|

Proprietary Data Insights Financial Pros Top Farm Products Stock Searches December

|

What we’re watching

|

|

A hawkish Federal Reserve and Omicron variant have given Wall Street analysts a lot to think about heading into 2022.

|

|

Stock Analysis |

Bunge’s Big Agribusiness |

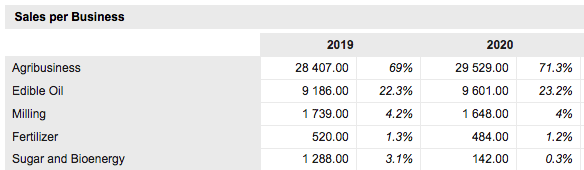

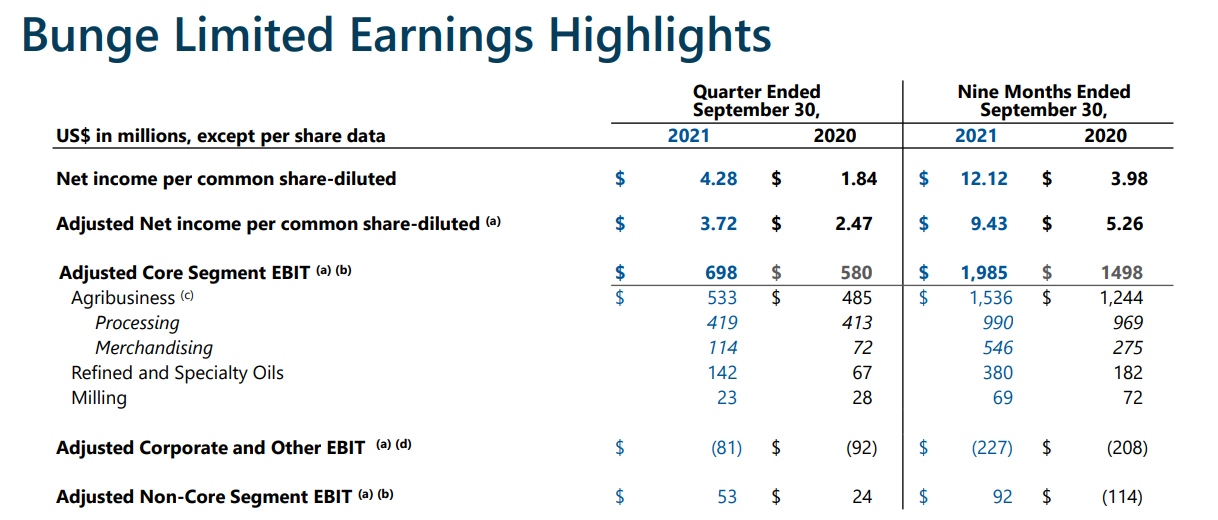

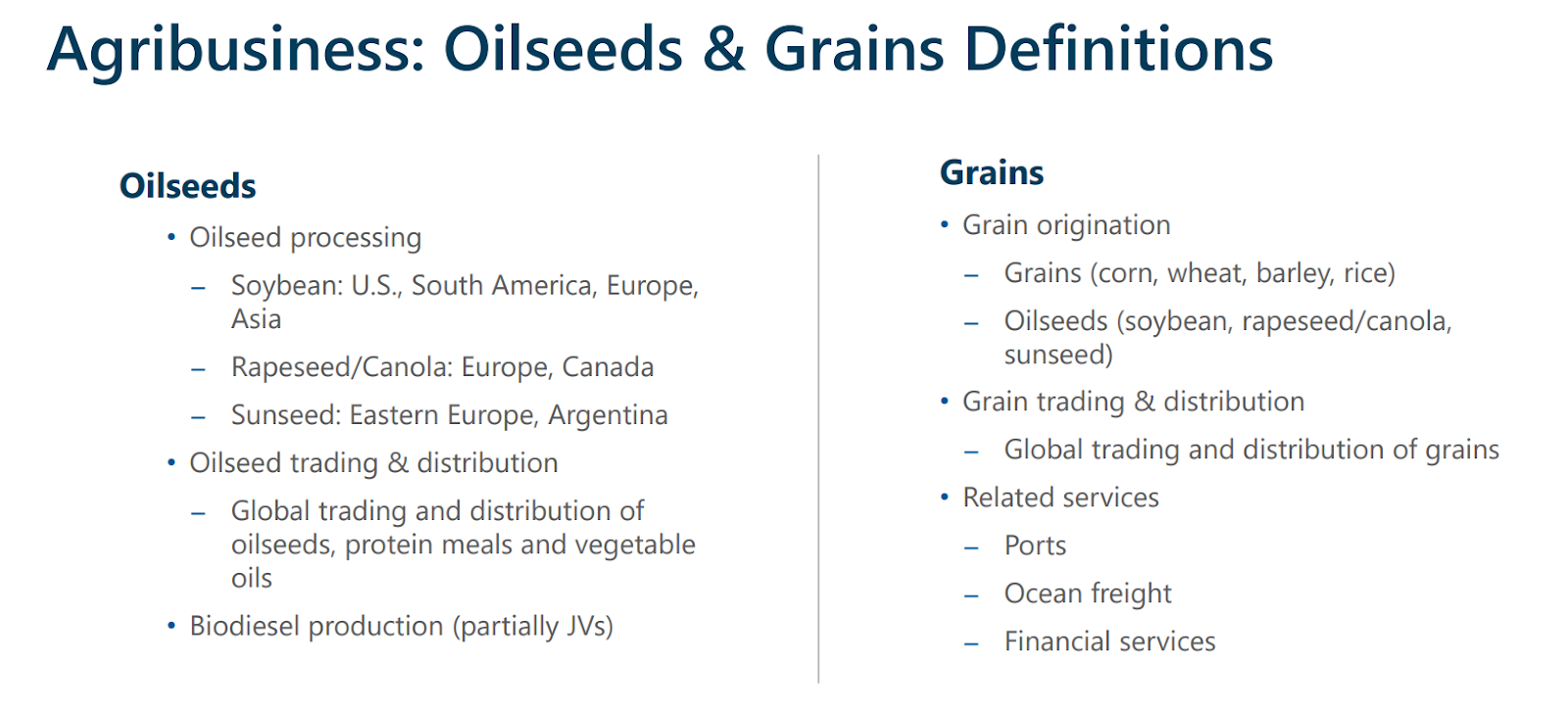

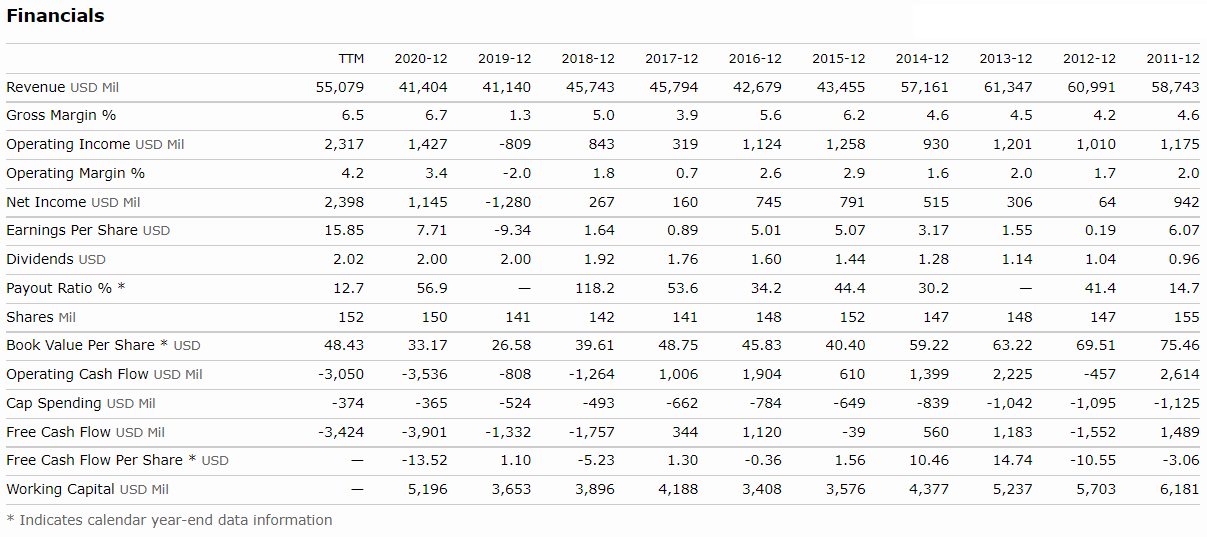

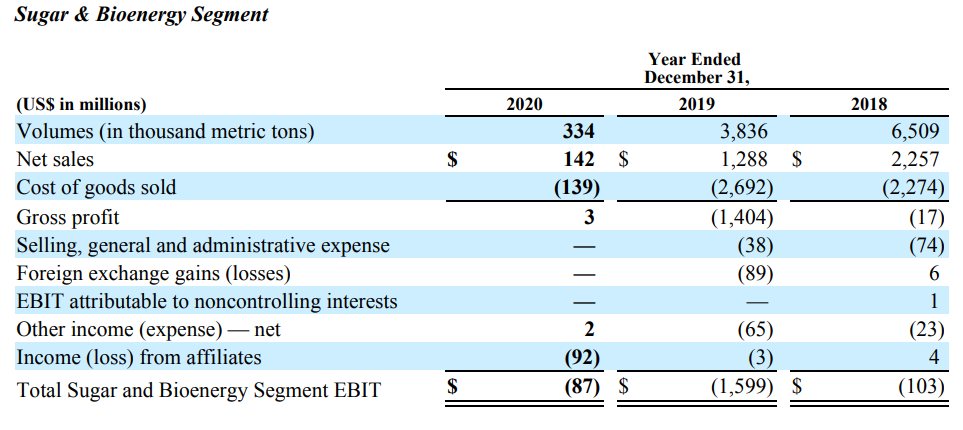

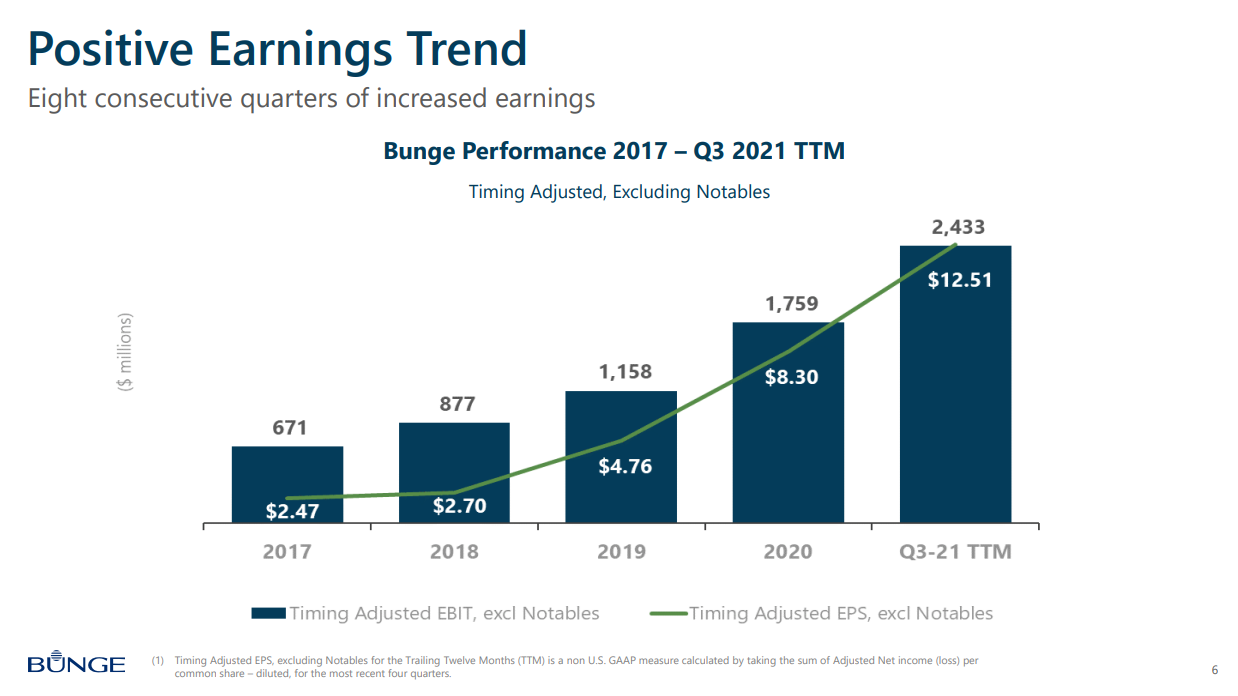

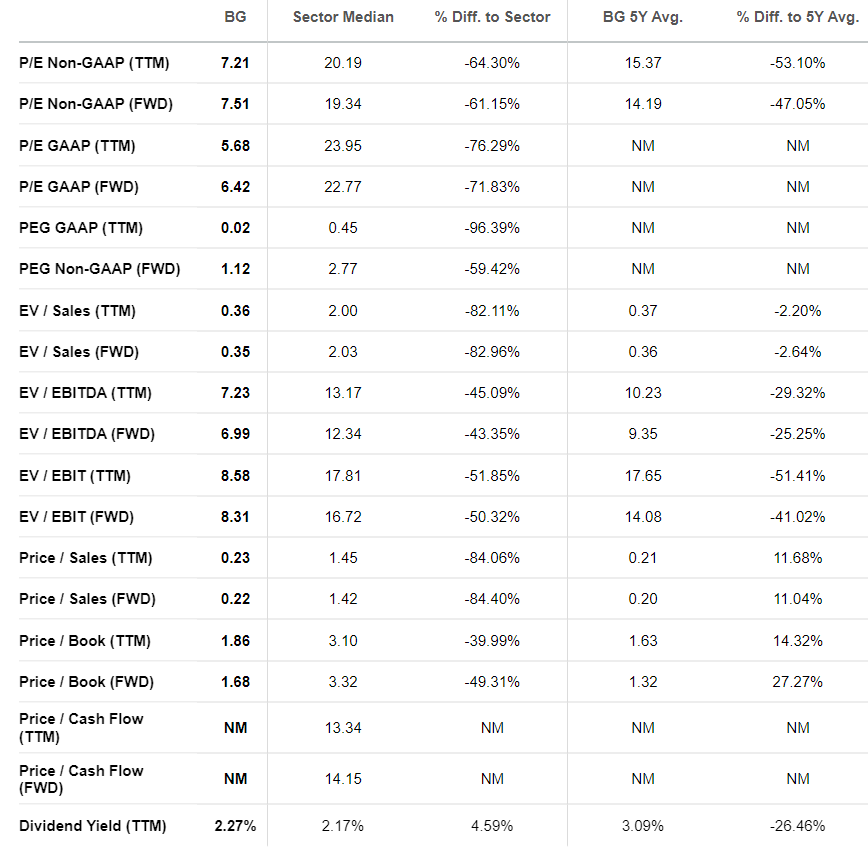

From 2011-2019, Bunge’s (BG) highest net income came in at $942 million. In the last 12 months, that number more than doubled to $2.398 billion. And there’s good reason to think the company’s strong performance will continue. Most of you probably aren’t too familiar with Bunge. Bunge operates one of the largest global agribusinesses with