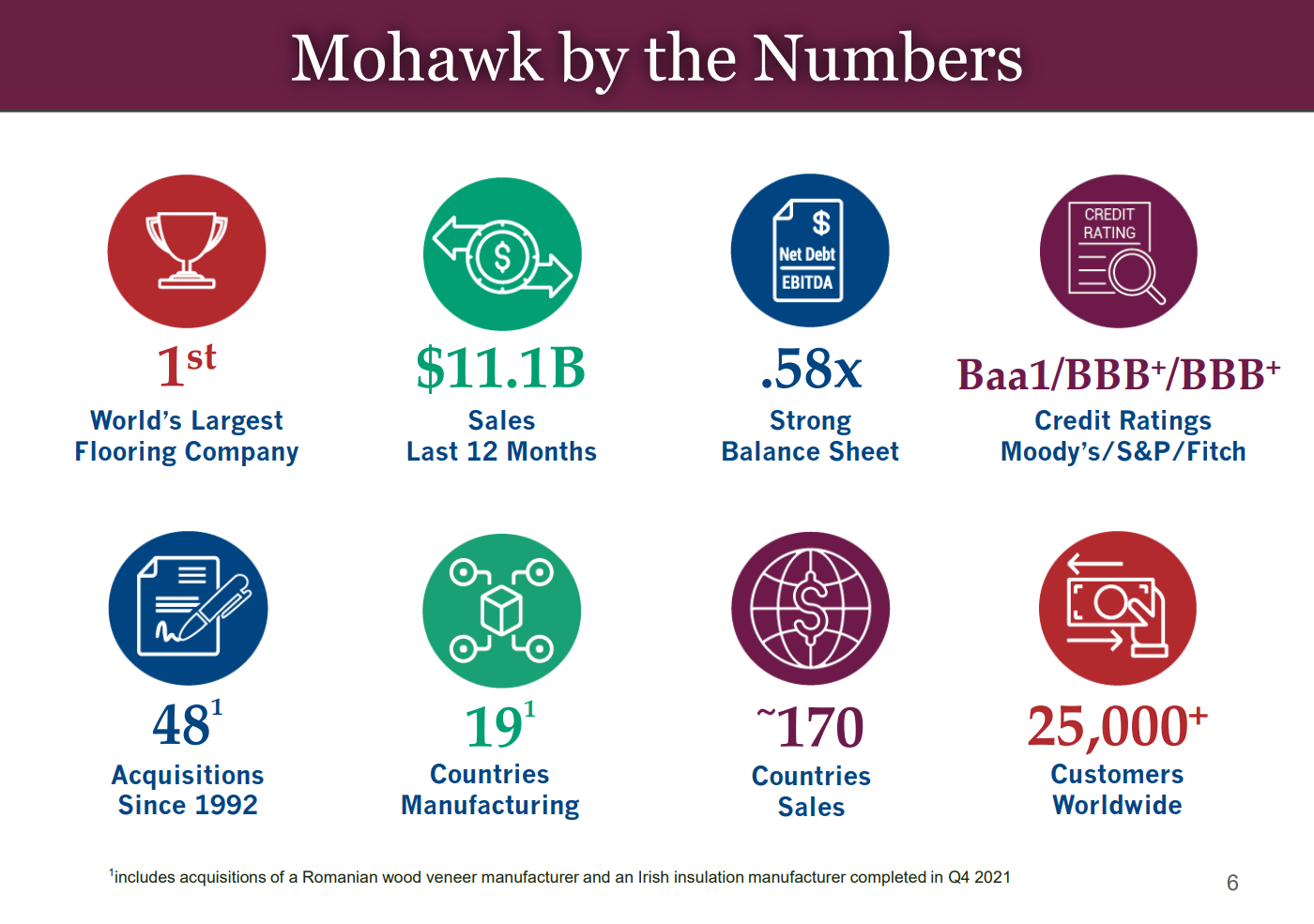

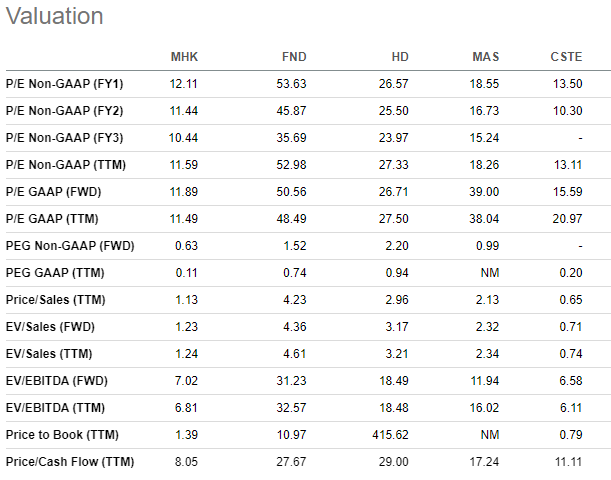

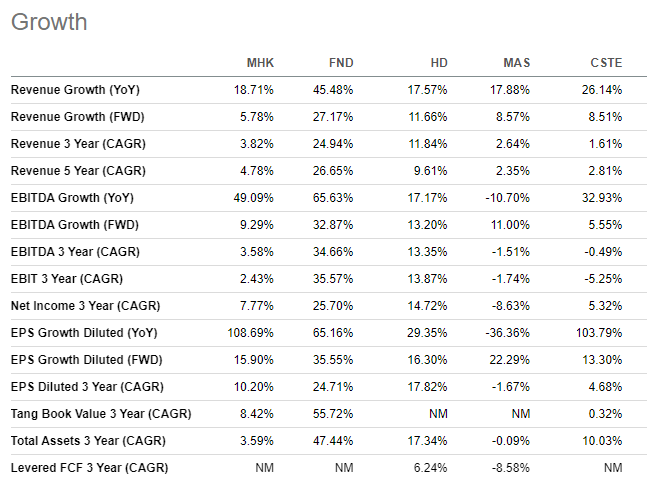

A Cheap Way To Play Housing Year-to-date, the S&P Homebuilders ETF (XHB) is up almost 50%. Imagine how excited we were when we found a housing stock that had yet to explode. As one of the leading global manufacturers of flooring products, we were surprised that Mohawk Industries (MHK) didn’t even make the top 5 home furnishings ticker searches amongst retail investors according to our proprietary data. Trading at just 12x forward earnings and 9x cash flow, this stock appeared to be a steal. But we’ve been fooled before. And considering the company’s heavy reliance on China for supply, we knew the current port congestion would factor into our analysis. The question was how much. Mohawk Industry’s Business With operations in Australia, Brazil, Canada, Europe, India, Malaysia, Mexico, New Zealand, Russia, and the United States, Mohawk Industries services customers around the world. The company is organized into three segments:

