|

Proprietary Data Insights Financial Pros Top Speciality Retail Stock Searches December

|

What we’re watching

|

|

A look at a company that was a godsend during lockdowns, Stitch Fix.

|

|

Stock Analysis |

Stitch Fix Tanks Into The Buy Zone |

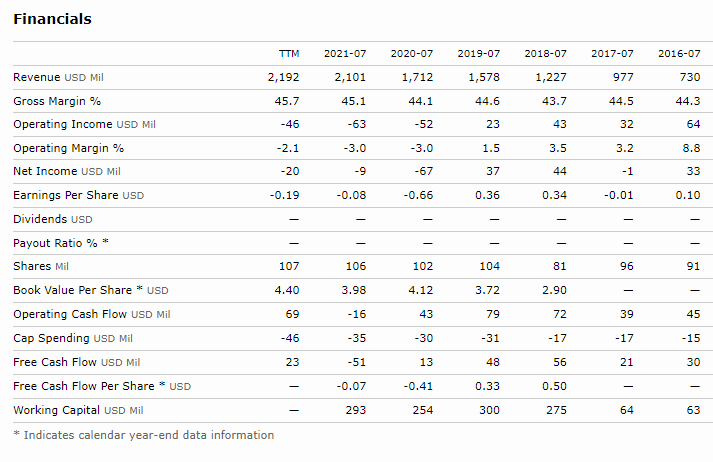

Stitch Fix Tanks Into The Buy Zone It ain’t easy being a clothing retailer these days. For those of us stuck at home during the pandemic, Stitch Fix (SFIX) was a godsend. The popular fashion subscription service saw revenue growth over 20% except for 2020. But the most recent quarterly call gave investors a lot to chew on. Shares plunged more than 23% in one day. For us, that places the stock in the ‘buy zone.’ While others run away from the fashion company, we see huge potential. At 1x FY’22 sales, we think it’s a steal. And considering it’s barely behind meme star GameStop in the top retail searches by financial pros this month according to our proprietary data, we know folks are interested. Stitch Fix’s Business Online personal styling retailer Stitch Fix started in 2011 as a women’s apparel subscription service expanding to men in 2016. The company provides styling services and merchandise from other brands as well as its own private label Exclusive Brands. Stitch Fix uses data science and human judgment to deliver personalized product shipments. Each box is known as a ‘Fix’ and is curated by company stylists in exchange for a styling fee. Five items are included in each box. Should you purchase all five items you receive a 20% discount on the total as well as a credit on the styling fee. You can also buy an annual Style Pass which comes with unlimited styling for a year for $49. More recently, the company launched ‘FreeStyle’ where customers can shop brands and make purchases outside of their subscription. This service came with high advertising spend since its launch. Additionally, privacy changes hurt Stitch Fix’s ability to target customers. The CEO suggested the biggest issue the company faces is getting more customers to buy items on the website. Many Fix customers struggle to transition to the Freestyle option with many unaware it even exists. Financials We want to start by pointing out that StitchFix isn’t growing at gangbuster rates of 50%-100% that we see with some startups. However, they continue to grow their active clients, revenues, and revenues per client steadily. While we don’t have specifics for the breakdown on Stitch Fix’s sales for subscriptions vs Freestyle, we want to highlight Q1 Freestyle sales were up 40% YOY with total revenues up 19% YOY. As we mentioned earlier, the company grew revenues +20% per year with the exception of 2020. We also want to point out the positive operating and free cash flow every year except for 2021. Going forward, the company expects total net revenue growth in the high single-digit range with adjusted EBITDA between 1%-2%. Note: Adjusted EBITDA’s biggest expense change is typically stock-based compensation. That type of forecast isn’t something you want to hear from a ‘growth’ company, especially one that has yet to turn a positive EPS. However, FY’23 growth is still expected 14% with FY’24 just below 10%. Currently, the company carries nearly $250 million in cash as inventory levels declined. And to that end, the company has begun to order out 6-9 months to avoid stock outages which so far have not hindered sales. Lastly, we want to point out that SG&A expenses have increased from ~45% to just shy of 50% of revenues as marketing and tech investments ramp up. We expect that to continue as the company iterates through FreeStyle onboarding to get it working right. Valuation The majority of valuation measures don’t work given the company has negative earnings. That said, we want to point out the company currently trades at <1x trailing and forward sales. By nearly every standard, that’s incredibly cheap. Given the investments into customer onboarding and experience, we feel the potential payoff in higher revenues per Fix customer and new growth from FreeStyle will significantly add to the company’s bottom line. Our Opinion – 10/10 Shares could trade lower but not by much. We feel the company is simply too cheap relative to its potential growth. The company engenders strong customer loyalty that creates a stable base from which to grow. All they need is time. |