|

Proprietary Data Insights Financial Pros Top Home & Hardware Stock Searches December

|

What we’re watching

|

|

With Lowes shifting direction it has become more appealing than Home Depot.

|

|

Stock Analysis |

We Prefer Lowes to Home Depot |

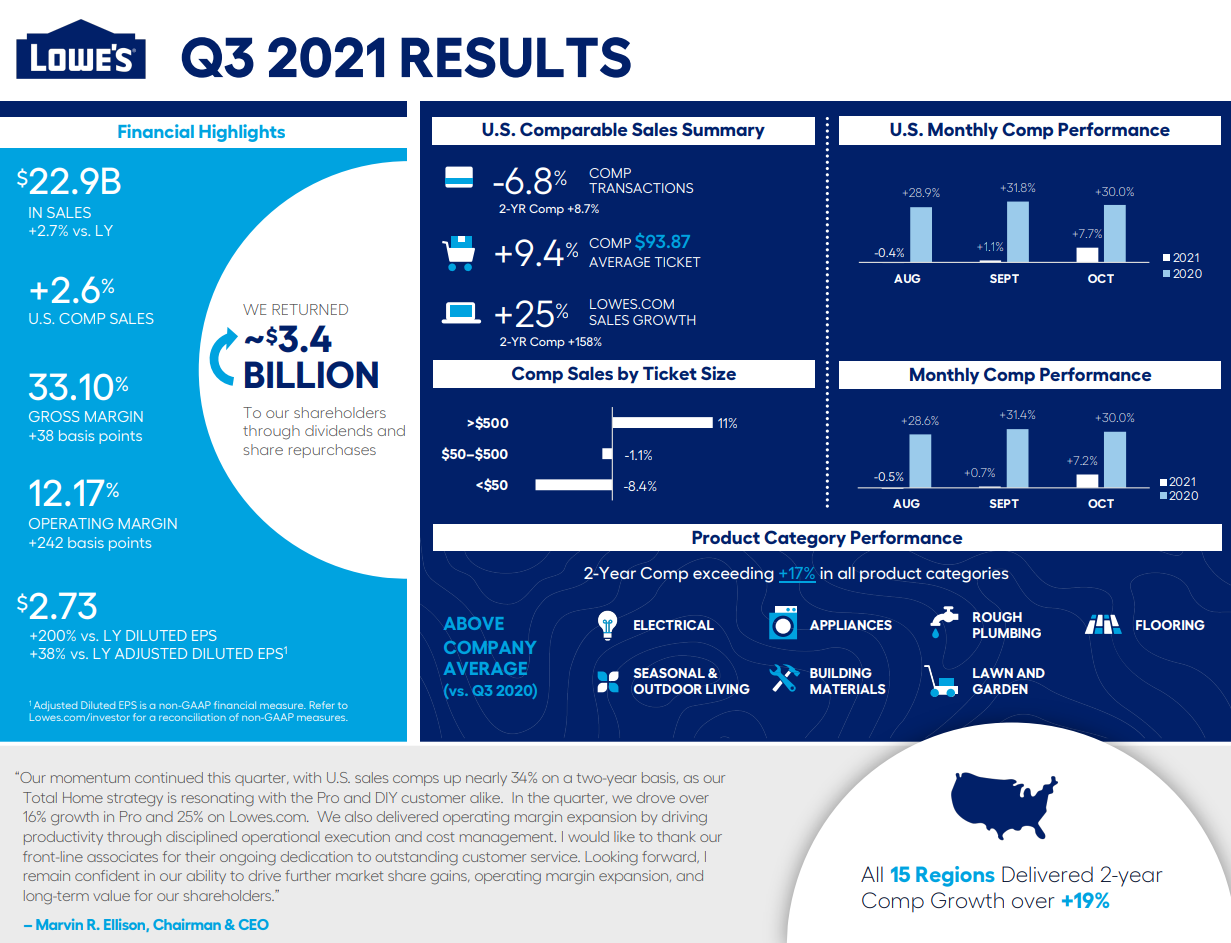

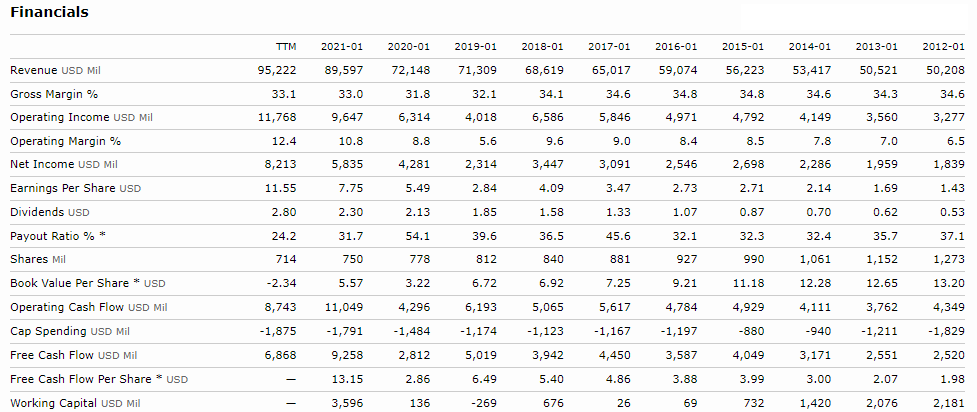

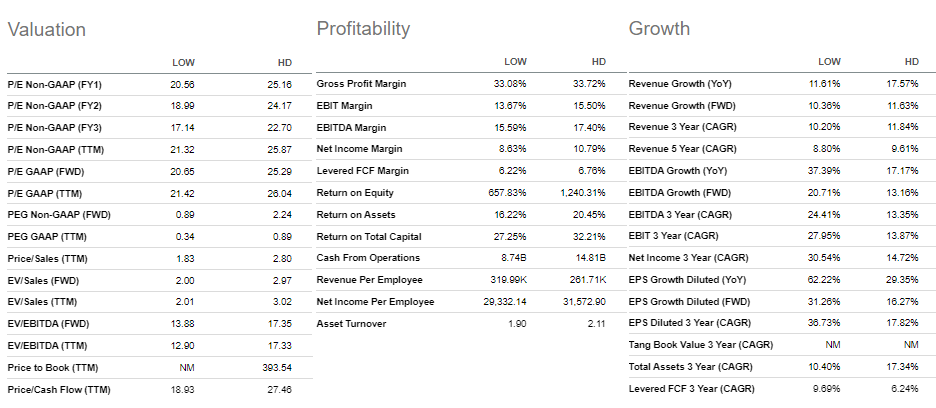

Home Depot (HD) generates nearly 50% more sales annually than Lowes (LOW). It’s also got a better 10-year revenue growth rate leading into the pandemic at 4.23% compared to 3.99%. Frankly, Home Depot was a better stock than Lowes…Was being the operative word. Under the direction of Marvin Ellison, a former HD executive, Lowes began to transform itself starting in 2018. The company shifted focus from retail to professionals as well as boosting online sales. While Lowes didn’t garner nearly as many searches amongst financial pros this month, we actually see that as an opportunity. You see, everyone knows about the housing and construction boom. But while they focus on the biggest player, we looked at which company could outperform in the coming year. And our bet is on Lowes. Lowes Business As the second largest home improvement retailer, Lowes has always been judged relative to Home Depot. Although both companies carry different brands, Lowes stores are seen as clean and more inviting with lighter paint colors and more attentive staff. However, they struggled to make inroads with construction professionals the way Home Depot has. About 45% of Home Depot’s total sales come from Pro customers compared to 20%-25% of Lowes’ total sales. In the most recent quarters, Lowes managed to grow sales amongst its Pro customers by ~25%. That helped Lowes increase sales and expand margins in the most recent quarter. The company’s current ‘Total Home Strategy’ incorporates growth with Pro customers as well along with expanding the online business, installation services, and products while driving localization. Financials Lowes saw steady