|

Proprietary Data Insights Retail Investors Top Internet Content & Info. Stock Searches November

|

What we’re watching

|

|

A look at a company which skyrocketed in price during lockdowns, Zoom.

|

|

Stock Analysis |

Zoom Might Be A Better Play Than You Think |

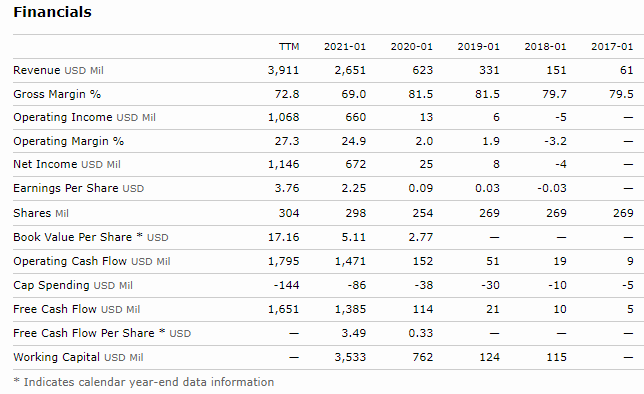

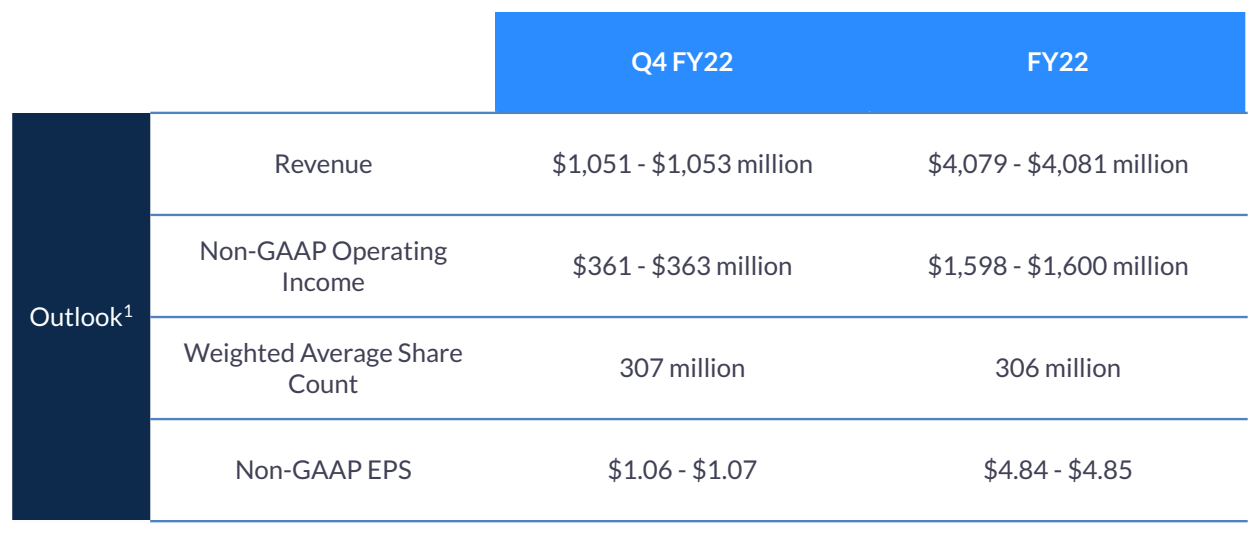

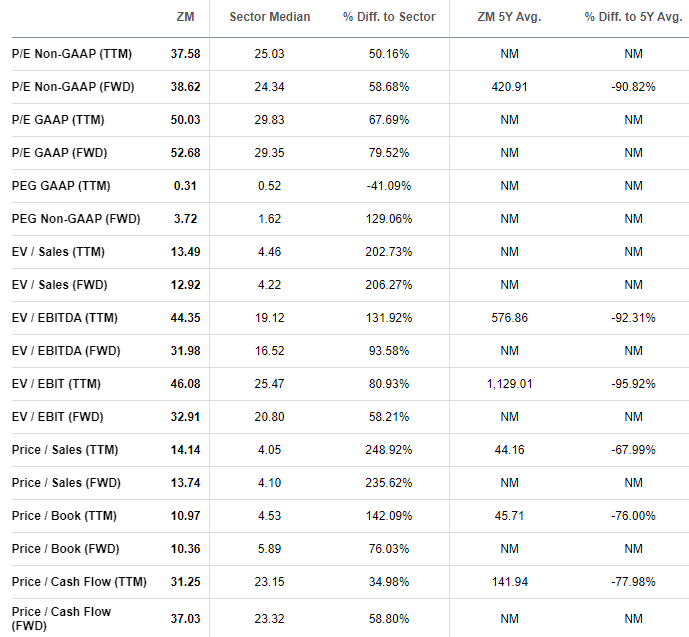

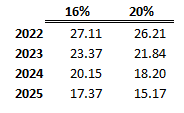

Back when lockdowns were all the rage, shares of Zoom Communications (ZM) went from just below $80 to nearly $600 in 38 weeks. Currently, the stock trades at $185, which appears to be a steal right? Bears will tell you that more competition and reality set in as the company reported slower revenue growth last quarter. But that ignores the underlying fundamentals of the company which trades at ~38x earnings and 31x cash over the last 12 months. To be fair, analysts forecast lower earnings and cash in the next 12 months. But we think there is a case to be made for shares of Zoom. And as one of the top internet content and information stock searches by retail investors last month, according to our proprietary data, we figured you all might be interested. Zoom’s Business If you don’t know about Zoom, you probably hid under a rock the last two years. Zoom Video Communications is a cloud-native platform that combines video, audio, phone, screen-sharing, and chat. Everyone from families to businesses used it for remote-working, collaboration, and good ol’ get-togethers. The company’s products include Zoom Meetings, Rooms, Phone, Chat, Conference Room Connector, Video Webinars, Zoom for developers, and the Zoom app marketplace. What makes Zoom unique is the platform’s ability to provide high-definition video and voice access across multiple devices while integrating within many popular platforms from Atlassian and Google to Salesforce and Slack. Zoom’s revenues come from subscriptions to its platform. Zoom Meeting is offered on a per-host-per-month basis in Basic, Pro, Business, and Enterprise tiers. Basic is offered for free as part of Zoom Video’s “freemium” strategy to convert these users into a Zoom Host, a paying user. Pro, Business, and Enterprise are offered at $14.99, $19.99, and $19.99, respectively, with a maximum of 9, 10, and 100 hosts, respectively. From their last quarterly call, the company has