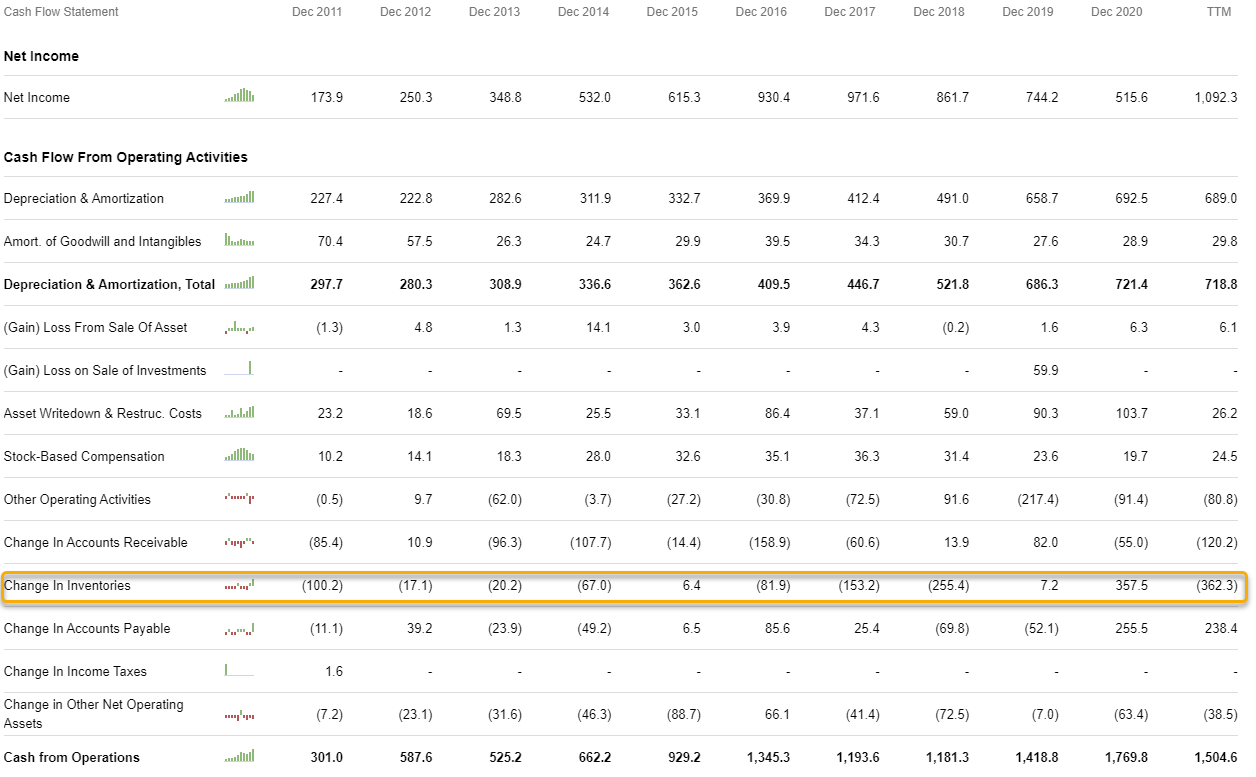

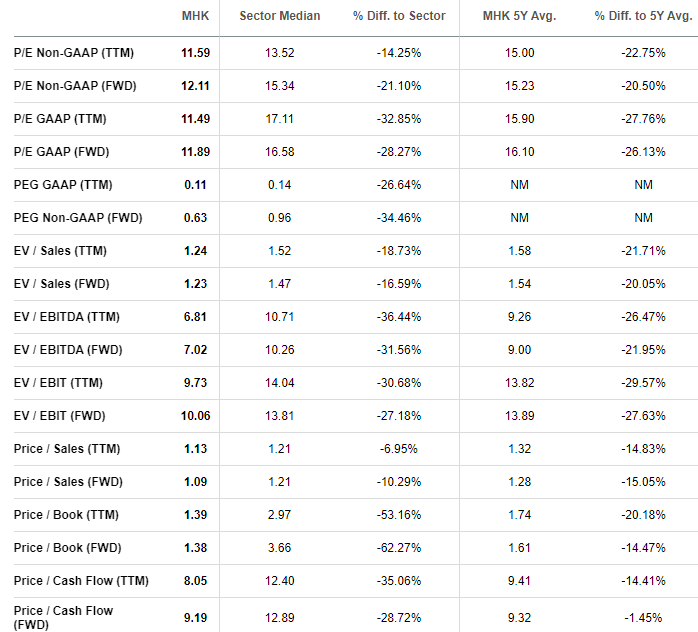

Mohawk’s sales have been boosted by home construction and remodeling, especially in the U.S., leading to a 16% increase in sales for the last 12 months. However, tight chemical supplies reduced the output of flooring products across the globe. Additionally, the high cost of natural gas in Europe has added pressure to that particular market. Still, as the company noted in the last quarter, most businesses are carrying significant backlogs which they hope to alleviate in the coming months. Financials While margins improved over the last year from pricing power and cost initiatives they were almost entirely offset by heavy inflation. Still, Mohawk is having its best year since 2017. The problem they face is one of growth. While investments have been made to increase capacity, the continued supply problems hinder production increases. As we noted earlier, high backlogs show demand is there. Yet, if Mohawk can’t increase its output quickly, those customers may substitute other products. You may have noticed that operational cash flow didn’t change all that much in the last few years even as earnings did. That comes largely as a result of changing inventory levels. Lastly, we want to note the company’s low debt levels with long-term debt at a paltry $1.66 Billion. Valuation Our valuation analysis was probably the most interesting we’ve come across in a while. Like we said earlier, housing stocks have been on a tear. Yet, investors left Mohawk behind. It’s hard to understand why considering the company beats out every single metric when you compare it to the consumer discretionary sector and its own 5-year average. When we tossed it up against other home improvement stocks it still beat them all. There was one place where Mohawk fell short – growth. The only knock we could really find against the company was the expected revenue growth. But even then, if you compared it to a company like Masco (MAS), it’s still undervalued relative to the rest of the market. Our Opinion – 10/10 We think Mowhak Industries is grossly undervalued. It’s entirely possible we’re missing something here that is depressing share prices. But at the moment, we conclude it’s driven by a poor growth outlook, which we expect to be fluid with upside potential. |