growth, effectively doubling their total sales over the last decade. At the same time, gross margins compress while operating margins expand. During that same time earnings grew by 6x while operation cash flow remained fairly steady. It wasn’t until quarters that the company started to see a marked increase in cash. Additionally, Lowes implemented shareholder-friendly initiatives, reducing the total shares outstanding by nearly 50% while paying out a dividend. Unsurprisingly, this led shares to quintuple from 2012-2020. Lastly, we want to point out that Lowes holds $23 billion in long-term debt on its balance sheet. However, it also carries $6.6 billion in cash along with more than $16 billion in inventory. So while the debt level is high, most of it is backed by inventory assets. Valuation For the valuation, we felt it best to prop Lowes up against Home Depot. Let’s start with our typical valuation metrics. Compared to HD, Lowes is cheaper in terms of price-to-earnings ratios (P/E) whether looking backwards or forwards. It’s also cheaper on a price-to-sales and cash flow basis. However, Lowes’ price-to-earnings growth (PEG) ratio is less than half that of Home Depot. Now, when we turn to margins, things get a bit more interesting. Gross margin is nearly identical between the two companies. However, Lowes has a lower EBITDA and net income margin. Not by much, but enough that justify its need to expand its omnichannel presence and penetration with Pro customers. The higher margins translate to the higher return on assets, equity, and capital for Home Depot compared to Lowes. That said, Lowes exhibits much higher growth in EBITDA, Net Income, and EPS despite lower revenue growth. This is where we see the most value as the company rearranges its business to mimic Home Depot. Our Opinion – 6/10 Although we believe Lowes is a better value than Home Depot, both appear frothy in this market and priced to perfection. Instead, we’d be interested in Lowes at a much lower price, closer to $150 per share. |