|

Proprietary Data Insights Retail Top Furnishings, Fixtures, & Appliances Stock Searches December

|

What we’re watching

|

|

A look at the demand increase for home appliance manufacturer Whirlpool.

|

|

Stock Analysis |

Why The Timing For Whirlpool Is Right |

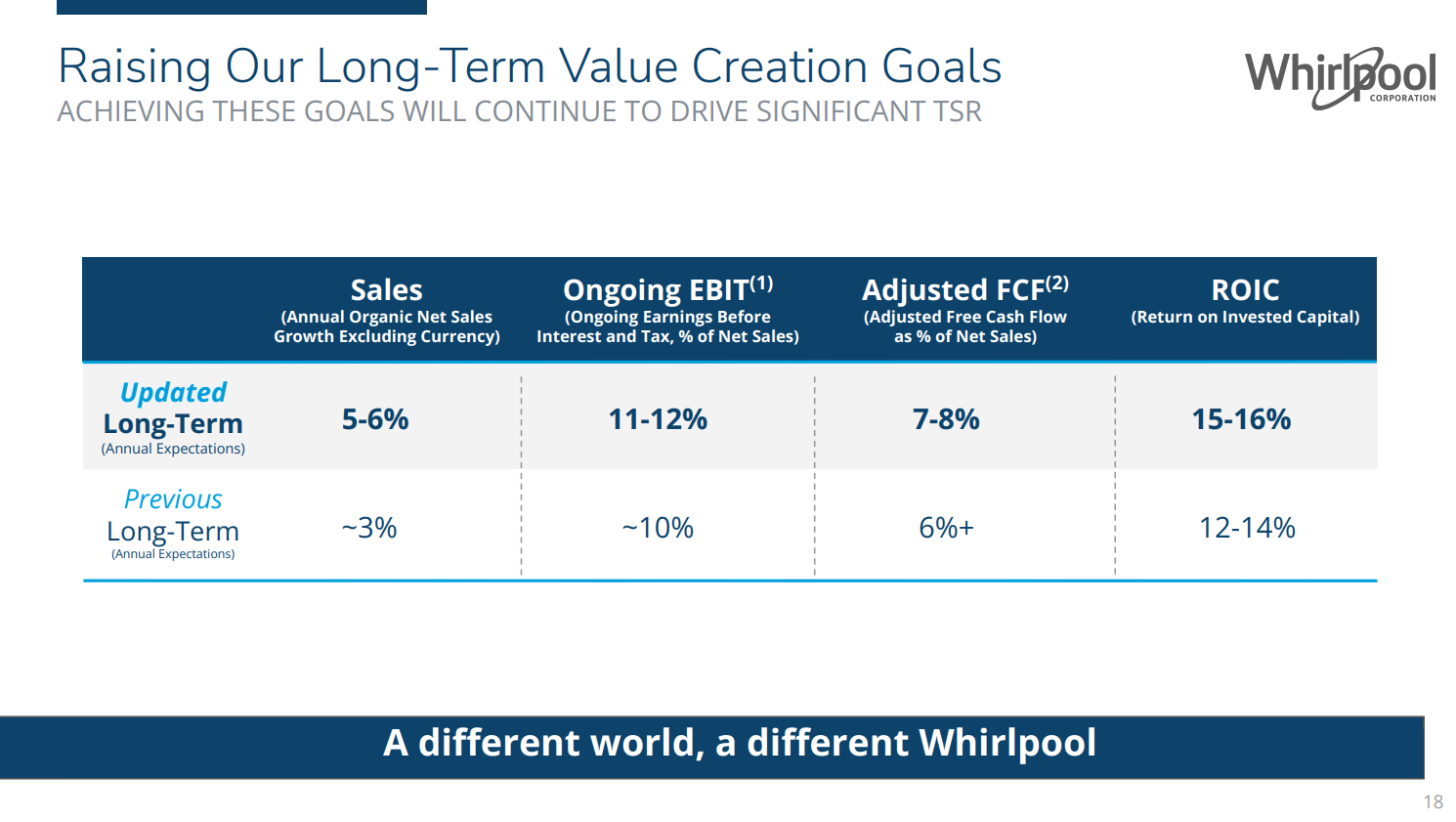

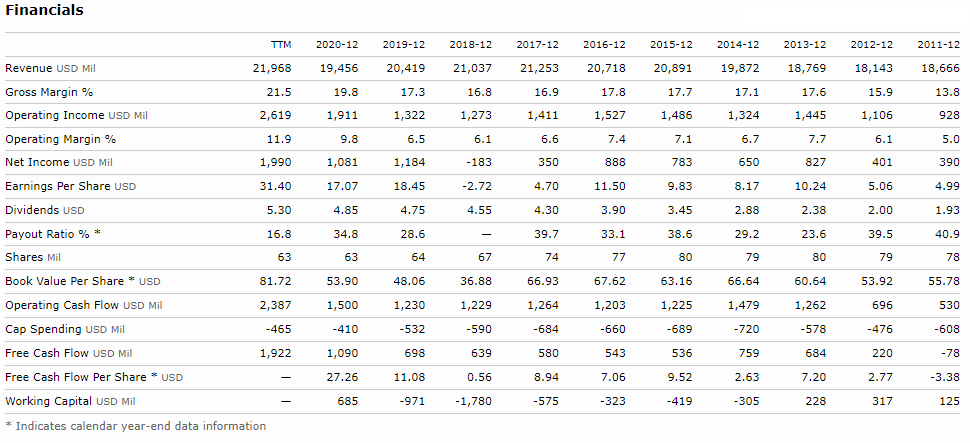

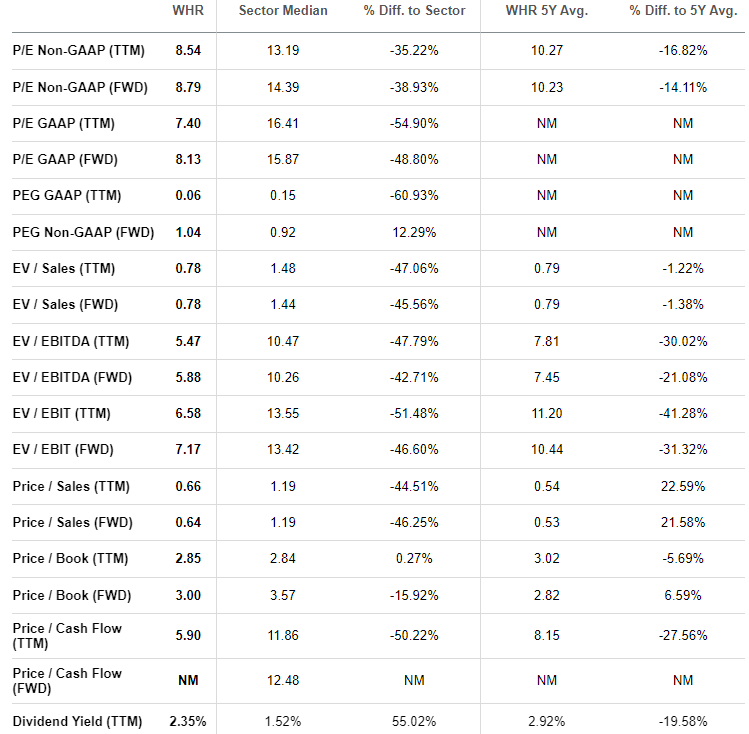

Despite directly benefiting from washing-machine tariffs, Whirlpool (WHR) ate an extra $50 million per quarter in higher steel and aluminum costs. Those numbers have skyrocketed as Covid crimped global supplies. Yet, demand for Whirlpool rose steadily, far outstripping supply, allowing the company to achieve higher price points. With a recent deal between the US and EU to remove steel and aluminum tariffs starting January 1, 2022, Whirlpool finds another avenue to pad its profits. And as investors, we want to see if we can pad our pockets. As the 5th highest furnishings, fixtures, and appliances stock search amongst retail investors for the month, according to our data, we feel far too many people may be overlooking the stock’s near-term potential. Trading at just 7.4x trailing earnings and 8.13x forward earnings, this stock could take a lot of investors by surprise. Whirlpool’s Business Based in Benton Harbor, Michigan, Whirlpool is one of the largest manufacturers of home appliances in the world with products in 14 countries and marketing in nearly every nation around the globe. The company’s products include laundry appliances, refrigerators and freezers, cooking appliances, and other small household appliances such as dishwashers and mixers. Breaking down the regions, Whirlpool earns 56% of revenues from North America, 16% from Europe, 21% from the Middle East & Africa, and 7% from Asia. Currently, management is focused on cost-based price increments coupled with cost-reductions initiatives aimed at boosting business efficiency and margins. That’s