more than $55 billion in annual sales. The company primarily focuses on agricultural commodities from oil seeds to animal feed to fertilizers. It’s not sexy seeing as how it’s the 4th highest farm products stock search amongst financial pros. But it is consistent and profitable. In fact, the company has raised its dividend every year for the last decade. Current valuations put the company at a cheap 6.42x forward earnings and 0.22x price to sales. But there’s so much more here than meets the eye. Bunge’s Business As an agricultural behemoth, Bunge operates three key segments: Note: Sugar & Bioenergy and fertilizer are not considered core segments. The business profitability breaks down as follows: Agribusiness makes up the bulk of profits as well as volume. The breakdown of these operations is listed below. Recently, Chevron (CVX) and Bunge entered into a 50/50 joint venture to meet demand for renewable fuels with Chevron expected to invest $600 million into biofuels. Financials When you quickly glance at the financials, the company’s performance doesn’t look too impressive. Sales slowly declined over the last decade. However, margins improved. Yet, the company saw horrid operating cash flows for the last several years. Allow us to explain. Because of the international nature of the company’s business and commodity trade, management employs derivative contracts to hedge prices. These contracts act like insurance policies against the price of grains, oils, etc. The change in their value is reflected in earnings. However, you won’t see them show up in cash flows until they’re bought or sold. So, cash flows can be quite deceiving for Bunge. Sugar & bioenergy dragged down profits in 2019. This came as a one-time impairment of $1.524 billion associated with a joint venture in Brazil. Excluding notable items, Bunge’s earnings trend looks fantastic. Lastly, we want to highlight Bunge carries $4.8 billion in long-term debt as well as $4 billion in accounts payable. However, with $1.5 billion in cash and $8 billion in inventory, this doesn’t concern us much. Valuation As we noted earlier, Bunge trades at a marked discount to the consumer staples sector and its own historical metrics. We love the price-to-earnings and price-to-sales ratios. While the company trades a bit higher than its historical price-to-book, meaning the share price compared to the total assets, the difference isn’t that high to concern us. Even the lower than normal dividend yield still looks attractive. Our Opinion – 9/10 Bunge is making the right moves to position itself for the future with its Chevron partnership. Shares aren’t likely to double in the next year. But, this is a solid blue-chip stock to ease into your portfolio with a long-term outlook. |