approximately 512,100 customers with more than 10 employees. Zoom went public in an IPO on April 17, 2019. Financials As a newer company, Zoom doesn’t have a ton of financial history. However, the company has been operating cash flow positive every year and delivered positive earnings all but one year. Growth skyrocketed during lockdowns with YOY revenues climbing 325%. That breakneck pace has slowed in recent quarters. The company provided the following guidance for Q4 and 2022. This equates to a ~54% growth to round out this year. What’s interesting is that analysts expect sales growth to slow markedly down to ~17% the following years. Keep in mind the video conferencing marketing is expected to grow at 15.5% per year through 2028. Microsoft announced a cheap version of its basic ‘Teams’ on December 1st, which directly competes with Zoom. A lot of bears believe it will significantly deteriorate Zoom’s revenues. However, many free versions already exist from other competitors. So we don’t expect this to have a material impact. Valuation As we went through the valuation metrics, we’re not too confident in the numbers assumed by the forward measures. Simply put, Zoom hasn’t provided guidance for next year’s earnings. So it seems a bit premature for analysts to assume flat earnings and worse cash flows than the current year. And this forms the crux of our argument for Zoom. Expenses certainly went up as the company spent marketing dollars to expand into Europe and the rest of the world. Do analysts expect that percentage to increase next year or is it on some other line item? Assuming it’s a transitory factor, if the company kept with 16%-20% growth on cash flows, which currently run around $1.8 Billion per year, with 306 million shares outstanding, this is what your price to cash flow would look like over the next 5 years: Our Opinion – 7/10 We feel that sentiment is far too bearish with this stock. However, we recognize that there’s uncertainty around the future growth both good and bad. Plus, the company is limited in its product offerings. What would make us more comfortable? Shares closer to $100. That might seem ridiculous considering the stock has already pulled back almost 70%. But frankly, when we want to put money to work it’s at the prices we want. There is always another stock around the corner. $100 is where this becomes a no brainer. |