led to the updated long-term outlook shown below. Whirlpool expects strong housing, equipment replacement, and increased disposable income to contribute to the higher sales outlook. Financials Over the last decade, sales and margins climbed steadily up until 2017. Both slid up through Covid before a very strong rebound. Notably, operating margin sits at the highest levels in the last decade along with cash flow. Part of this is driven by the company’s divestiture from Whirlpool China and Turkey which added $286 million in cash to 2021. With operational improvements hitting the bottom line along with stronger production, the company increased its guidance for the balance of 2021 during the last quarter’s earnings call. What’s impressive is the company’s average revenue growth over the last decade is around 1%-2%. So the increased forecasts for this year to 3% organic growth plus long-term growth of 5%-6% is quite impressive. Lastly, we want to point out the company’s fortress balance sheet. Whirlpool holds nearly $3 billion in cash with a bit less than $5 billion in long-term debt. That provides them with plenty of firepower to spend on CAPEX and acquisitions. Valuation As we mentioned earlier, Whirlpool’s valuation metrics are quite juicy. Although the company trades at a slightly higher price-to-sales ratio than it’s 5-year average, we think this fails to capture future revenue growth. Otherwise, the company dominates every category compared to the consumer discretionary sector. And we love the low price to cash flow and a dividend yield of 2.35%. However, we’d like to see the company put more of its capital to work in the form of production expansion or share buybacks. Our Opinion – 9/10 We think Whirlpool offers incredible value and current forecasts by the company and analysts don’t take into account lower steel and aluminum costs next year. That, along with heavy demand should keep production flowing, pricing high, and margins improving. |