|

Proprietary Data Insights Financial Pros Top Comm. Services Stock Searches December

|

What we’re watching

|

|

A look at Verizon expanding their 5G network by $18 billion per year.

|

|

Stock Analysis |

Verizon Wireless |

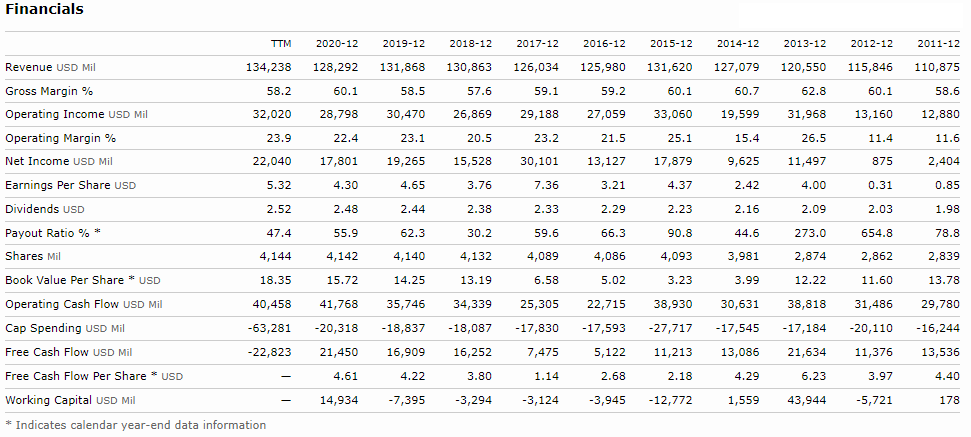

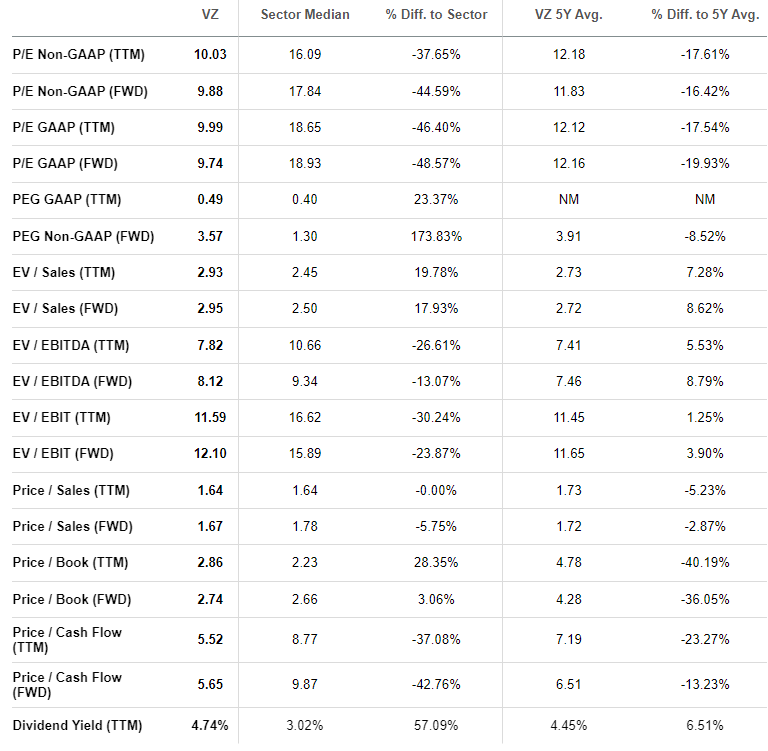

The global 5G market is anticipated to hit $667.9 billion by 2026 with compound annual growth of 122.3%! Verizon (VZ) aims to lead the charge making serious investments into the field. The company currently spends ~$18 billion a year to expand its 5G network. We see the amazing potential here. The question is can it offset the challenges Verizon faces? Higher rates hurt utility and telecommunications companies in two ways. First, duethe heavy debt load, interest expenses rise crimping profitability. Second, investors treat high dividend payers like telecom companies and utilities like bonds. So if the Fed raises rates, that lowers the price of US Treasury bonds and should feed through to the telecom and utility sectors. But markets might have already priced in the worst of it. Considering Verizon was the second most searched telecom stock this month by financial pros, we know there’s a lot of interest. So we thought it best to take an in-depth look to determine its value. Verizon’s Business We won’t bore you with explaining who Verizon is or what they do. Instead, we’ll dive into the revenues which are split into two categories: consumer (70.9% of revenues), business (23.4% of revenues), and its recent sale, as of Sep 21, 2021, Verizon Media. Verizon holds around 40% of the postpaid phone market, about 1/3rd greater than AT&T. In the last decade, the company divested from much of its traditional fixed-line footprint. However, the company holds extensive fiber assets in most major US metro areas that historically served enterprise customers. Along with its 5G, Verizon continues to expand its fiber network with the goal of supporting wireless networks while enabling them to offer new services. Recently, Verizon teamed up with Amazon Web Services to create and deploy low latency applications to mobile devices using 5G, becoming the first to offer such a service. Similar to AT&T, Verizon found the move into media too costly. The company bought AOL in 2015 for $4.4 billion and Yahoo two years later for $4.5 billion. In 2018, the company wrote down $4.6 billion. The recent sale of Verizon Media to Apollo Capital adds $4.25 billion in cash, preferred interests of $750 million, and a 10% stake in the new company. Financials Verizon kept its 10-year average revenue growth just below 3% leading into the pandemic. At the same time, gross and operating margins remained flat outside of the years where acquisitions and writedowns occurred. Currently, management projects 3%-5% wireless revenue growth for the remainder of this year. Before we discuss the company’s debt, we want to point out a few key items. First, the payout ratio, which looks at dividend payouts in proportion to earnings, trended around 50% over the last 5 years. With an operating cash flow of between $25-$40 billion annually, the company had plenty of room to invest in its future and pay out shareholders. Free cash flow, which is operating cash flow minus capital expenditures, landed at roughly $16-$20 billion annually. Now, on the balance sheet, Verizon currently holds $143 billion in long-term debt or around 3.5x-5.5x operating cash flow. To give you a point of reference, AT&T holds $155 billion in long-term debt or around 3.4x-5.0x operating cash flow. Valuation Given the significant changes underway with AT&T, we’re going to look at Verizon’s valuation metrics by themselves. Verizon comes in at a discount compared to the communications actor except when it comes to enterprise value (EV) to sales and price-to-book. However, these aren’t metrics we’re too concerned with. Instead, we focus on the price to cash flow, which is below the sector median and the company’s own 5-year average, the nice dividend yield, as well as the price-to-earnings growth (PEG) ratios. All of these suggest Verizon trades at a nice discount. Our Opinion – 7/10 While we like the valuation, we feel that AT&T is doing more to invest in the 5G space and controlling its debt better. With interest rates set to rise, that will be a key driver of profitability in the near future. Nonetheless, we’d prefer a greater margin of safety, with share prices below $50 before we’d be interested. |