|

Proprietary Data Insights Retail Top Furnishings, Fixtures, & Appliances Stock Searches December

|

What we’re watching

|

|

A look at a word leader in building materials and composite solutions which is benefitting from increased construction spending.

|

|

Stock Analysis |

Owens Corning Is A Double-Edged Sword |

Construction spending continues to run hot on everything from housing to commercial buildings. As the world leader in building materials and composite solutions, Owens Corning (OC) benefits from the strong demand. Yet, heavy inflation drags down their margins. That’s probably why it ranked last amongst financial pros’ building products and equipment stock searches this month according to our proprietary data. However, we feel there might be a near-term catalyst once we make it past the holidays. And that could send shares soaring. Owens Corning’s Business Know all that Pink Panther insulation in your attic? You can thank Owens Corning for that. Started back in 1938, the company operates three segments:

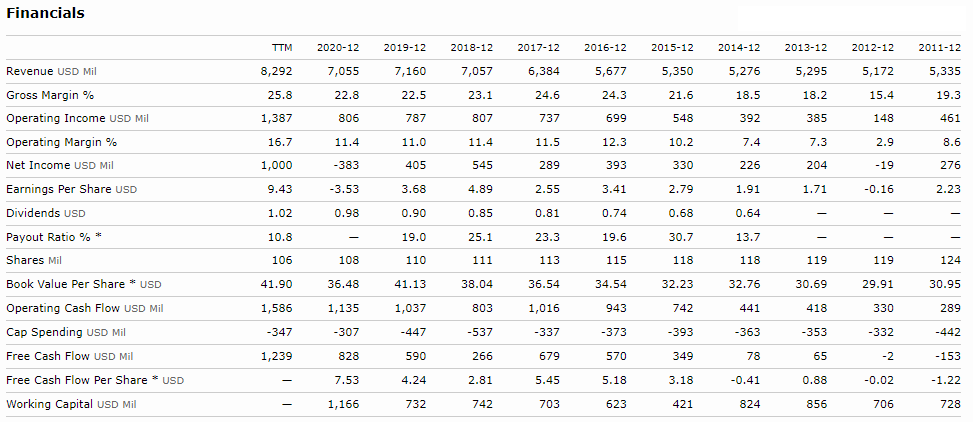

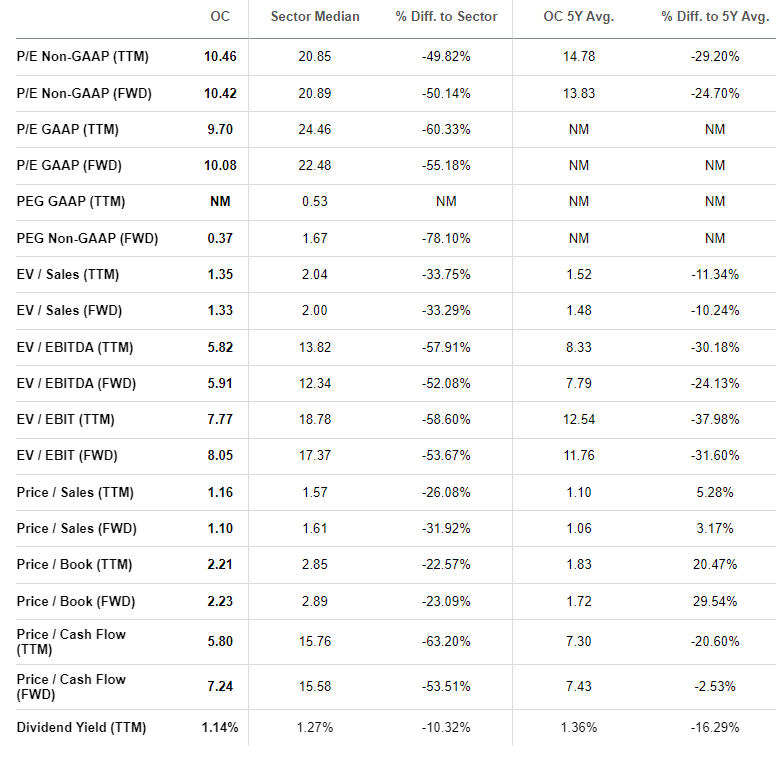

Note: Corporate eliminations were 2.9% of net sales. Currently, the company is focusing on its key markets, including North America, Europe, and India, as well as creating a more cost effective network through improved supply chains and manufacturing processes. Owens added to their top line through acquisitions of vliepa GmbH and Paroc. At the same time, they shed assets such as their insulation site in Santa Clara, California. Financials After fairly robust growth through 2018 of close to 10%, sales began to slip. It wasn’t until the most recent year that the company saw double digit revenue expansion. To offset most of the inflationary pressures, Corning increased prices and plans to keep at it to ensure a positive price/cost mix. That’s allowed them to push gross margins to nearly 28% in the most recent quarter with operating margin just shy of 18.5%. As part of its growth strategy, the company maintains low levels of debt, with long-term obligations at $2.89 billion with nearly $1 billion cash on hand. With free cash flow of nearly $1.2 billion, that frees management to make acquisitions to expand the business as well as invest in their supply chain. Valuation Current value metrics for Owens Corning paint a stock priced at a discount. With shares trading at just 10x earnings and 6x-7x cash flow, Owens Corning offers better value than the vast majority of stocks in the industrial sector. In fact, shares trade better than their 5-year average with the exception of price to sales, price to book, as well as dividend yield. Our Opinion – 7/10 Inflationary headwinds should subside in Q1-Q2 of next year as supply chain issues clear. Yet, Owens will still have all its price increases in place. That should protect margins against what we see as heavy construction demand for the next several years. That said, even as cheap as the company is now, we’d prefer a better margin of safety with the company and be more interested in shares closer to $80. |